Payroll compliance: requirements, consequences & solutions

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll compliance is the process of following all federal, state, and local laws governing how employers calculate wages, withhold and deposit taxes, classify workers, maintain records, and issue payments on time. Employers that fail to comply face graduated IRS failure-to-deposit penalties (2% to 15%), personal liability under the Trust Fund Recovery Penalty (IRC § 6672), and DOL back-wage recovery - $273 million recovered for approximately 152,000 workers in FY 2024. Approximately 53% of companies have been penalized for payroll noncompliance in the last five years, and noncompliance averages over $845 per employee per year in total costs.

- Penalty rate for noncompliance: 53% of companies have been penalized for payroll noncompliance in the last five years (Alight's 2024 Company Payroll Complexity Report).

- Cost of noncompliance: Over $845 per employee per year when factoring in fines, back wages, penalties, and internal remediation.

- Small business payroll penalties: Approximately 40% of small businesses incur payroll penalties each year (IRS data via Paychex).

- Errors per pay period: Organizations using traditional payroll processes average approximately 15 errors per pay period at roughly $291 per error (EY, December 2022).

- 2026 Social Security wage base: $184,500. 401(k) elective deferral limit: $24,500 ($11,250 super catch-up for ages 60-63 under SECURE 2.0).

Key 2026 payroll compliance updates

Employers should be aware of the following changes for the 2026 tax year. Social Security wage base increased to $184,500. Health FSA contribution limit increased to $3,400, with a maximum carryover of $680 (per IRS Rev. Proc. 2025-32). HSA contribution limits for 2026 are $4,400 (individual) and $8,750 (family). 401(k) elective deferral limit increased to $24,500 ($8,000 catch-up for employees aged 50 and over; $11,250 "super catch-up" for ages 60-63 under SECURE 2.0). Beginning in 2026, employees who earned more than $150,000 in 2025 must make catch-up contributions as Roth (after-tax) per SECURE 2.0. FICA threshold for household employees increased to $3,000.

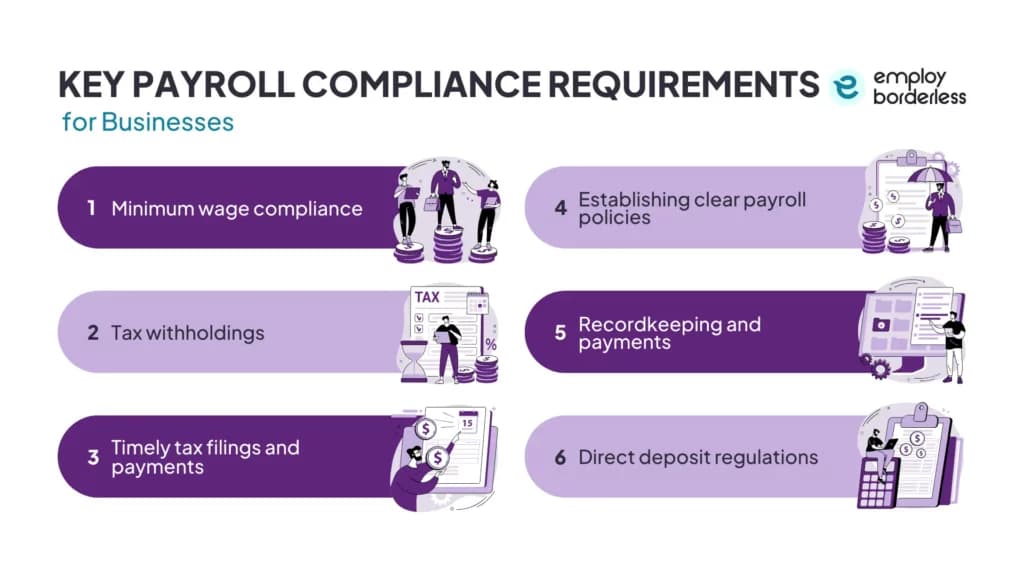

What are the federal requirements for payroll compliance?

Federal payroll compliance covers eight areas. Tax withholding and deposit, wage and hour rules, worker classification, equal pay, benefits reporting, recordkeeping, form filing, and employment eligibility verification. Each area has its own enforcement agency, penalty structure, and audit triggers.

Tax withholding and deposit requirements

Employers must withhold federal income tax (based on employee W-4 elections and IRS Publication 15-T tables), Social Security tax (6.2% on wages up to $184,500 in 2026), and Medicare tax (1.45% on all wages, plus 0.9% Additional Medicare Tax on employee wages above $200,000, which is employee-paid only). The employer matches 6.2% Social Security and 1.45% Medicare. FUTA is 6.0% on the first $7,000 per employee (0.6% effective after the standard credit, higher in credit reduction states).

Deposit timing depends on your lookback period liability. Employers with $50,000 or less in total employment taxes during the lookback period (12 months ending the preceding June 30) are monthly depositors and must deposit by the 15th of the following month. Above $50,000, the employer is a semi-weekly depositor. Taxes on wages paid Wednesday through Friday must be deposited by the following Wednesday. Taxes on wages paid Saturday through Tuesday must be deposited by the following Friday. All federal tax deposits must be made through EFTPS.

Wage and hour compliance (FLSA)

The Fair Labor Standards Act sets the federal minimum wage ($7.25/hour, unchanged since 2009), overtime requirements (1.5x regular rate for hours exceeding 40 per workweek for non-exempt employees), and the salary threshold for exempt status ($35,568/year or $684/week). The DOL's 2024 rule that would have raised this threshold to $58,656 was vacated by a federal court on November 15, 2024. State thresholds exceed the federal level in several states, including California ($70,304 in 2026), New York ($60,406 to $64,350 depending on region), Washington ($80,168 for small employers with 1-50 employees; higher for 51+ employees), Alaska, and Maine.

The FLSA's "regular rate" calculation is a frequent compliance failure point. Non-discretionary bonuses (production bonuses, attendance bonuses, quarterly incentives), commissions, and shift differentials must be included in the regular rate for overtime calculation purposes under Section 7(e). Many employers fail to include these, leading to systematic overtime underpayment that DOL WHD enforcement routinely flags.

California also requires daily overtime (1.5x over 8 hours, 2x over 12 hours per day). New York Labor Law § 191 requires weekly pay for manual workers, with recent litigation (Vega v. CM & Associates Construction Management, LLC in the First Department, 2019, and Grant v. Global Aircraft Dispatch in the Second Department, 2024, creating a department split) generating significant class action exposure for employers paying manual workers biweekly instead of weekly.

Equal Pay Act

The Equal Pay Act requires employers to provide equal pay to men and women who perform substantially similar jobs in the same workplace. All forms of compensation are covered, including salaries, bonuses, overtime pay, stock options, life insurance, and profit-sharing. Violations can result in EEOC complaints and civil lawsuits. Employers can reduce exposure by auditing wage rates annually, using industry income averages as benchmarks, documenting all pay decisions, and making compensation data visible across the organization.

Worker classification

The IRS uses a common-law test examining behavioral control, financial control, and the type of relationship to determine whether a worker is an employee or independent contractor. The DOL's 2024 independent contractor rule (effective March 11, 2024) adopted a six-factor economic-reality test, but DOL stopped enforcing it in May 2025 (Field Assistance Bulletin 2025-1, instructing field staff to revert to the pre-2024 framework from Fact Sheet #13) and formally proposed to rescind and replace it on February 26, 2026 with a 2021-style "core factors" framework focused on control and opportunity for profit or loss. The 2024 Rule remains technically in effect for private litigation pending the formal rescission. A worker can be correctly classified under one test but misclassified under the other. The complexity of classification rules is one of the reasons many employers turn to automated payroll systems that flag classification discrepancies.

States add their own tests. California's AB5 (effective January 1, 2020, codifying the ABC test from Dynamex Operations West v. Superior Court) imposes misclassification penalties under California Labor Code § 226.8 of $5,000 to $15,000 per violation for willful misclassification, or $10,000 to $25,000 per violation if there's a pattern or practice of willful misclassification. The National Employment Law Project has estimated, based on state-level enforcement audits, that 10% to 30% of employers misclassify at least some workers.

IRC Section 3509 provides reduced-rate federal relief for non-willful misclassification. If 1099s were filed, the reduced rates are 1.5% of wages for income tax withholding plus 20% of the employee's share of FICA, plus full employer FICA. If 1099s were not filed, rates double to 3% of wages plus 40% of employee FICA. Section 3509 is not available if the employer had a reasonable basis for classification under Section 530 of the Revenue Act of 1978 (in which case no reclassification liability applies) or if the misclassification was willful (which triggers criminal penalties under IRC § 7201 and § 7202).

ACA reporting

Employers reaching 50 full-time equivalent (FTE) employees trigger Applicable Large Employer (ALE) status under the ACA. ALEs must file Form 1095-C (and transmittal Form 1094-C) reporting health coverage offers to employees. The 2026 Section 4980H penalties per IRS Rev. Proc. 2025-26 are $3,340/year per full-time employee (minus 30) if minimum essential coverage isn't offered to at least 95% of full-time employees, or $5,010/year per employee receiving a premium tax credit if coverage is unaffordable or doesn't meet minimum value.

Recordkeeping and form filing

The IRS requires employers to keep payroll records for at least 4 years (per 26 CFR § 31.6001-1). The FLSA requires 3 years for payroll records and 2 years for time cards and work schedules (per 29 CFR § 516.5-516.6). I-9 employment eligibility verification forms have a separate retention rule. Employers must retain I-9s for 3 years after the date of hire, or 1 year after the date of termination, whichever is later. This often exceeds the standard payroll records retention period.

Employers with 10 or more information returns (W-2s, 1099s, aggregated across form types) must file electronically per Treasury Decision 9972. W-2s and W-3 must be filed by January 31. Form 941 is filed quarterly. Form 940 (FUTA) is filed annually. For returns required to be filed in 2026 (tax year 2025), late-filing penalties are $60 per form if filed within 30 days of the deadline, $130 per form if filed by August 1, and $340 per form if filed after August 1 or not filed. Intentional disregard triggers a $680 per form penalty with no annual cap.

What are the state and local requirements?

State payroll compliance adds layers of complexity that no federal rule covers.

Requirement | What it covers | Key details |

State income tax withholding | 9 states have no wage income tax (AK, FL, NV, NH, SD, TN, TX, WA, WY). NH never taxed wages; its remaining Interest & Dividends tax is eliminated effective January 1, 2027. WA does not tax wages but imposes a 7% capital gains tax on long-term gains above ~$262,000. | Employers must register, withhold, and remit in every state where employees work, subject to reciprocity agreements and convenience rules. |

SUTA | State unemployment tax. Rates vary by state and employer experience rating (0.5% to 7%+). | New employers get a default rate until experience rating applies. Taxable wage bases vary ($7,000 to $62,500+). |

PFML | Employer and/or employee contributions required. | Current programs in RI, CA, NJ, NY, MA, WA, CT, OR, CO. Delaware and Maryland contributions began 2025 with benefits effective 2026. Maine and Minnesota effective 2026. |

Pay frequency | States mandate minimum pay frequencies. | CA Labor Code § 204 requires semi-monthly pay with specific deadlines: wages for the 1st-15th must be paid by the 26th; wages for the 16th-end-of-month by the 10th of the following month. NY § 191 requires weekly for manual workers. |

Reciprocity agreements | Allow withholding in employee home state instead of work state. | PA has agreements with NJ, OH, VA, WV, MD, IN. Other states have similar arrangements. |

Convenience of employer rules | Require withholding in employer state even for remote workers. | Eight states impose some form of this rule. Full rules: Alabama, Delaware, Nebraska, New York, Pennsylvania. Reciprocal rules (only apply if worker's home state has a similar rule): Connecticut, New Jersey. Limited (nonresident managerial workers only): Oregon. |

A single remote hire in a new state triggers registration, withholding, SUTA, and labor law compliance in that state. Multi-state payroll is the number-one compliance complexity driver, especially since remote work expanded the geographic footprint of many employers.

What are the international payroll compliance requirements?

A one-size-fits-all approach to payroll doesn't work for employers with international operations. Even if the organization's headquarters is based in the United States, it must abide by the local employment and tax laws where its employees are working. Key international regulations that affect payroll processing include the EU Working Time Directive (which limits weekly working hours and sets minimum paid leave standards, with member-nation amendments), the Labor Law of the People's Republic of China (covering employment contracts, wages, working hours, and overtime), the UAE Wages Protection System (requiring registration with the Ministry of Human Resources and payment through approved financial institutions by established deadlines), the UK Employment Rights Act (covering employment contracts, dismissal procedures, and parental leave), and Japan's Labor Standards Act (covering minimum wage, working hours, overtime, and annual leave).

For companies hiring in countries where they don't have a legal entity, an EOR (Employer of Record) handles local payroll compliance, tax withholding, statutory benefits, and labor law requirements in each country. This eliminates the need to establish a local entity and build in-country compliance expertise from scratch.

What are the consequences of non-compliance?

Payroll non-compliance consequences escalate from financial penalties through personal liability to criminal prosecution. Beyond the regulatory consequences, payroll errors directly damage workforce trust. Approximately one in three US workers has left a company due to payroll problems, and nearly 49% of employees start searching for new jobs after experiencing just two payroll errors. With a majority of Americans living paycheck to paycheck (per LendingClub/PYMNTS research, approximately 60% to 66% as of 2024-2025), even a single late or inaccurate payment can leave employees unable to cover bills or handle emergencies.

Consequence | Authority | Details |

Late deposit penalties | IRS | 2% if 1-5 days late, 5% if 6-15 days late, 10% if 16+ days late, 15% if not deposited within 10 days of IRS notice. |

Trust Fund Recovery Penalty | IRS (IRC § 6672) | 100% of unpaid trust fund taxes (withheld income tax + employee FICA) assessed personally against any responsible person. The TFRP equals (not adds to) the unpaid trust fund taxes; it is the IRS mechanism for collecting from individuals when a business fails to remit. |

W-2/1099 late filing (2026) | IRS | $60/form within 30 days, $130/form by August 1, $340/form after August 1. Intentional disregard triggers $680/form with no annual cap. |

State misclassification | State labor departments | CA Labor Code § 226.8 imposes $5,000-$15,000 per violation (willful), or $10,000-$25,000 per violation (pattern or practice). |

FLSA overtime violations | DOL WHD | Back wages + liquidated damages (equal to back wages). DOL recovered $273M in back wages and damages for ~152,000 workers in FY 2024. |

ACA penalties (2026) | IRS (IRC § 4980H) | $3,340/year per FTE (minus 30) for no MEC, or $5,010/year per employee receiving PTC. Per Rev. Proc. 2025-26. |

Federal misclassification (non-willful) | IRS (IRC § 3509) | 1.5% wages + 20% employee FICA (1099s filed), or 3% + 40% (not filed). Full employer FICA still owed. |

Federal misclassification (willful) | IRS/DOJ (§ 7201/§ 7202) | Criminal penalties. Fines and imprisonment. Section 3509 relief not available. |

What are the most common payroll compliance mistakes?

Even well-intentioned employers make payroll compliance mistakes that trigger penalties, back wages, and audit exposure. Research shows employers average at least 15 payroll errors per pay period, and over half of payroll teams still use error-prone spreadsheets instead of dedicated payroll technology.

Misclassifying employees and independent contractors: Worker classification errors trigger back taxes, benefit disputes, and retroactive penalties at both federal and state levels. The distinction is easily blurred, and a worker can be correctly classified under one test (IRS common-law) but misclassified under another (DOL economic reality). If in doubt about a worker's status, employers should submit Form SS-8 to the IRS.

Failing to include all compensation in the regular rate: Non-discretionary bonuses, commissions, and shift differentials must be included in the FLSA regular rate calculation for overtime purposes. Many employers exclude these, resulting in systematic overtime underpayment that DOL WHD enforcement routinely flags.

Missing tax deposit and filing deadlines: Late deposits trigger graduated IRS penalties from 2% to 15%. Late W-2/1099 filings trigger per-form penalties that scale with delay. A payroll compliance calendar with automated reminders prevents most deadline failures.

Ignoring pay equity requirements: Inconsistent pay practices or unexplained salary differences can expose businesses to Equal Pay Act violations, EEOC complaints, and reputational damage. Regular payroll reviews help identify and address pay gaps before they escalate.

Incomplete or disorganized records: Scattered pay stubs, outdated employee records, and missing I-9s become a serious liability during audits. IRS requires 4 years of payroll records, FLSA requires 3 years for basic records and 2 years for supporting documents. Records should be current, organized, and accessible at all times.

Workers' compensation classification errors: Insurance premiums for workers' comp are based partly on employee classifications and total payroll. Most states require insurance carriers to conduct annual audits. Incorrect payroll records or job classification errors can result in additional premium obligations. Conducting an internal audit before the insurance company audit helps catch discrepancies.

What are the best practices for payroll compliance?

Strong payroll compliance requires a structured approach that combines internal controls, technology automation, and expert oversight. Building these practices into your payroll system reduces risk and creates a process you can rely on.

Build a compliance calendar: Map every federal, state, and local deadline for the year. This includes quarterly 941 filings, annual W-2/1099 distribution (January 31), annual 940 filing, state SUTA quarterly returns, and state-specific deadlines for PFML contributions, pay data reporting, and new hire reporting. Assign ownership for each deadline and set automated reminders.

Automate payroll processing: Payroll software automates three high-risk compliance areas. Tax calculation (automatic rate updates when federal, state, and local rates change), deposit timing (automated EFTPS payments that meet deadlines), and form generation (W-2, 1099, 941, 940 populated from payroll data). Per Deloitte's Global Payroll Benchmarking Survey, automating payroll can reduce errors by up to 50% and processing time by 25%. The cost of payroll software ($30 to $150/month base + $5 to $20/employee) is typically offset by the reduction in correction costs ($291 per error) and penalty avoidance.

Classify workers correctly from day one: Determine exempt vs non-exempt status under FLSA, employee vs independent contractor status under both IRS and DOL tests, and state-specific classification requirements. Misclassification is the fastest path to compounding penalties because it triggers liability across multiple tax types simultaneously.

Conduct regular internal audits: At minimum, conduct a full payroll compliance audit annually. Quarterly spot-checks of tax deposits, employee classifications, overtime calculations, and I-9 retention catch errors before they compound. Only about 29% of companies audit their payroll processes regularly (per OneSourceVirtual analysis), which helps explain the high noncompliance rate. Trigger additional audits after expanding into a new state, completing an acquisition, reclassifying workers, or migrating payroll systems.

Keep detailed, accurate records: Make sure new hires submit all required documents. Review them carefully for inverted numbers, incomplete fields, and incorrect dates. File records so they can be easily accessed by both HR and payroll departments. Cloud-based payroll platforms centralize data and simplify audit workflows.

Stay current with regulatory changes: Tax laws, labor regulations, and payroll rules at federal, state, and international levels are constantly evolving. Subscribe to IRS e-News, DOL alerts, and state labor department updates. Designate one team member to review updates and flag changes affecting your organization. What was compliant last year may not meet requirements today.

How can outsourcing payroll help with compliance?

Outsourcing shifts the compliance burden from your internal team to a provider whose core business is staying current with tax law, labor regulations, and filing deadlines across every jurisdiction you operate in. For a complete overview, see our guide to payroll outsourcing.

Three models exist for outsourcing compliance. Payroll software with self-service (Gusto, ADP Run, Paychex Flex) handles processing and filing while the employer manages inputs. Full-service payroll providers (ADP, Paychex, Paycor) add dedicated support, compliance monitoring, and audit assistance. PEO arrangements add co-employment with pooled benefits, workers' comp administration, and broader HR compliance support.

The compliance advantage of outsourcing is strongest for multi-state employers, where each new state adds registration, withholding, SUTA, and labor law requirements. A provider processing payroll across all 50 states already has those registrations and rate tables in place. Estimates of outsourcing cost savings vary widely, typically ranging from 18% to 35% depending on company size and which costs are included in the comparison (software licensing, training costs, penalty avoidance, and staff time freed for revenue-generating activities). For growing businesses, understanding payroll importance and choosing the right system are the first steps toward sustainable compliance.

What is the most common payroll compliance violation?

Late tax deposits and wage-hour violations (missed overtime, meal and rest break violations) are the most frequent payroll compliance violations. Worker misclassification is less frequent but typically the highest-impact violation because it triggers back taxes, interest, and penalties at both federal and state levels across multiple tax types simultaneously.

How often should I audit payroll for compliance?

At minimum, conduct a full payroll compliance audit annually. Quarterly spot-checks of tax deposits, employee classifications, overtime calculations, and I-9 retention catch errors before they compound. Trigger additional audits after expanding into a new state, completing an acquisition, reclassifying workers, migrating payroll systems, or changing benefits enrollment.

What if I have international employees?

US payroll compliance rules apply only to domestic employees. For employees in countries where you don't have a legal entity, an EOR (Employer of Record) handles local payroll compliance, tax withholding, statutory benefits, and labor law requirements in each country. Each country has its own employment laws, social security systems, tax obligations, and payment rules, making in-house international compliance impractical for most companies.

Does payroll software handle all compliance requirements?

No. Payroll software automates calculations, tax filing, and deposit timing, but it requires proper setup, regular updates, and informed human oversight. Software handles the mechanical aspects (tax rates, withholding formulas, form generation) but doesn't address judgment-dependent decisions like whether a worker is an employee or contractor, whether non-discretionary bonuses should be included in the FLSA regular rate calculation, or how to apply state-specific rules for remote workers in convenience-of-employer jurisdictions. Software is a tool, not a complete compliance solution.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Ready to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations