Payroll importance: what it is and why it is essential for business

Robbin Schuchmann

Co-founder, Employ Borderless

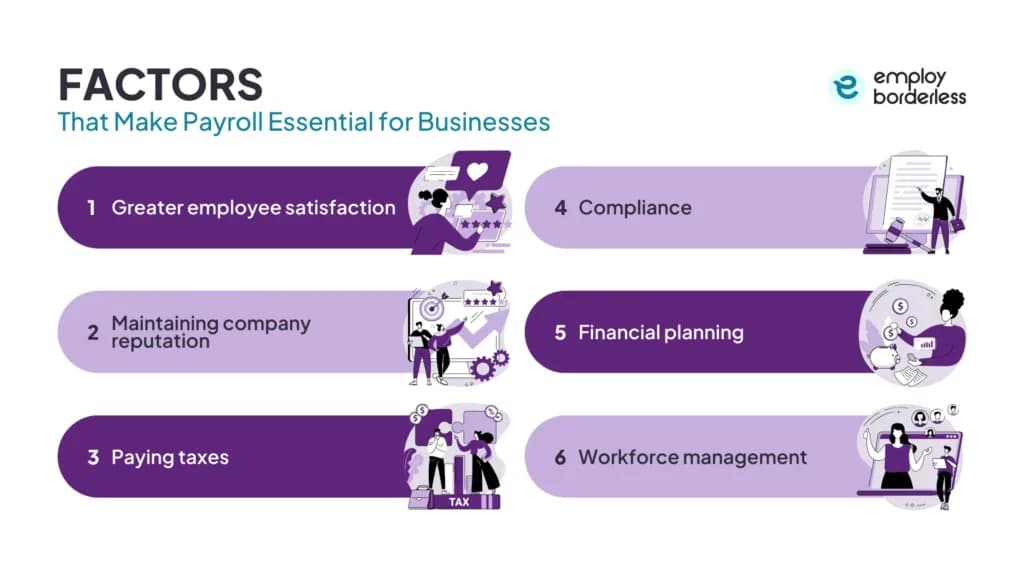

Payroll is important because it directly affects employee trust, tax compliance, cash flow, and legal liability. For service-based and knowledge-work businesses, payroll is often the single largest operating expense, and getting it wrong triggers IRS penalties, employee turnover, and potential personal liability for business owners. Getting it right keeps employees paid accurately and on time, keeps the business compliant with federal and state tax obligations, and provides the financial data needed for budgeting and strategic planning.

The IRS estimates that approximately 40% of small and mid-sized businesses incur payroll penalties each year (cited by Paychex and others). A 2017 Workforce Institute at Kronos study found that 54% of American workers (roughly 82 million employees based on the 2017 labor force) had been affected by some type of payroll problem. ADP Research's 2025 worker survey found that 63% of US workers reported living paycheck to paycheck, making reliable and accurate payroll critical not just for the business but for the financial stability of its workforce. These aren't abstract risks. They're the practical consequences of treating payroll as an afterthought rather than a core business function.

What is the purpose of payroll?

The purpose of payroll is to pay employees accurately and on time while meeting the tax withholding, reporting, and record-keeping requirements the law demands. It also gives business owners the financial data they need to budget, forecast labor costs, and make informed hiring decisions. In short, payroll exists to keep employees paid, the business compliant, and financial planning grounded in real numbers.

Why does payroll accuracy matter for employees?

Payroll accuracy matters because employees depend on correct, timely pay to meet their financial obligations, and payroll errors damage trust quickly.

The same 2017 Workforce Institute at Kronos study found that 49% of workers will start looking for a new job after experiencing just two payroll errors. Some industry surveys suggest that as many as one in four employees would consider leaving after even a single payroll error. The study also found that 42% of workers find their pay stubs confusing to read, meaning some errors go unnoticed until they compound into larger problems at tax time. Whether employees catch errors immediately or discover them months later, the outcome is the same. Trust breaks down, and the company bears the cost of turnover, retraining, and reputation damage.

The cost of replacing an employee who leaves over payroll frustration (recruiting, hiring, onboarding, training) typically runs 50% to 200% of their annual salary, depending on role seniority and industry, according to SHRM research. Employees who trust that their pay is handled correctly are more engaged, more productive, and less likely to leave. Employees who don't trust payroll spend mental energy checking pay stubs, questioning deductions, and worrying about errors instead of focusing on their work.

How does payroll affect the employee experience?

Payroll is about more than calculating wages and distributing paychecks. The payroll experience is part of an employee's overall experience at the organization, and it shapes how they feel about the company's reliability and professionalism.

Accurate and timely payments are the foundation, but modern employees expect more. They expect instant access to digital pay stubs, real-time visibility into how their salary is calculated, mobile access to payroll information, and self-service portals where they can update their bank details, address, tax elections, and benefit enrollments without waiting for HR. Organizations that provide these features build stronger trust and reduce the volume of payroll-related HR inquiries.

Early wage access (on-demand pay) is one emerging innovation that demonstrates a commitment to employee financial well-being. Allowing employees to access earned wages before the traditional payday provides flexibility and reduces financial stress, particularly for the two-thirds of workers living paycheck to paycheck. Several major payroll providers now integrate early wage access into their platforms. Offering multiple payment methods (direct deposit, pay cards, digital wallets) also accommodates diverse employee preferences and improves satisfaction.

Why is payroll important for tax compliance?

Payroll is the primary mechanism through which businesses meet their federal and state tax obligations, including income tax withholding, Social Security and Medicare contributions (FICA), federal unemployment tax (FUTA), and state unemployment insurance (SUI). Social Security tax (6.2% employer, 6.2% employee) applies up to the annual wage base of $184,500 for 2026. Medicare (1.45% each) has no wage cap. An Additional Medicare Tax of 0.9% applies to employee wages over $200,000, which the employer must withhold but doesn't match.

IRS enforcement of payroll tax compliance

IRS enforcement of payroll tax compliance is particularly aggressive because withheld taxes are held in trust for the government. Form 941 deposit penalties escalate based on how late the deposit is. Deposits made 1 to 5 days late incur a 2% penalty. Six to 15 days later, the penalty rises to 5%. More than 15 days later, it reached 10%. If the business still hasn't paid within 10 days of receiving an IRS notice and demand, the penalty jumps to 15%. These FTD penalties are separate from failure-to-file penalties on Form 941 itself (5% per month up to 25%), and willful failure to collect or pay over trust fund taxes can trigger criminal penalties under IRC Section 7202 (up to 5 years imprisonment, with maximum fines of $250,000 for individuals and $500,000 for corporations under 18 USC §3571).

Trust Fund Recovery Penalty (TFRP)

The most serious payroll tax consequence is the Trust Fund Recovery Penalty (TFRP) under IRC Section 6672. When a business fails to remit withheld income taxes and the employee share of FICA to the IRS, the IRS can assess the TFRP against any "responsible person" who willfully failed to pay. The TFRP does not cover the employer's share of FICA. A "responsible person" is someone with significant control over financial decisions, specifically the authority to decide which creditors get paid. This typically includes business owners, officers, and directors, and can extend to employees who have actual disbursement authority (not merely those who process transactions under direction). The TFRP equals 100% of the unpaid trust fund amount. It is generally not dischargeable in bankruptcy under 11 U.S.C. § 523(a)(1)(A), and the IRS can pursue collection for the 10-year statute period under IRC Section 6502 from the date of assessment.

State payroll tax requirements

State payroll tax requirements add another layer. Each state has its own income tax withholding rules, unemployment insurance rates, and filing deadlines. Businesses operating in multiple states must comply with each state's requirements independently. States like California, New York, and Massachusetts also impose additional payroll taxes for programs like paid family leave (CA, NY, MA), disability insurance (CA, NY), and commuter transportation (NY).

Why does payroll matter for cash flow and financial planning?

Payroll is commonly 15% to 30% of total revenue for most businesses, reaching up to 50% in labor-intensive service industries like healthcare, hospitality, and professional services. This makes payroll one of the most significant line items in any operating budget, which means even small errors or timing mismatches can create real cash flow problems.

Accurate payroll data

Accurate payroll data feeds directly into financial planning, budgeting, and forecasting. When payroll records are clean and current, business owners can see exactly how much they're spending on labor, how that cost breaks down by department or project, and where labor costs are trending over time. This visibility is essential for making informed decisions about hiring, raises, benefits, and growth.

Payroll also affects cash flow timing

Most businesses run payroll on a fixed schedule (weekly, biweekly, or semi-monthly), and the payroll tax deposits follow their own calendar. Failing to account for the timing of payroll disbursements and tax deposits can leave a business short on cash at critical moments. This is especially true for businesses with seasonal revenue patterns, where payroll obligations remain constant even when income fluctuates.

Why is payroll accounting important?

Payroll accounting is the process of recording, managing, and analyzing all payroll-related transactions, and it provides the financial foundation for understanding the true cost of your workforce.

Payroll accounting goes beyond calculating net pay. It tracks gross wages, all deductions (federal, state, local taxes, benefits contributions, garnishments), employer payroll taxes (FICA match, FUTA, SUTA), and payroll liabilities (amounts owed but not yet paid). These transactions must be recorded accurately in your general ledger so that financial statements reflect the real cost of employment.

A well-organized payroll accounting system helps you assess whether it's more cost-effective to hire full-time employees, part-time workers, or contractors. It simplifies tax reporting by clearly documenting every payroll-related financial transaction. It gives you visibility into total compensation costs (not just wages, but benefits, employer taxes, and administrative costs) so you can make informed budgeting decisions. And it creates the audit trail you'll need if the IRS or a state agency requests records.

Setting up a proper chart of accounts for payroll (with separate categories for salaries, employer taxes, health insurance, retirement contributions, workers' comp, and payroll liabilities) keeps every payroll-related expense tracked consistently and makes month-end reconciliation straightforward.

Why is payroll important for legal compliance beyond taxes?

Payroll obligations extend well beyond tax withholding and include wage and hour compliance under the Fair Labor Standards Act (FLSA), proper employee classification, overtime calculations, minimum wage adherence, and record-keeping requirements.

The FLSA requires employers to pay non-exempt employees at least the federal minimum wage ($7.25 per hour, though many states set higher minimums) and overtime at 1.5 times the regular rate for hours exceeding 40 in a workweek. The "regular rate" isn't just based on hourly pay. It must include non-discretionary bonuses, shift differentials, commissions, and certain incentive pay, which is a calculation many employers get wrong.

Payroll systems must correctly track hours, apply the right overtime calculations, and maintain records for at least four years under IRS regulations (Reg. § 31.6001-1 requires four years for payroll tax records, while FLSA requires three years for payroll records and two years for supporting wage computation records). The Department of Labor's Wage and Hour Division recovered approximately $213 million in back wages in fiscal year 2022.

Employee classification also runs through payroll. Whether a worker is classified as a W-2 employee or 1099 contractor determines which payroll taxes apply, which labor protections are triggered, and which forms need to be filed. Misclassification can result in back taxes, penalties, and lawsuits. The payroll system is where these classification decisions become operational, so accuracy at the payroll level is the front line of classification compliance.

Why does worker classification run through payroll?

Correctly classifying workers as W-2 employees or 1099 independent contractors is one of the most critical payroll decisions a business makes, and misclassification triggers cascading consequences.

When a worker is classified as a W-2 employee, the employer must withhold federal income tax, withhold and match FICA (6.2% Social Security + 1.45% Medicare), pay FUTA and SUTA, provide workers' compensation coverage, and comply with FLSA wage and hour protections. When a worker is classified as a 1099 contractor, none of these obligations apply. The contractor handles their own self-employment taxes, has no wage protections, and receives no employer-provided benefits.

The IRS, DOL, and state agencies actively pursue misclassification because the revenue and labor protection gaps are significant. Misclassification can result in back taxes for all periods the worker was misclassified, IRS penalties under IRC Section 3509 (1.5% of wages for income tax plus 20% of employee FICA if 1099s were filed; the employer still owes 100% of employer FICA and FUTA), state-level penalties (California Labor Code § 226.8 imposes $5,000 to $15,000 per violation for willful misclassification), and potential FLSA back-pay liability for unpaid overtime. Payment frequency also matters. How often you pay employees (weekly, biweekly, semi-monthly, or monthly) is often dictated by state law, and failing to comply with state pay frequency requirements is a separate compliance violation.

Why does payroll affect company reputation?

A company's reputation as an employer depends heavily on whether it pays people correctly and on time, and payroll failures spread quickly through employee networks, review sites, and word of mouth.

Negative payroll experiences show up on employer review platforms like Glassdoor and Indeed. Candidates researching potential employers routinely check these reviews, and patterns of payroll complaints (late pay, incorrect deductions, tax filing errors) signal organizational dysfunction. For small and mid-sized businesses competing for talent against larger employers, payroll reliability is a baseline expectation that can't be failed without consequences.

On the positive side, businesses that handle payroll well (accurate pay, clear pay stubs, transparent deductions, responsive corrections when errors occur) build a foundation of trust that supports retention, engagement, and employer brand strength. Bonuses and benefits administered through payroll also reinforce that employees are valued. A well-timed bonus or a competitive benefits package tells employees they're important to the organization, which directly affects motivation and productivity.

How can payroll data drive strategic business decisions?

Payroll generates enormous amounts of data every cycle, and most businesses underutilize that data for strategic decision-making.

Businesses can use payroll data to discover inequalities in compensation structures (pay gaps by gender, role, or department), detect turnover and absenteeism patterns (do employees leave more frequently after certain pay events?), assess whether compensation packages are competitive against market benchmarks, identify departments with excessive overtime (signaling understaffing or poor scheduling), and forecast future payroll costs based on hiring plans and raise cycles.

The only requirement for using payroll data strategically is centralizing it in a single system that provides full transparency and easy reporting. When payroll data is scattered across spreadsheets, disconnected systems, or outsourced providers without reporting access, the strategic value is lost. Modern payroll platforms include analytics dashboards that surface these insights automatically.

Should you use manual or automated payroll?

Manual payroll (spreadsheets, hand calculations) works for very small businesses with simple pay structures, but it becomes increasingly risky as headcount grows.

Payroll software matters because it automates calculations, tax filings, and record-keeping that would otherwise take hours of manual work each pay cycle. It cuts down on errors, keeps up with changing tax rates automatically, and gives employees self-service access to pay stubs and tax forms without HR having to step in.

Factor | Manual Processing | Automated Systems |

Error rate | High. Manual data entry and calculations increase mistakes considerably. | Low. Studies cite error reductions of 30% to 50% with payroll automation. |

Processing time | Lengthy. Requires manual calculations and verification each cycle. | Industry data suggests automation cuts processing time by 25% or more, depending on starting point. |

Compliance updates | Manual tracking of tax law changes. Easy to miss updates. | Automatic updates for tax rates and regulations. |

Employee access | Limited. Requires HR intervention for pay stubs and information. | Self-service portals available 24/7. |

Scalability | Difficult. Each new employee adds proportional workload. | Scales without proportional cost increases. |

Cost structure | Lower initial cost but higher long-term expenses from errors and time. | Higher initial investment with ongoing savings. |

Industry data suggests each payroll error costs approximately $291 to correct (per the EY/Paycom December 2022 analysis), including processing time, administrative workload, and compliance adjustments. For a company making 15 corrections per pay period (the average found in that same analysis), that's approximately $4,365 per cycle in correction costs alone. Automated systems that prevent even half of those errors pay for themselves quickly.

How can you ensure payroll is handled correctly?

The best way to ensure payroll accuracy and compliance depends on your company's size, complexity, and internal resources. Businesses generally choose from four options, each with different costs, control, and compliance trade-offs.

For businesses with straightforward domestic payroll

For businesses with straightforward domestic payroll (single state, W-2 employees only), a dedicated payroll system like Gusto, QuickBooks Payroll, or ADP Run can automate calculations, handle tax filings, and generate year-end forms with minimal manual effort. For businesses operating in multiple states or with more complex needs (garnishments, multiple pay rates, benefits administration), a full-service payroll provider or PEO offers hands-off compliance management at the cost of some employer control. CPEOs specifically can assume federal employment tax liability under IRC Section 3511, which provides an additional layer of protection against payroll tax risk.

For businesses expanding internationally

For businesses expanding internationally, payroll importance multiplies because each country has its own tax codes, social contribution rates, mandatory benefits, and filing deadlines. An EOR can handle multi-country payroll compliance without requiring the business to establish local entities. EOR services typically include payroll processing, tax withholding, statutory benefits administration, and employment contract management for each country, which reduces the cost and complexity of global expansion.

For businesses that want to outsource entirely

Professional payroll providers bring specialized expertise, dedicated compliance monitoring, and advanced automation tools that most businesses can't maintain internally. Outsourcing transfers much of the compliance risk to the provider, frees internal teams to focus on revenue-generating activities, and scales effortlessly as headcount grows. Internal payroll processing time varies widely. Small businesses with automation may spend only a few hours per pay period, while mid-sized businesses running manual payroll in multiple states can exceed 10 hours per cycle. Outsourcing eliminates most of that time commitment.

What happens if you get payroll wrong?

Getting payroll wrong can result in IRS deposit penalties (2% to 15% of the late amount), failure-to-file penalties (5% per month up to 25%), state tax penalties, employee lawsuits for wage violations, back pay liability, and personal liability under the Trust Fund Recovery Penalty. Beyond financial consequences, payroll errors cause employee turnover, damage to company's reputation, and loss of trust. Each error costs approximately $291 to correct in administrative time and processing alone (per EY/Paycom data).

Is payroll the biggest expense for most businesses?

For service-based and knowledge-work businesses, payroll and related labor costs are typically the largest operating expense, commonly representing 15% to 30% of total revenue and reaching up to 50% in labor-intensive industries. Even well-established businesses with mature financial systems keep a close eye on this number, since payroll tends to stay one of the largest and most closely watched expense categories as a company grows. For manufacturers, retailers, and distributors, the cost of goods sold (raw materials, inventory) often exceeds payroll. Regardless of industry, payroll is significant enough that accuracy directly affects profitability and cash flow.

How often should payroll be audited?

Payroll experts recommend auditing payroll at least quarterly, with a full annual audit at year-end before W-2s and tax returns are filed. There's no regulatory requirement for a specific audit frequency, but quarterly reviews catch errors before they compound, including incorrect tax rates, misapplied deductions, and classification mistakes. Year-end audits reconcile total wages, total taxes withheld, and total employer contributions against what was reported to the IRS and state agencies.

Can you be personally liable for payroll tax errors?

Yes, under the Trust Fund Recovery Penalty (IRC Section 6672), any "responsible person" with significant control over financial decisions who willfully fails to remit withheld payroll taxes can be held personally liable for 100% of the unpaid trust fund amount. This covers withheld income taxes and the employee share of FICA (but not the employer's FICA share). The TFRP is generally not dischargeable in bankruptcy, and the IRS can pursue collection for the 10 years following assessment under IRC Section 6502.

What is the difference between payroll accounting and regular accounting?

Payroll accounting specifically deals with recording and managing payroll transactions (wages, deductions, taxes, benefits), whereas regular accounting covers all financial transactions of a business. Payroll accounting requires its own chart of accounts, its own reconciliation process, and its own compliance calendar because the penalties for payroll-specific errors (TFRP, FTD penalties, wage-and-hour violations) are different from and often more severe than general accounting errors.

Can payroll be outsourced?

Yes, many businesses outsource payroll to third-party providers to save time, reduce errors, and ensure compliance. Outsourcing options range from basic payroll processing services (calculations and direct deposits) to full-service providers that handle tax filing, benefits administration, workers' comp, and compliance monitoring. For businesses with international employees, an EOR can handle country-specific payroll requirements without requiring entity setup.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations