Payroll reporting: definition, components, importance, types, process, common mistakes, and best practices

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll reporting is a detailed document that summarizes payroll-related information and employee compensation for a specific period. It records pay rates, working hours, gross wages, net pay, tax withholdings, and deductions. Companies that keep payroll reports organized stay compliant with labor and tax laws, avoid penalties, and maintain accurate financial records.

- Employer FICA rate: 6.2% Social Security and 1.45% Medicare on all employee earnings.

- FUTA rate: 6% on the first $7,000 of each employee's wages, offset by state credits.

- New hire reporting deadline: State agencies must receive new hire reports within 20 days of the hire date.

- Annual W-2 deadline: January 31 for issuing W-2 forms to employees and tax authorities.

- Payroll records retention: A minimum of four years after the fourth quarter filing date, per IRS requirements.

What is payroll reporting?

Payroll reporting is a detailed document that summarizes payroll-related information and employee compensation for a specific period. It records important details, such as pay rates, working hours (regular, overtime, and paid time off), gross wages, and net pay after deductions.

Payroll reporting adds a list of all payroll deductions, which include Social Security, Medicare, and federal, state, and local taxes, along with employer-paid taxes and contributions and voluntary contributions, like retirement and benefits.

Payroll reporting also covers employee identifiers (full legal name, ID, hiring date), payroll period details, leave balances, garnishments, and service fees. These reports support financial planning, budgeting, auditing, accurate tax filing, regulatory compliance, and communication with staff.

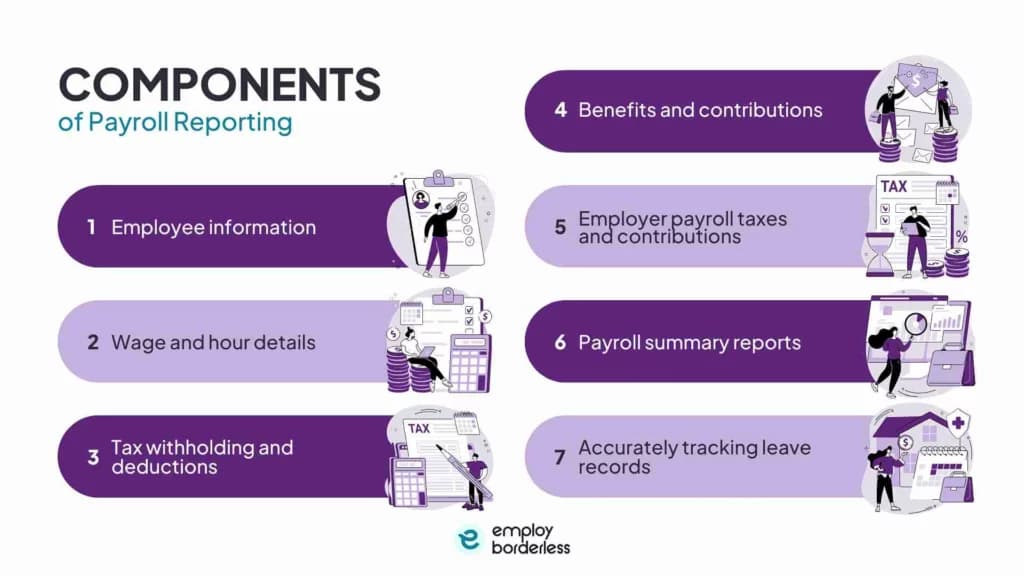

What are the components of payroll reporting?

The components of payroll reporting are employee information, wage and hour details, tax withholding and deductions, benefits and contributions, employer payroll taxes and contributions, payroll summary reports, and accurately tracking leave records.

These components must be reported accurately to reduce the risk of errors and penalties, and to maintain legal compliance and financial transparency.

Employee information

Employee information is the employment details that are recorded for each staff member within a company. This information includes the employee's full legal name, ID (Identification number), employee type, address, hiring date, job title, department, and supervisor.

Employee data is the basis for forms like W-2 and 1099, and quarterly filings like Form 941. Accurate data matters because out-of-date addresses cause delivery failures for forms like W-2s, Form I-9, and 1099s. Government authorities reject payroll reports that contain incorrect personal details, inconsistent data entry, incorrect worker classifications, or inaccurate tax filings.

Wage and hour details

Wage and hour details show the hours worked by employees within a specific pay period and the wages earned during the same period. This includes standard salaries or hourly rates, regular work schedules, overtime or double time, and any additional compensation like commissions, bonuses, or incentive payments.

Documenting this data makes sure workers receive fair compensation under laws like the FLSA (Fair Labor Standards Act) and that overtime is properly recorded. Overestimation and miscalculation of wages and hours create legal liability and wage settlement issues.

Companies use biometric time clocks, payroll systems like ADP, Rippling, TimeClock Plus, or time-tracking software to maintain compliance. These tools automate wage computation, pay rule application, and break recording, which reduces human error rates.

Tax withholding and deductions

Tax withholding is the process by which an employer deducts income and payroll taxes from an employee's pay cheque and sends the money directly to the government on the employee's behalf. This withholding acts as a prepayment towards the employee's annual tax liability.

Tax withholding and deductions include federal income tax, state and local taxes, and required FICA (Federal Insurance Contributions Act), Social Security, and Medicare contributions. They also cover involuntary deductions like child support and wage garnishments, and voluntary deductions like health insurance premiums and 401(k) contributions.

Employers must compute and submit tax withholdings regularly to federal, state, and local tax authorities - for example, by using the IRS EFTPS (Electronic Federal Tax Payment System) to deposit withheld FICA and federal income tax.

Benefits and contributions

Benefits are non-wage compensations, like health insurance, paid time off, and retirement plans that an employer provides to employees with standard pay. Employer contributions include FICA tax payments and HSA funding (Health Savings Account), while employee contributions are pre-tax or post-tax 401(k) contributions.

Employer-sponsored benefits include life and disability insurance, PTO (Paid Time Off), retirement plan contributions (such as pensions and 401(k)s), and health, dental, and vision insurance premiums. These benefits reduce gross wages through deductions and increase total compensation.

Accurate reporting is required for compliance with benefits regulations like ERISA (Employee Retirement Income Security Act). The payroll manager must match benefit deductions with provider invoices to avoid differences such as overpayment or missed contributions.

Employer payroll taxes and contributions

Employer payroll taxes and contributions are mandatory payments based on employee wages. These payments are separate from employee withholdings and are required to maintain legal compliance.

Employers pay FICA taxes on all employee earnings, 6.2% Social Security, and 1.45% Medicare, according to a tax topic titled "Topic no. 751, Social Security and Medicare withholding rates" published by the IRS (Internal Revenue Service).

Both FUTA (Federal Unemployment Tax Act) and SUTA (State Unemployment Tax Act) unemployment taxes are collected, but SUTA differs by state, while FUTA is 6% of the first $7,000 of an employee's wages (offset by state credits), according to an article titled "Unemployment Insurance Tax Topic" published by DOL (United States Department of Labor).

Employers also pay workers' compensation premiums, which are based on company records of compensation claims and the risk of job injury costs. Payroll taxes are submitted on forms such as FUTA through annual Form 940, and FICA and income taxes through quarterly Form 941.

Payroll summary reports

Payroll summary reports are documents that list every payroll-related activity, such as employee gross wages, hours worked, net pay, and bonuses and commissions, over a specified period, which are produced weekly, biweekly, or monthly.

These reports often show totals by department, job role, or location and include total gross pay, net pay, and all deductions for organizational analysis. Payroll experts use them to analyze total payroll costs, identify irregularities, and monitor budgetary metrics.

For instance, a payroll summary may show that the sales department's gross wages rose by 10% during the quarter, prompting a closer review of staff adjustments.

Accurately tracking leave records

Tracking leave records means carefully recording and keeping track of employees' time off in terms of vacation, sick leave, and FMLA (Family Medical Leave Act), to support compliance, payroll accuracy, and workforce planning.

These records are stored in centralized systems or specialized software, which includes leave balances, accruals, usage dates, and reasons. Accurate leave records help companies comply with labor laws and prevent errors like overpayments or underpayments. For example, a management tool that automatically tracks PTO accruals and usage makes payroll processing error-free and helps avoid disputes.

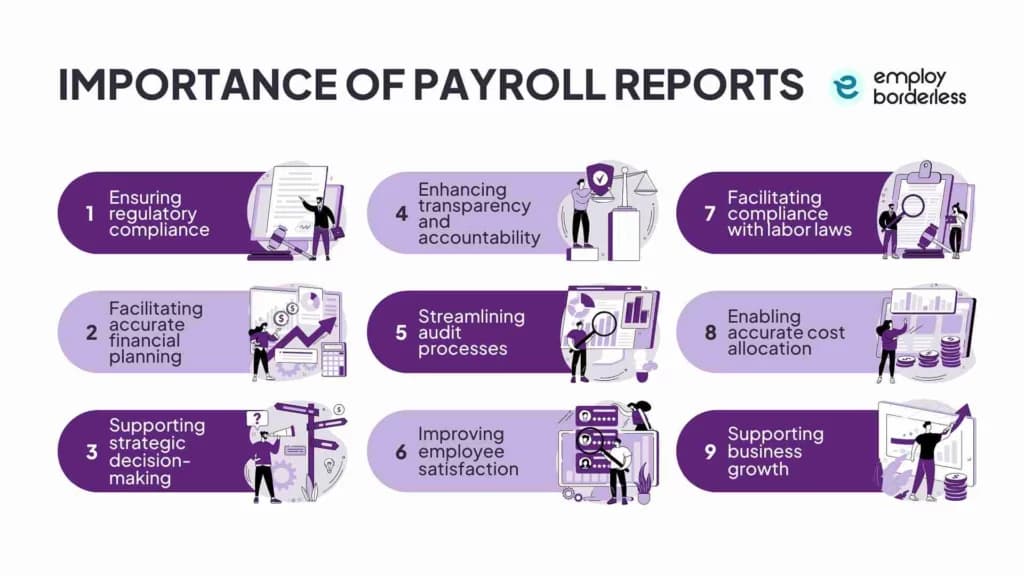

Why are payroll reports important?

Payroll reports are important because they ensure regulatory compliance, facilitate accurate financial planning, support strategic decision-making, improve employee satisfaction, facilitate compliance with labor laws, and support business growth. They support financial planning, guarantee legal compliance, and direct strategic business choices.

The reasons why payroll reports are important are listed below.

Ensuring regulatory compliance: Regulatory compliance means accurately and quickly reporting payroll to comply with all applicable laws and regulations related to labor standards, such as FLSA and FMLA. It requires creating and keeping records that satisfy legal specifications for filings, audits, and government supervision. For instance, a U.S. company moving to real-time benefits in-kind payroll reporting (beginning April 2026) must train employees and update systems before the deadline to reduce last-minute compliance risks.

Facilitating accurate financial planning: Accurate financial planning means using timely payroll data to inform budgeting, cost estimation, cash flow management, and cost control. Payroll reports give a clear picture of labor-related costs, such as wages, taxes, and benefits, which makes it easier to estimate future spending and make financial decisions.

Supporting strategic decision-making: This is the process of using payroll data to make strategic decisions that support organizational goals, compliance, and workforce management. Integrated payroll systems such as HR/ERP (Human Resources/Enterprise Resource Planning Systems) allow targeted employee adjustments, global reporting, and advanced payroll solutions. They also help companies compare providers, verify vendor SLAs (Service Level Agreements), and predict problems like rising labor expenses.

Enhancing transparency and accountability: Transparent and detailed payroll reports give employees insight into their compensation, including wages, deductions, taxes, and benefits. Transparent payroll reporting assures employees that their pay cheques are fair and accurate, while accurate documentation makes internal reviews and regulatory audits easier.

Streamlining audit processes: Payroll reports reduce manual labor in audit processes, increase accuracy, and quickly surface errors or compliance issues. Payroll records, financial data, and attendance logs are automatically compared by systems, which identify differences before audit processing. Real-time monitoring also helps in identifying irregularities early.

Improving employee satisfaction: Accurate, timely, and transparent compensation builds trust and workplace morale. Employees rely on their income, so payment errors or delays cause stress and damage trust. Clear pay stubs and communication promote clarity and reduce disputes.

Facilitating compliance with labor laws: Payroll reporting helps organizations stay compliant with applicable labor laws across federal, state, and local jurisdictions. It ensures employees receive legally required compensation (minimum wage and overtime) and accurately differentiates between contractor and employee roles and exempt and non-exempt statuses to avoid misclassification penalties.

Enabling accurate cost allocation: Cost allocation means assigning labor costs, including wages and taxes, to specific departments or projects using detailed payroll data. This improves accountability and budgeting by showing which programs or cost centers are responsible for labor expenses.

Supporting business growth: Payroll reporting uses payroll data to help businesses maintain financial stability and grow by managing workforce costs accurately. Automated systems reduce human error, support hiring budgeting and resource allocation, and keep the company compliant with labor law as it scales.

What are the types of payroll reports?

The types of payroll reports are employee earnings report, payroll summary report, tax liability report, quarterly payroll tax reports, annual payroll tax reports, certified payroll reports, retirement contribution reports, custom payroll reports, federal payroll reports, state payroll reports, and local payroll reports.

Employee earnings report

An employee earnings report is a detailed record of an employee's payroll history, which includes gross pay, net pay, working hours, tax withholdings, deductions, and yearly totals.

For instance, it may include regular wages, overtime, FICA, and 401(k) contributions. It provides transparency, which allows employees to verify their pay details. This report is useful for companies of all sizes, from startups to large enterprises.

Payroll summary report

A payroll summary report provides a summary of a business's payroll activity over a given period, which includes total gross wages, employer taxes or contributions, deductions, and net pay. For example, a company's payroll summary report from June 1 to June 15 shows gross income of $120,000, taxes of $20,000, deductions of $8,000, and net income of $92,000, and provides a brief overview of payroll accuracy and cash flow. This type of payroll summary report is used by startups, small businesses, and large corporations.

Tax liability report

The tax liability report lists employer payroll tax obligations and employee gross pay, taxable wages, and withheld taxes (such as FICA, FUTA, and Medicare) for a selected period. For instance, a company's tax liability report from July 1 to July 30 accounts for gross pay of $300,000, FICA withheld $20,000, FUTA liability $900, and Medicare $3,000.

It tracks payroll taxes that are due and withheld, which helps in accurate tax compliance and avoids penalties. It is useful to medium-sized and larger organizations that process different payroll tax forms.

Quarterly payroll tax reports

A quarterly payroll tax report (such as IRS Form 941) shows information about income, Social Security, and Medicare taxes withheld as well as the employer's tax liabilities for the quarter. For example, according to a quarterly payroll tax report, the company paid $600,000 in wages during the second quarter (April 1 to June 30), withheld $35,000 in employee FICA taxes, and owed $45,000 in employer FICA, for a total of $80,000 in federal payroll taxes.

The report helps businesses avoid IRS penalties and maintain timely tax deposit compliance. Businesses, particularly medium to large-sized enterprises, rely on quarterly tax reports to stay current with federal regulations.

Annual payroll tax reports

Annual payroll tax reports summarize all payroll taxes for the year and help businesses correctly file Forms 940, 944, W-2, and W-3 and confirm full-year tax compliance. For instance, in 2024, the company's total wages were $2.4 million, FICA withheld $180,000, employer FICA $180,000, and FUTA liability $30,000.

The annual tax report compiles all employee taxes and compensation for IRS and SSA (Social Security Administration) reporting. All employers must maintain compliance with annual reporting requirements, such as Forms W-2, W-3, 940, and 944.

Benefits and deductions report

The benefits and deductions report covers each employee's contributions, such as health, insurance, retirement plans, and employer matches or deductions by pay period. It helps businesses monitor benefit costs, accurately administer benefits, and maintain compliance with reporting regulations.

For example, a benefits and deductions report shows employee A's health insurance deduction is $200, 401(k) contribution is $300, and employer match is $150. This report is helpful for medium to large companies that provide employee benefits, but also for small businesses that want to keep benefit costs under control.

PTO (Paid Time Off) report

A PTO (Paid Time Off) report keeps track of each employee's accrued and used PTO, which includes vacation, sick, and personal days. For instance, in May, employee A accrued 16 hours, used 8 hours, with 8 hours remaining in their PTO balance.

This report helps employers maintain accrual and payout policy compliance, manage scheduling, and avoid overwork. It is helpful for startups, small to medium-sized businesses, and other organizations tracking employee availability and leave trends.

Direct deposit register

A direct deposit register is a payroll report that lists all direct deposit payments made during a pay period, which includes employee IDs and names, bank routing and account information, deposit amounts, and payment dates for each payroll run.

For instance, the payroll statement "May 15 payroll: employee A (account ending number 1345) received $2,600 and employee B (account ending number 8789) received $3,300" makes it clear who was paid, how much, and to which bank account. This allows payroll teams to compare ACH (Automated Clearing House) files with actual bank deposits and confirm that each employee was paid accurately.

Workers' compensation report

The workers' compensation report summarizes employee wages by job classification over a specified period. For instance, the company reported a gross wage of $50,000 for clerical staff and $60,000 for field technicians during the April 1 to April 30 payroll period. The taxable payroll for workers' compensation during that time was $110,000.

This report is useful for medium-sized to large businesses in monitored or high-risk sectors, such as manufacturing or construction, where accurate wage distribution by job code is required for cost control and insurance compliance.

New hire report

The new hire report is a legally mandated payroll report that lists all recently hired or rehired employees and is submitted to state agencies within 20 days of the hire date.

For instance, a company makes a new hire report that includes employee A, SSN (Social Security Number) 124-85-3864, 101 Main Street, Hired: 21/05/2025, Employer EIN (Employer Identification Number): 11-2045684. This report helps with workforce tracking, reduces the risk of welfare and unemployment fraud, and enforces child support. All companies must comply with state and federal laws to avoid penalties.

Job costing report (for construction and project-based work)

A job costing report (for construction and project-based work) keeps track of all labor expenses related to a particular project, such as hours worked, employee wages, overtime, payroll taxes, and fringe benefits.

For instance, from May 1 to May 31, a full-service construction company's project reported labor costs of approximately $16,000 for foundation work, $14,000 for plumbing, and $12,000 for electrical. The project's total labor cost of about $42,000 shows how payroll costs were allocated to different tasks.

This report is particularly helpful for contractors and businesses handling different bids or projects, including small remodeling crews and major construction companies that require financial transparency.

Certified payroll reports

A certified payroll report is a weekly payroll report required by the U.S. Department of Labor from contractors involved in federally funded construction projects and is submitted using Form WH-347.

For instance, an electrician worker worked 5 overtime hours and 40 regular hours on a federal project during the week ending April 10, 2025. His gross wage was $1,300, his fringe benefit was $400, and he received a net pay of $1,080. He used Form WH-347 to file the report and filed a signed compliance statement to certify compliance with Davis-Bacon standard wage requirements.

This report helps contractors comply with Davis-Bacon Act regulations, pay appropriate wages, and accurately record hours according to job classification.

Retirement contribution reports

The retirement contributions report compiles an employee's pre-tax contributions to a retirement plan, like a 401(k), for each pay period.

For example, employee A made a payroll deduction of approximately $700 to her traditional 401(k) plan for the May 2025 payroll cycle. This sum was filed under her retirement deductions, withheld before taxes, and sent to the retirement plan provider for investment.

This report is useful for businesses of all sizes that offer employee-funded retirement plans because it confirms that contributions are correctly withheld and applied, reduces taxable wages, and supports compliance with IRS limits.

Custom payroll reports

A custom payroll report is a customized payroll summary according to user-specified criteria, like date range, employee groups, and particular fields, like department, bank account, or working hours.

For example, the department-filtered custom payroll report for April 2025 shows the sales department report of employee A, ID (Identification Number) 012, gross pay of $4,000, taxes of $650, deductions of $1,500, and net pay of $3,500. This report is best for all types of businesses as it provides flexible insight into payroll data by offering deeper analysis, automated reports, and customized views.

Federal payroll reports

Federal payroll reports are a government-mandated document that records employee wages, tax withholdings, and employer tax obligations, which include Social Security, Medicare, and federal unemployment taxes.

For instance, the employer reported $260,000 in total wages paid, $17,000 withheld for federal income tax, $16,000 in employer and employee Social Security and Medicare taxes, and timely tax deposits to the IRS on Form 941 for the second quarter of 2025. The majority of U.S. employers who deduct federal income, Social Security, or Medicare taxes must submit Form 941 every quarter, except for some seasonal, agricultural, or household employers.

State payroll reports

A state payroll report is a legally mandated payroll filing made to state and sometimes local governments. It covers payroll-related information such as income tax withheld, state unemployment tax, and, in some jurisdictions, workers' compensation contributions.

For example, a quarterly state report might include monthly quarter one 2025 gross wages of $130,000, state income tax withheld of $8,600, and state unemployment tax of $1,900. These reports are used by all companies in a state that employs people, regardless of size or sector.

Local payroll reports

Local payroll reports track payroll-related taxes and deductions mandated by city or government authorities, such as workers' compensation contributions, payroll expense taxes, and local income taxes.

For example, a Philadelphia-based company submits its local payroll report for the first quarter of 2025, which shows total gross wages of $140,000, city wage tax withheld of $1,670, and local services tax of $400. This report is important for companies working under government authorities that impose payroll-specific taxes.

| Report type | Key data captured | Filing form / frequency | Who uses it |

|---|---|---|---|

| Employee earnings report | Gross pay, net pay, hours, tax withholdings, deductions | Per pay period | All employers |

| Payroll summary report | Total gross wages, taxes, deductions, net pay | Weekly / biweekly / monthly | All employers |

| Tax liability report | Gross pay, FICA withheld, FUTA liability, Medicare | Per pay period | Medium to large organizations |

| Quarterly payroll tax report | Income, Social Security, Medicare taxes withheld | Form 941 - quarterly | Most U.S. employers |

| Annual payroll tax report | Full-year wages, FICA, FUTA liability | Forms 940, 944, W-2, W-3 - annually | All employers |

| Benefits and deductions report | Health, retirement, employer match per employee | Per pay period | Medium to large employers |

| PTO report | Accrued, used, and remaining leave balances | Per pay period / monthly | All employers |

| Direct deposit register | Employee IDs, bank details, deposit amounts, dates | Per payroll run | All employers using direct deposit |

| Workers' compensation report | Wages by job classification | Monthly / quarterly | Medium to large, high-risk sectors |

| New hire report | Employee name, SSN, address, hire date, EIN | Within 20 days of hire | All employers |

| Job costing report | Labor costs per project task | Per project / monthly | Construction and project-based businesses |

| Certified payroll report | Hours, wages, fringe benefits by job classification | Form WH-347 - weekly | Federal construction contractors |

| Retirement contribution report | Pre-tax 401(k) contributions per employee | Per pay period | All employers offering retirement plans |

| Custom payroll report | User-defined fields by date range, department, or group | On demand | All employers |

| Federal payroll report | Wages, federal income tax, Social Security, Medicare | Form 941 - quarterly | Most U.S. employers |

| State payroll report | State income tax withheld, SUTA | Quarterly | All state employers |

| Local payroll report | City wage tax, local services tax | Quarterly | Employers in cities with local payroll taxes |

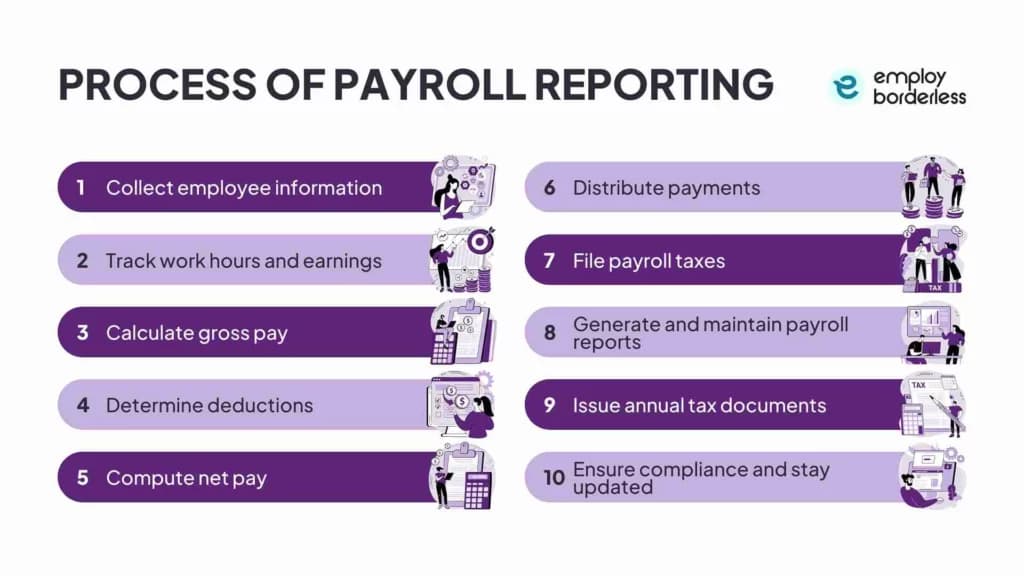

What is the process of payroll reporting?

The process of payroll reporting is collecting employee information, tracking work hours and earnings, calculating gross pay, determining deductions, computing net pay, distributing payments, filing payroll taxes, generating and maintaining payroll reports, issuing annual tax documents, and ensuring compliance and staying updated.

The processes of payroll reporting are listed below.

Collect employee information: Collecting employee information is the process of gathering personal, tax, banking, and work-related data required to compute payroll and guarantee legal compliance. These include tax forms (such as W-4 or local equivalents), work authorization documents (such as I-9 in the United States), banking information for direct deposit, classification information (hourly or salaried, exempt status, benefits enrollment), and legal identifiers (such as Social Security Number or national ID).

Track work hours and earnings: Tracking work hours and earnings means accurately documenting the time employees spend on the job, including start and end times, breaks, and overtime. This information confirms that employees receive fair compensation and that payroll complies with labor laws. It also covers timesheet approval, time entry (clocking in and out), earnings computation, and payroll system integration for tax deductions and wage payments.

Calculate gross pay: Calculating gross pay is the process of calculating an employee's total earnings before any deductions. The payroll or HR department divides the annual salary by the number of pay periods for salaried employees, and multiplies the number of hours worked (including overtime at the proper rate) by the wage for hourly workers. It then adds any extra pay, such as commissions, tips, bonuses, holiday pay, or shift differentials.

Determine deductions: Determining deductions involves calculating all mandatory and voluntary deductions from an employee's gross pay. Social Security, Medicare (FICA), federal, state, and local taxes are mandatory deductions. Voluntary deductions are employee-selected expenses, such as retirement contributions and health insurance premiums.

Compute net pay: Computing net pay means withholding all relevant deductions from an employee's gross pay - taxes, retirement contributions, insurance premiums, and garnishments - to calculate their take-home pay. This is the real amount employees receive in their paychecks and must be correct for both legal compliance and employee satisfaction.

Distribute payments: Distributing payments is the process of selecting a method to deliver net pay. Payments are made with cash, pay cards, physical checks, or EFT (Electronic Fund Transfers), depending on the company's setup and employee preferences. Employers also create pay stubs, archive payment records, settle transactions, and manage fund splits to confirm all distributions are finished and accurately documented.

File payroll taxes: Filing payroll taxes means sending the required tax forms and payments to the government for taxes deducted from employee paychecks, as well as the employer's portion. This covers federal income tax, Social Security, Medicare, and unemployment taxes on forms such as IRS Form 941 and Form 940.

Generate and maintain payroll reports: Generating payroll reports means creating detailed summaries of payroll information for each pay period or time frame. For instance, a small retail company generates a monthly payroll summary at the end of each month showing $245,000 in gross pay, $60,000 in tax withheld, $25,000 in benefits deductions, and each employee's net pay. The report is then stored in the payroll system for budgeting, compliance audits, and year-over-year cost comparisons.

Issue annual tax documents: Issuing annual tax documents means employers create and send year-end tax forms to both employees and tax authorities. Every employee receives a W-2 form summarizing their total pay and tax withholdings. Both the IRS and employees receive these forms by the mandatory deadline, which is usually January 31, according to a news release titled "IRS reminds employers of January 31 deadline for Form W-2, other wage statements" published by the IRS (Internal Revenue Service).

Ensure compliance and stay updated: This is the process of staying current with payroll laws and regulations to prepare for any tax or legal changes. It requires routinely checking payroll policies against the most recent labor laws, tax laws, and governmental orders to avoid penalties and confirm accurate reporting.

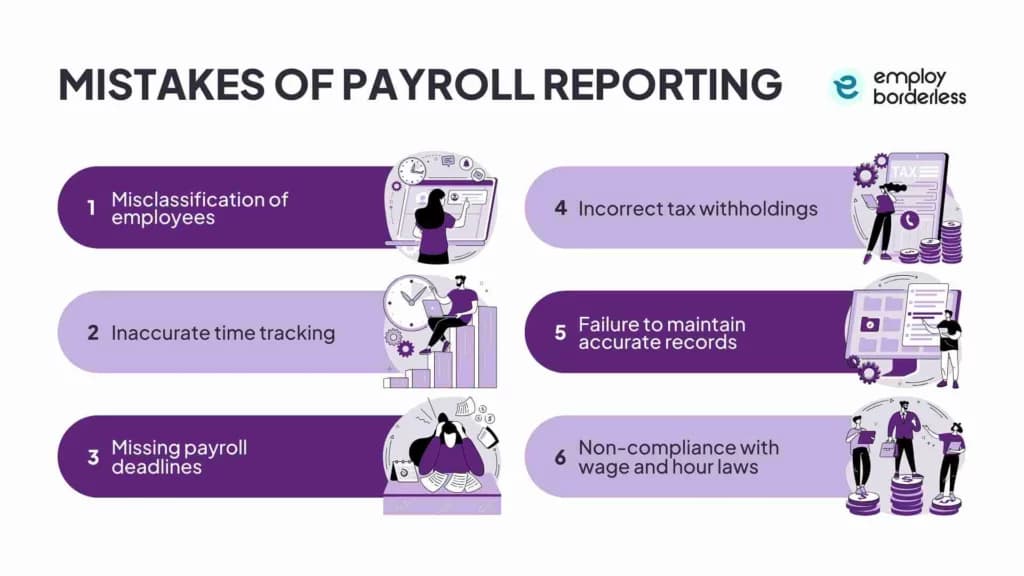

What are the payroll reporting mistakes?

The payroll reporting mistakes include misclassification of employees, inaccurate time tracking, missing payroll deadlines, incorrect tax withholdings, failure to maintain accurate records, and non-compliance with wage and hour laws.

The payroll reporting mistakes are listed below.

Misclassification of employees: Misclassification means labeling an employee as an independent contractor or vice-versa. This restricts workers' benefits such as unemployment insurance, overtime compensation, minimum wage, and tax withholding protections. Companies sometimes make false classifications to avoid paying benefits, payroll taxes, and labor law obligations.

Inaccurate time tracking: Inaccurate time tracking means employees' actual hours are not correctly recorded - for example, through missing clock-ins, rounded or estimated entries, or manual errors that cause inaccurate payroll calculations and compliance issues. This raises labor expenses, causes payroll errors, and puts companies at risk of fines or audits.

Missing payroll deadlines: Missing payroll deadlines is the failure to process or submit payroll, including employee compensation and tax payments, by the planned or legally mandated date. This causes wage delays, IRS penalties, violations of labor laws such as the FLSA (Fair Labor Standards Act), and damage to the company's reputation and employee trust.

Incorrect tax withholdings: Incorrect tax withholdings occur when an employer withholds too much or too little tax from a pay cheque, due to inaccurate payroll setup, out-of-date tax tables, Form W-4 errors, or software mistakes. These errors cause IRS penalties, unexpected tax bills for workers, and the requirement to file Form 941-X.

Failure to maintain accurate records: Failure to maintain accurate records means not creating or keeping complete payroll documentation, including hours worked, wages paid, deductions, and time logs, as required by law. Employers face audit risks, back-pay claims, penalties, and legal liability as a result.

Non-compliance with wage and hour laws: Non-compliance with wage and hour laws means an employer fails to meet legal requirements for paying workers correctly, such as minimum wage, overtime pay, recordkeeping, and working conditions, as specified by laws like the U.S. FLSA and state regulations. Violations include failing to provide mandatory breaks, misclassifying non-exempt workers, or not paying overtime.

What are the best practices for payroll reporting?

The best practices for payroll reporting are to automate payroll, update employee records, monitor tax laws, audit payroll regularly, secure payroll data, standardize procedures, meet reporting deadlines, integrate systems, and train payroll staff.

The best practices for payroll reporting are listed below.

Automate payroll: Automate payroll is the use of payroll software to reduce manual labor by handling standard payroll tasks, such as data entry, gross and net pay computations, deductions, payments, tax filing, and reporting. This increases productivity, keeps the company tax-law compliant, and reduces errors that cost staff time.

Update employee records: Updating employee records maintains data accuracy and compliance, including job titles, department changes, contact details, salary adjustments, and role status updates. For example, if an employee changes their mailing address mid-year, HR must update it in the system before processing payroll to confirm that W-2 and other tax forms are delivered correctly. The address needs to be updated by January 5 if year-end W-2 processing starts on January 6 to avoid misdelivery.

Monitor tax laws: Monitoring tax laws means staying informed of recent and future changes to federal, state, and local payroll-related tax laws, including tax rates, deadlines, and compliance requirements. Employers stay current by reviewing legal notifications, subscribing to updates, and using tools such as automated payroll systems or compliance calendars.

Audit payroll regularly: Regular payroll audits involve a systematic review of payroll documentation, procedures, and transactions. This is done for each pay period, with at least a thorough audit performed quarterly or annually to confirm accuracy and compliance and identify irregularities such as incorrect deductions, misclassifications, or ghost workers.

Secure payroll data: Securing payroll data means protecting all sensitive payroll information, including employee IDs, Social Security numbers, bank account details, and wage data. HR teams secure payroll data by using strong access controls, encryption, authentication, and backups to prevent fraud, unauthorized access, and data breaches.

Standardize procedures: Standardized procedures mean every pay cycle follows a reliable process through documented steps for all payroll tasks, such as time tracking, data entry, payroll calculation, deductions, and reporting. These procedures support global growth, simplified operations, and strategic insights.

Meet reporting deadlines: Meeting reporting deadlines means completing payroll-related tasks, like filing withholdings, submitting tax forms, and issuing pay cheques, on the appointed dates to avoid fines, stay compliant, and keep employee trust. It also supports consistent audits and financial reviews by keeping all records current and available.

Integrate systems: Integrating systems means connecting payroll software to other business tools, like HR, accounting, time tracking, and expense systems, so data moves between them automatically. For instance, a medium-sized consulting business that previously ran separate payroll and HR systems integrated the two to reduce administrative effort, improve accuracy, and gain real-time insights for better decision-making.

Train payroll staff: Training payroll staff means giving employees regular, structured instruction on payroll operations, software use, compliance standards, tax updates, audit procedures, and best practices. Trained payroll staff resolve employee problems faster, deliver on-time payments, and build trust inside the company.

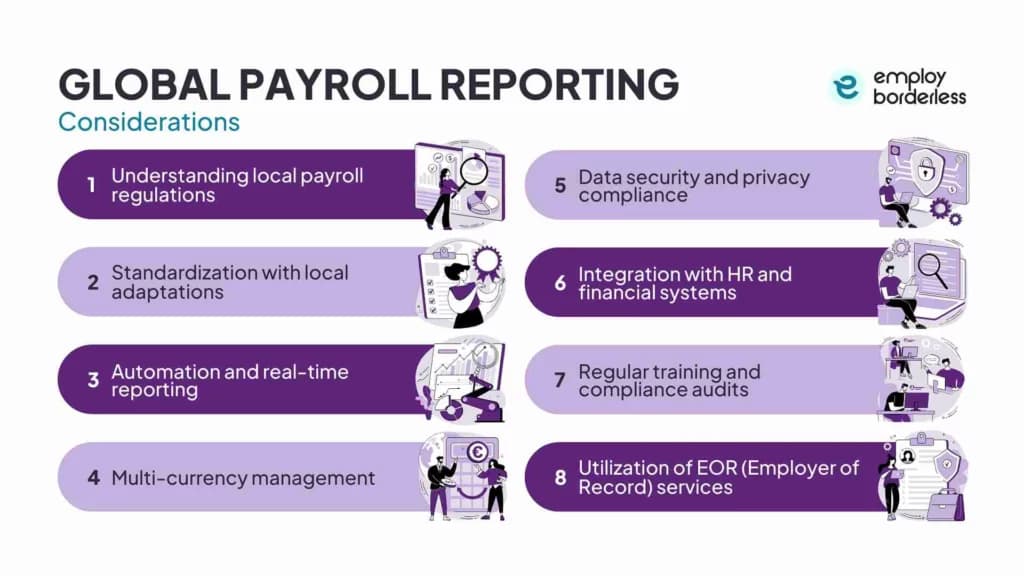

What are the global payroll reporting considerations?

The global payroll reporting considerations are understanding local payroll regulations, standardization with local adaptations, automation and real-time reporting, multi-currency management, and utilization of EOR (Employer of Record) services.

The global payroll reporting considerations are listed below.

Understanding local payroll regulations: Understanding local payroll regulations means staying aware of and complying with local laws relating to employee compensation, tax withholdings, Social Security contributions, labor standards, legal benefits, and payroll reporting deadlines. This knowledge helps businesses fulfill their legal responsibilities in every country where they operate and avoid fines.

Standardization with local adaptations: Standardization with local adaptations means developing a single, uniform global payroll procedure that also complies with local payroll regulations. It covers data formats, reporting techniques, and finding a balance between local differences and global consistency. This reduces errors, improves compliance, and supports growth across markets.

Automation and real-time reporting: Automation with real-time reporting means using cloud-based payroll technology to automate data collection, payments, filings, and tax and benefit computations, while producing current payroll reports and compliance records across multiple countries. For example, a global corporation used an automated payroll system to instantly identify a new UK employee's missing tax ID. The payroll manager quickly resolved the issue by retrieving the correct ID from HR records, updating it in the system, and confirming the entry.

Multi-currency management: Multi-currency management is the ability of payroll systems to process salaries, taxes, and reports in different local currencies while automatically applying accurate exchange rates and combining data into a single reporting currency for global oversight. This keeps the company's financial records stable and confirms workers are paid in their local currency as required by law.

Data security and privacy compliance: Data security and privacy compliance means using strong policies and procedures, such as encryption, access controls, secure storage, and legal frameworks, to protect sensitive payroll data including salaries, tax IDs, and bank account information. Companies must follow applicable data protection laws, such as the CCPA (California Consumer Privacy Act) and GDPR (General Data Protection Regulation), and international standards, such as ISO 27001/27701 (Information Security Management System).

Integration with HR and financial systems: Integration with HR and financial systems is the connection of payroll software with financial and accounting systems, such as ERP (Enterprise Resource Planning) or general ledger, and HRIS (Human Resource Information System) and HRMS platforms (Human Resource Management System), including time and attendance and benefits. This allows automatic data exchange, smooth payroll expense reporting, and consistent global payroll operations.

Regular training and compliance audits: Regular training and compliance audits mean keeping employees informed of current rules and carrying out internal and external checks to confirm that payroll procedures, documentation, and files comply with local and global legal requirements. These steps reduce errors and risks, build employee trust, and improve payroll credibility.

Utilization of EOR (Employer of Record) services: Using EOR services means engaging a third-party legal entity that employs foreign workers on your behalf while you retain control over daily operations and management. The EOR manages payroll and filings, confirms compliance with local labor and tax rules, and reduces administrative burden.

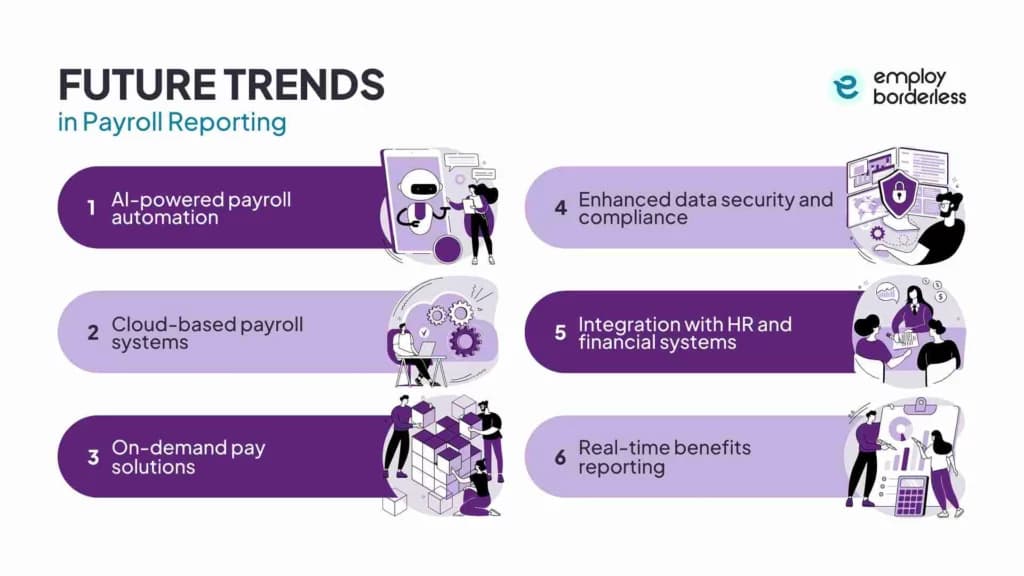

What are the future trends in payroll reporting?

The future trends in payroll reporting are AI-powered payroll automation, cloud-based payroll systems, on-demand pay solutions, enhanced data security and compliance, integration with HR and financial systems, and real-time benefits reporting.

The future trends in payroll reporting are listed below.

AI-powered payroll automation: AI-powered payroll automation is the use of artificial intelligence, including machine learning and generative AI, to automate processes such as data entry, tax compliance, and regulatory compliance over time. AI-assisted tools recognize errors in payroll reporting (duplicate payments or missing IDs), make real-time compliance updates, and provide predictive insights, which allows payroll departments to fix problems before payroll cycles close.

Cloud-based payroll systems: Cloud-based payroll systems are internet-based platforms maintained on remote servers, accessed via an internet connection, that automate payroll actions including wage and salary calculations, tax deductions, payment issuance, and reporting. These systems allow faster, more accurate payroll reporting and support geographic independence and transparency.

On-demand pay solutions: On-demand pay, also known as EWA (Earned Wage Access), is a system that allows employees to access a portion of their earned income before payday. It uses payroll integration to track work hours, compute available pay, and handle deductions automatically. Companies must maintain updated payroll tracking methods and digital networks to offer on-demand pay, which also allows real-time reporting to tax authorities.

Enhanced data security and compliance: Enhanced data security and compliance is the use of advanced technologies, like encryption, secure cloud platforms, and audits, to keep employee payroll data safe and compliant with legal requirements. Companies are updating their payroll systems to include auto-compliance updates and real-time security protection.

Integration with HR and financial systems: Companies are connecting their payroll systems with HR and financial platforms to increase overall payroll administration efficiency, stay compliant with changing legal requirements, and produce faster, error-free reports.

Real-time benefits reporting: Real-time benefits reporting is the real-time processing and reporting of employee benefits directly to payroll systems, such as ADP (Automatic Data Processing) and Gusto. This allows taxable benefits to be taxed in real-time, typically every month depending on the employee's pay cycle.

What is the purpose of payroll?

The purpose of payroll is to make sure that workers are paid correctly and on time for the labor they perform. It also manages the calculation, deduction, and payment of taxes and other deductions. It involves determining pay, maintaining track of hours worked, and complying with tax laws.

Payroll also includes the list of employees and their salaries, which are deducted from gross income as an expense to reduce taxable income. Companies use software to accurately handle payroll while following regulations like the FLSA (Fair Labor Standards Act), which establishes rules for minimum wage, overtime compensation, and specific child labor restrictions.

What role does data accuracy play in effective payroll reporting?

The role data accuracy plays in effective payroll reporting is to make sure that workers are paid properly and that businesses maintain compliance with labor and tax regulations. Companies use automated payroll systems and audits for payroll accuracy to make sure reporting is effective and transparent.

Which components are essential for comprehensive payroll reporting?

The components essential for comprehensive payroll reporting are employee data, employee earnings, tax withholdings and deductions, net pay, employer payroll taxes and contributions, wage and hour details, and payroll summary reports. These payroll components help in accurate, clear, and legally compliant payroll reporting.

What are the KPIs (Key Performance Indicators) to monitor in payroll reporting?

The KPIs (Key Performance Indicators) to monitor in payroll reporting are payroll processing time, payroll accuracy rate, compliance rate, cost of payroll errors, overtime costs, employee satisfaction, employee leave, training costs, and turnover rate. Payroll KPIs allow companies to use both historical and current payroll data, identify patterns, improve decision-making, and avoid problems that impact payroll compliance.

How long are businesses required to store payroll records?

Businesses are required to store payroll records for a minimum of four years following the date on which the fourth quarter of the year was filed, according to an article titled 'Employment tax recordkeeping' published by the IRS (Internal Revenue Service). These records involve different kinds of paperwork like employer identification numbers, wage payments, employee information, tax deposits, and copies of filed forms, which have to be available for IRS review.

Why is data compliance critical in payroll reporting processes?

Data compliance is critical in payroll reporting processes because it protects sensitive employee information, guarantees compliance with legal and regulatory standards, and maintains organizational credibility. Payroll compliance improves employee morale and trust as workers expect their financial and personal information to be handled safely and responsibly.

What are the steps involved in generating accurate payroll reports?

The steps involved in generating accurate payroll reports are collecting employee information, tracking work hours and earnings, calculating gross pay, determining deductions, computing net pay, distributing payments, filing payroll taxes, generating and maintaining payroll reports, issuing annual tax documents, ensuring compliance, and staying updated. Payroll processing steps guarantee accurate payroll processing and compliance with legal standards.

How do payroll summaries and payroll tax reports differ?

Payroll summaries and payroll tax reports differ in terms of usage and compliance, content included, frequency and timing, purpose, regulatory relevance, filing schedules, and legal obligations. Payroll summaries provide a brief overview of all payroll operations over a given period, which includes gross pay, net pay, deductions, and employer contributions. Payroll tax reports explain the taxes deducted from employee wages and the employer's tax obligations and are used for external compliance when submitting government forms, like IRS Form 941 or 940.

How do in-house payroll systems manage reporting tasks?

In-house payroll systems manage reporting tasks by using integrated software that creates both standard and customized payroll reports and automates the calculation of wages, taxes, and deductions. In-house payroll systems need trained personnel and frequent updates to stay compliant with changing tax regulations, and they also provide real-time access, error correction, and data security.

What advantages do cloud-based payroll systems offer for reporting?

The advantages that cloud-based payroll systems offer for reporting are centralized employee data in one place, real-time analytics, and efficient report generation (without the need to switch between tools). Cloud-based payroll systems provide automated updates that reduce manual errors and legal risks by keeping reports aligned with current tax rates and compliance regulations.

What is the recommended frequency for generating payroll reports?

The recommended frequency for generating payroll reports depends on the company's payroll schedule. Payroll reports are usually generated weekly, biweekly, or monthly for each pay period. Compliance also calls for more thorough reports, such as annual summaries for W-2s and Form 940, and quarterly tax filings such as IRS Form 941. Frequent reporting supports timely tax submissions, audit readiness, accuracy, and early detection of errors.

How is AI transforming payroll reporting practices?

AI is transforming payroll reporting practices in terms of accuracy, providing predictive insights, automating repetitive data tasks, and helping identify irregularities early, such as duplicate payments or misclassifications. AI in payroll reduces legal risk by automatically applying the correct tax settings and continuously monitoring regulatory changes.

What is the significance of audits in payroll reporting?

The significance of audits in payroll reporting is confirming the correctness of wage computations, tax withholdings, and employee classifications. They help in identifying errors and fraud and guarantee compliance with tax and labor laws. The role of audits in payroll maintains the accuracy of payroll operations, which also improves financial transparency, reduces the risk of fines, and improves internal controls.

How does outsourcing payroll functions affect reporting accuracy?

Outsourcing payroll functions affects reporting accuracy by reducing manual payroll errors, such as incorrect tax withholdings, benefit miscalculations, and missed overtime, through automated systems, expert knowledge of tax regulations, and regular compliance reviews. Companies also face payroll outsourcing problems, such as delays in updates through miscommunication or loss of control over real-time changes in information that affect the accuracy and timeliness of reports.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations