10 essential payroll components every business should know

Robbin Schuchmann

Co-founder, Employ Borderless

The components of payroll are the individual elements that make up an employee’s total compensation, from gross earnings through employer-side costs and deductions down to net pay. Every payroll cycle involves calculating four categories of components. Earnings are what the employee earns. Employer costs are what the company pays on top of earnings. Employee deductions are what are subtracted from gross pay. And net pay is what the employee actually takes home.

Understanding payroll components matters because errors in any single element can trigger compliance problems. Misapplying a tax rate, miscalculating overtime, or forgetting a pre-tax deduction doesn’t just produce a wrong paycheck. It creates a tax filing discrepancy that the IRS, state tax authorities, or local agencies will eventually flag. Staying aligned with payroll regulations and compliance requirements across all jurisdictions starts with understanding how each component works.

This guide breaks down every payroll component in the order they appear in the gross-to-net calculation, explains the US-specific tax rates that apply in 2026, and shows how each component fits into the total cost of employment.

What are the gross pay components?

Gross pay is the total amount an employee earns before any deductions, including base salary or hourly wages, overtime, bonuses, commissions, allowances, expense reimbursements, and PTO compensation. It’s the starting point for every payroll calculation. All tax withholdings, benefit deductions, and employer-side costs are calculated from gross pay.

Base salary or hourly wages

Base salary is the fixed amount an employee earns per pay period as agreed in their employment contract, while hourly wages are calculated by multiplying hours worked by the employee’s hourly rate. For salaried employees, the base pay stays consistent each pay period. For hourly employees, it fluctuates based on actual hours worked. Under the Fair Labor Standards Act (FLSA), the federal minimum wage is $7.25 per hour, though most states set higher minimums.

The FLSA exempts employees who meet specific duties tests and earn a salary of at least $684 per week ($35,568 per year) from overtime requirements. This is the 2019 federal threshold, which remains in effect after the 2024 DOL rule raising it to $1,128/week was vacated nationwide by the U.S. District Court for the Eastern District of Texas in November 2024. Some states set higher thresholds (California, New York, Washington, Colorado, Alaska, and Maine all exceed the federal level), so employers must apply whichever threshold is higher.

Overtime pay

Overtime pay is additional compensation owed to non-exempt employees who work more than 40 hours in a workweek, calculated at a minimum of 1.5 times their regular hourly rate under the FLSA. Exempt employees (typically salaried workers meeting specific salary and duties tests) aren’t entitled to overtime under federal law. Some states have stricter overtime rules. California, for example, requires daily overtime for hours worked beyond 8 in a single day and double time for hours beyond 12. Getting overtime calculations right is one of the fastest ways to improve payroll accuracy.

Bonuses and commissions

Bonuses are one-time or periodic payments made on top of base pay, while commissions are performance-based payments tied to sales or revenue targets. Both are included in gross pay and are subject to federal income tax, Social Security, and Medicare withholding. The IRS treats bonuses as supplemental wages, which employers can withhold at a flat 22% federal rate (on the first $1 million in supplemental wages per calendar year) or combine with regular wages using the employee’s W-4 information. Once an employee’s supplemental wages exceed $1 million in a year, the excess must be withheld at the highest federal income tax rate (37%).

Allowances and stipends

Allowances are additional payments given to employees for specific purposes like housing, transportation, or meals. In the US, most cash allowances are taxable income. Some exceptions exist for accountable plan reimbursements (where the employee provides documentation and returns any excess), qualified transportation fringe benefits (commuter and parking benefits, up to monthly IRS limits), qualified moving expenses for Armed Forces members, and working condition fringe benefits. General allowances added to paychecks without documentation requirements are treated as regular wages for tax purposes.

Expense reimbursements

When employees pay for business-related expenses with their own money, they are typically entitled to reimbursement. Whether these reimbursements are taxable depends on the plan structure. Under an accountable plan (the employee provides documentation, the expense has a business connection, and any excess is returned), reimbursements are not taxable and don’t appear on the W-2. Under a non-accountable plan, reimbursements are treated as taxable wages subject to all withholdings. Common reimbursable expenses include travel, meals, lodging, and professional development costs. When processing reimbursements through payroll, make sure the plan structure is correctly configured to avoid turning non-taxable reimbursements into taxable income.

Paid time off compensation

PTO compensation includes wages paid for vacation, sick leave, personal days, and holidays when the employee isn’t working. There’s no federal law requiring paid time off in the US, but more than 20 states and Washington DC now mandate paid sick leave for employees. Most employers also offer vacation and personal time as part of their benefits package. PTO pay is included in gross pay and taxed the same as regular wages. When employees separate from the company, some states require payout of accrued but unused PTO.

What are the employer-side payroll costs?

Employer-side payroll costs are expenses the company pays on top of the employee’s gross pay that don’t appear on the employee’s paycheck, including the employer’s share of FICA taxes, FUTA, state unemployment insurance, and workers’ compensation. These costs add approximately 10% to 15% to gross pay for most US employers before factoring in voluntary benefits like health insurance and retirement plan matching, which can bring the fully loaded cost to 25% to 40% above base salary.

FUTA (federal unemployment tax)

FUTA is a federal unemployment tax paid entirely by the employer at a rate of 6.0% on the first $7,000 of each employee’s wages per year, with a maximum credit of 5.4% for timely state unemployment tax payments, resulting in a net rate of 0.6% for most employers. That works out to $42 per employee per year at the standard net rate of 0.6%.

Employers in credit reduction states pay higher effective FUTA rates because their states haven’t repaid federal unemployment loans. Credit reduction states are recomputed annually. Building a compliance framework for payroll that accounts for these state-by-state variations is essential for multi-state employers.

State unemployment insurance (SUI/SUTA)

State unemployment insurance is an employer-paid tax that funds state unemployment benefits programs, with rates and wage bases varying by state. Each state sets its own tax rate schedule based on the employer’s experience rating and the solvency of the state’s unemployment trust fund. Rates typically range from under 1% for employers with clean claims histories to 10% or higher for employers with significant unemployment claims. The taxable wage base ranges from $7,000 (matching the FUTA minimum in states like California) to $78,200 in Washington for 2026.

Some states also require employer contributions to state disability insurance (SDI) or paid family and medical leave (PFML) programs. California, New York, New Jersey, Rhode Island, Hawaii, Washington, Massachusetts, Connecticut, Colorado, Oregon, Delaware, Maine, Maryland, and DC have mandatory SDI or PFML programs, with several additional states enacting programs in recent years.

Workers’ compensation insurance

Workers’ compensation is employer-funded insurance that covers medical expenses and lost wages for employees injured on the job. Most states require employers to carry workers’ comp coverage. The cost varies by industry and job classification, with higher-risk industries like construction paying significantly more than office-based roles. Rates are typically expressed as a cost per $100 of payroll.

What are the payroll deductions?

Payroll deductions are amounts subtracted from an employee’s gross pay, divided into mandatory deductions (required by law) and voluntary deductions (elected by the employee). The order in which deductions are applied matters because pre-tax deductions reduce taxable income while post-tax deductions don’t.

Federal income tax withholding

Federal income tax is withheld from each paycheck based on the employee’s W-4 form, which indicates their filing status, number of dependents, and any additional withholding amounts. The US uses a progressive tax system with rates ranging from 10% to 37% across multiple income brackets. Employers use IRS Publication 15-T (Federal Income Tax Withholding Methods) to calculate the correct withholding for each pay period.

Employee FICA taxes

Employees pay 6.2% of their wages for Social Security (on earnings up to $184,500 in 2026) and 1.45% for Medicare (on all earnings), matching the employer’s contribution. Employees earning more than $200,000 per year also pay an Additional Medicare Tax of 0.9%, bringing their total Medicare rate to 2.35% on wages above that threshold. This additional tax is employee-only. The employer doesn’t match it. Employers are required to withhold the 0.9% once an employee’s wages exceed $200,000 regardless of filing status, but the actual tax liability threshold varies. It’s $200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately. Employees reconcile the difference on their tax return.

State and local income taxes

Most states impose a state income tax that employers must withhold from employee paychecks, though nine states (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming) have no state income tax on wages. Some cities and counties also impose local income taxes. New York City, for example, imposes a resident income tax ranging from 3.078% to 3.876%. Ohio has municipal income taxes in hundreds of cities. Employers must withhold the correct state and local taxes based on where the employee works and, in some cases, where they live. Some states have reciprocal agreements that relieve the work-state from requiring withholding for non-residents who live in the reciprocal state. Under these agreements, the employee files a non-residence certificate with the work state, and the employer withholds only for the employee’s state of residence.

Pre-tax deductions

Pre-tax deductions are amounts subtracted from gross pay before federal income tax is calculated, which reduces the employee’s taxable income. However, not all pre-tax deductions receive the same treatment for FICA purposes. This distinction matters for accurate payroll processing.

Section 125 cafeteria plan deductions (health insurance premiums, FSA contributions, and HSA contributions made through a cafeteria plan) are exempt from both federal income tax and FICA taxes (Social Security and Medicare). This means they reduce the employee’s tax bill on both fronts.

Traditional 401(k) contributions are exempt from federal income tax but are still subject to FICA. The employee’s 401(k) deferral reduces their income tax withholding, but Social Security and Medicare taxes are still calculated on the full wages before the 401(k) deduction. For 2026, employees under 50 can contribute up to $24,500 per year (per IRS Notice 2025-67). Employees aged 50 and older can add a catch-up contribution of $8,000, and employees aged 60 to 63 qualify for a super catch-up of $11,250 under SECURE 2.0. This distinction is one of the most common sources of payroll errors. If your payroll system treats 401(k) contributions the same as Section 125 deductions for FICA purposes, you’ll under-withhold Social Security and Medicare taxes and create a liability with the IRS. The role of audits in payroll is to catch these FICA treatment errors before they become IRS liabilities.

Post-tax deductions

Post-tax deductions are amounts subtracted from pay after taxes have been calculated, meaning they don’t reduce the employee’s taxable income. Common post-tax deductions include Roth 401(k) contributions, some life insurance premiums (employer-provided coverage over $50,000 is treated as taxable income), union dues, wage garnishments (court-ordered deductions for child support, alimony, or creditor judgments), and charitable contributions through payroll.

Deduction Type | Reduces Income Tax? | Reduces FICA? | Notes |

Health insurance (Section 125) | Yes | Yes | Must be through a Section 125 cafeteria plan |

FSA contributions | Yes | Yes | Through Section 125 plan |

HSA contributions (via payroll) | Yes | Yes | Only when through Section 125 plan |

Traditional 401(k) | Yes | No | Still subject to Social Security and Medicare |

Roth 401(k) | No | No | Post-tax; no tax benefit at contribution |

Life insurance (over $50K) | No | No | Imputed income; taxable to employee |

Wage garnishments | No | No | Court-ordered; post-tax |

Union dues | No | No | Post-tax |

How is net pay calculated?

Net pay is the amount the employee takes home after all deductions are subtracted from gross pay.

The formula is net pay = gross pay – pre-tax deductions – federal income tax – employee FICA – state/local taxes – post-tax deductions.

Here’s how a $75,000 annual salary breaks down for a single filer with no dependents, contributing $300/month to a 401(k) and $200/month to health insurance through a Section 125 plan, paid semi-monthly across 24 pay periods.

Component | Per Pay Period (Semi-Monthly) |

Gross pay | $3,125.00 |

Pre-tax health insurance (Section 125) | -$100.00 |

Pre-tax 401(k) contribution | -$150.00 |

FICA wages (gross minus Section 125 only) | $3,025.00 |

Social Security (6.2% of $3,025) | -$187.55 |

Medicare (1.45% of $3,025) | -$43.86 |

Federal income tax withholding (est.) | -$320.00 |

State income tax (approximation at ~3.3% effective rate) | -$100.00 (example; varies by state) |

Net pay (take-home) | ~$2,223.59 |

Notice that Social Security and Medicare are calculated on $3,025 (gross minus the Section 125 health insurance deduction), not on the full $3,125. The 401(k) contribution reduces federal income tax withholding but doesn’t reduce FICA. This distinction is why the table shows the FICA wages line separately.

In this example, approximately 21% of gross pay goes to federal, state, and FICA taxes, with an additional 8% going to the employee’s own retirement savings and health insurance. The actual percentage varies depending on the employee’s state, filing status, benefit elections, and retirement contribution level. An employee in Texas (no state income tax) would take home roughly $100 more per pay period than this example shows. Cloud-based payroll software automates these gross-to-net calculations and applies the correct FICA treatment for each deduction type automatically.

What are payroll liabilities?

Payroll liabilities are the payroll expenses a company owes but has not yet paid, including employee wages, the employer’s share of FICA taxes, unemployment insurance, withheld income taxes, benefit contributions, and accrued PTO. Withholdings and payroll deductions are considered liabilities from the moment they are withheld from an employee’s paycheck until the money is transferred to the agencies and providers to which they are due.

Tracking payroll liabilities accurately is critical for cash flow management and compliance. Employers must ensure that business income and cash flow can accommodate payroll obligations on their scheduled dates. Failing to remit withheld taxes on time triggers IRS deposit penalties (2% to 15%, depending on how late) and can create personal liability under the Trust Fund Recovery Penalty for responsible persons who willfully fail to remit.

What tax forms are required for payroll?

Employers must collect specific forms from employees before placing them on payroll, file periodic reports with federal and state agencies, and distribute year-end tax documents.

Employee onboarding forms: Form W-4 (Employee’s Withholding Certificate) determines federal income tax withholding. Form I-9 (Employment Eligibility Verification) verifies that each new hire is authorized to work in the United States. Form W-9 (Request for Taxpayer Identification Number) should be collected from every independent contractor at onboarding, regardless of expected payment amount, to support potential 1099 filing and protect against backup withholding obligations. Without a W-9 on file, the payer must initiate 24% backup withholding once a 1099 filing obligation is triggered.

Quarterly and annual employer filings: Form 941 (Employer’s Quarterly Federal Tax Return) reports and remits the employer and employee shares of FICA plus withheld federal income taxes. Form 940 (Employer’s Annual Federal Unemployment Tax Return) reports FUTA liability. Form 944 is an annual alternative to quarterly 941 filings for employers with $1,000 or less in annual employment tax liability (only if the IRS has notified you to use it).

Year-end employee documents: Form W-2 (Wage and Tax Statement) reports each employee’s annual wages and taxes withheld. Form W-3 transmits W-2 data to the Social Security Administration. Form 1099-NEC reports payments of $2,000 or more to independent contractors for tax year 2026 (raised from $600 under Section 70433 of the One Big Beautiful Bill Act, signed July 4, 2025). This threshold will be inflation-adjusted starting in 2027. For Applicable Large Employers (50+ full-time employees), Form 1095-C reports health coverage offers, and Form 1094-C transmits the 1095-C data to the IRS.

State filings: State equivalents to Form 941 (typically combined unemployment and withholding quarterly returns, such as NY Form NYS-45, CA DE-9/DE-9C, or IL UI-3/40) must also be filed in each state where the employer has employees. Each state sets its own filing deadlines and formats.

When must employers deposit payroll taxes?

The federal government has two regular deposit schedules for income and FICA tax deposits, plus a next-day acceleration rule that overrides either schedule in certain situations.

Monthly depositors: Must deposit employment taxes on payments made during a month by the 15th day of the following month. This schedule applies to employers with $50,000 or less in total tax liability during the lookback period.

Semi-weekly depositors: Must deposit employment taxes for pay dates on Wednesday, Thursday, or Friday by the following Wednesday. For pay dates on Saturday, Sunday, Monday, or Tuesday, the deposit is due by the following Friday. This schedule applies to employers with more than $50,000 in total tax liability during the lookback period.

$100,000 next-day rule: If an employer accumulates $100,000 or more in taxes on any day during a deposit period, the tax must be deposited by the next business day, regardless of the employer’s regular deposit schedule.

FUTA deposits follow a separate schedule. If FUTA liability exceeds $500 in a quarter, the employer must deposit by the last day of the first month following the quarter's end. If $500 or less, the liability carries forward to the next quarter.

How often must employers pay employees?

Pay frequency is driven by state law and employer preference. Common schedules include weekly, biweekly (every other week), semi-monthly (twice per month on set dates, such as the 1st and 15th), and monthly. Some states mandate minimum pay frequencies. California, for example, requires semi-monthly pay for most employees. New York requires weekly pay for manual workers. Employers must check their state’s requirements when setting up payroll schedules, especially if they have remote employees in multiple states.

How does benefits administration connect to payroll?

Benefits administration is a payroll component that involves managing enrollment, calculating deductions, and ensuring that employer and employee contributions are remitted to the correct providers on schedule.

During open enrollment periods, employees review and select their benefit plans (health insurance, dental, vision, FSA, HSA, life insurance, disability, retirement). The payroll system must then apply the correct deduction amounts, categorize each deduction as pre-tax or post-tax, calculate the employer’s matching contribution where applicable, and remit both portions to the benefits providers. Changes during the year (qualifying life events like marriage, birth, or loss of other coverage) trigger mid-year updates that must flow through payroll accurately.

Common benefits processed through payroll include health insurance premiums, retirement plan contributions (401(k), 403(b), SIMPLE IRA), FSA and HSA contributions, life and disability insurance, and commuter benefits. Each has specific tax treatment rules that the payroll system must apply correctly.

How do payroll components differ for international employers?

Payroll components for international employers differ primarily in statutory contribution rates, mandatory benefits, and the types of deductions required by local law. The gross-to-net framework stays the same (earnings minus deductions equals net pay), but the specific components within each category change by country.

In France, employer social security contributions add 40% to 45% of gross salary, covering health insurance, pension, unemployment, and family benefits. In Germany, the employer’s share is approximately 21% to 23% (including insolvency contribution and statutory accident insurance), split across pension (9.3%), health insurance (7.3% + variable supplementary rate), unemployment (1.3%), and long-term care (1.8%). In the UK, employer National Insurance is a flat 15% on earnings above the secondary threshold (from April 2025). In India, the employer’s provident fund contribution is 12% of basic salary, plus ESI (Employees’ State Insurance) for eligible workers.

International payroll also introduces components that don’t exist in US payroll. Many countries require employers to distinguish between overtime on normal workdays during daytime, overtime during nighttime, and overtime on weekends and holidays, each at different premium rates. Accruals for severance pay, holiday pay, and 13th/14th-month salary must be tracked as employer liabilities throughout the year. Skills development levies, insolvency fund payments, and sector-specific payroll taxes exist in several countries and must be included in the employer’s cost calculations.

For companies hiring across multiple countries, each country’s payroll components must be calculated according to local law. An employer of record (EOR) or global payroll provider typically handles these country-specific calculations to avoid compliance errors. Data security in payroll becomes especially important when employee compensation data crosses international borders and falls under different privacy regulations like GDPR.

What payroll records must employers maintain?

Employers must maintain payroll records for at least 4 years per IRS regulations (Reg. § 31.6001-1) and at least 3 years under the FLSA, making the effective standard 4 years. Some HR experts recommend retaining records for 7 years to cover all federal and state requirements.

Under the FLSA, the basic records an employer must maintain include employee’s full name and Social Security number, address, birth date (if under 19), gender and occupation, day and time when the workweek begins, hours worked each day and total hours each workweek, basis on which wages are paid (hourly rate, weekly salary, piecework), regular hourly pay rate, total straight-time earnings, total overtime earnings, all additions to or deductions from wages, total wages paid each pay period, and date of payment and pay period covered. Electronic payroll data storage solutions make maintaining these records and retrieving them during audits significantly easier than paper-based systems.

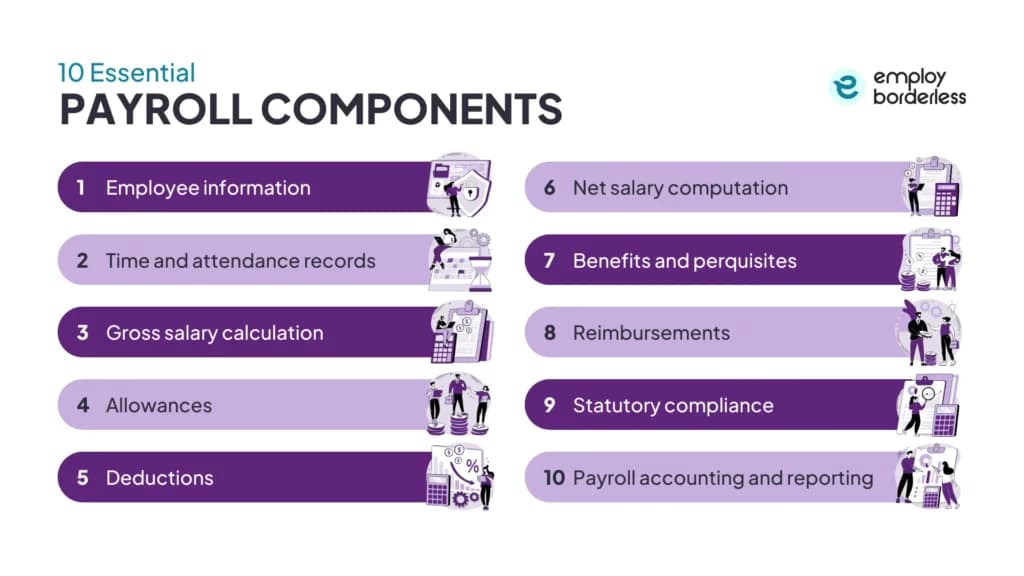

What are the main components of a payroll system?

The main components of a payroll system are employee data management, time and attendance tracking, gross pay calculation, tax computation, deductions processing, benefits administration, net pay calculation, payment distribution, and reporting and compliance. These components work together to transform raw employee data (hours worked, salary, tax status) into accurate paychecks and correct tax filings.

What is the difference between gross pay and net pay?

Gross pay is the total amount an employee earns before any deductions, while net pay is the amount they take home after all taxes and deductions are subtracted. For a typical US employee, net pay is roughly 65% to 80% of gross pay, depending on their tax bracket, benefit elections, and state of residence.

What payroll taxes do US employers pay?

US employers pay 6.2% Social Security tax (on wages up to $184,500 in 2026), 1.45% Medicare tax (no wage cap), FUTA at an effective rate of 0.6% (on the first $7,000 per employee), and state unemployment insurance at rates that vary by state and employer experience rating. Workers’ compensation insurance is also an employer cost in most states. Combined, employer-side payroll taxes and mandatory insurance typically add 10% to 15% on top of each employee’s gross salary before factoring in voluntary benefits like health insurance and retirement plan matching, which can bring the fully loaded cost to 25% to 40% above base salary.

What is the difference between pre-tax and post-tax deductions?

Pre-tax deductions are subtracted from gross pay before taxes are calculated, which lowers the employee’s taxable income and reduces their tax bill. Post-tax deductions are subtracted after taxes, so they don’t reduce taxable income. Common pre-tax deductions include traditional 401(k) contributions and health insurance premiums through a Section 125 plan, though their tax treatment differs. Section 125 deductions reduce both income tax and FICA, while 401(k) contributions reduce only income tax and remain subject to Social Security and Medicare. Common post-tax deductions include Roth 401(k) contributions and wage garnishments. The critical distinction is that Section 125 deductions reduce both income tax and FICA, while 401(k) contributions reduce only income tax.

How many payroll components are there?

There’s no fixed number of payroll components because the specific elements depend on the country, the employer’s benefit offerings, and the employee’s elections. A basic US payroll has at a minimum seven components, including base pay, federal income tax withholding, Social Security tax (employee and employer), Medicare tax (employee and employer), FUTA, and state taxes. Most employers also handle health insurance, retirement contributions, and various voluntary deductions, bringing the total to 10 to 15 distinct line items on a typical payroll run.

What are payroll liabilities, and why do they matter?

Payroll liabilities are amounts a company owes but hasn’t yet paid, including accrued wages, withheld taxes awaiting remittance, employer FICA due, unemployment taxes, and accrued PTO or benefits. They matter because these amounts must be tracked as current liabilities on the balance sheet and remitted on schedule. Late remittance of withheld taxes triggers IRS penalties and can create personal liability for business owners under the Trust Fund Recovery Penalty.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Ready to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations