Cost of a PEO: pricing models, services, and factors that influence pricing (hidden costs)

Robbin Schuchmann

Co-founder, Employ Borderless

A professional employer organization typically costs $100 to $250 per employee per month for small and mid-sized businesses (10-100 employees) on a flat-fee PEPM model, or 3% to 12% of gross payroll on a percentage model. Larger companies (100+) can negotiate PEPM rates as low as $40 to $120. The total cost of working with a PEO goes beyond the administrative fee and includes benefits premiums, workers’ compensation insurance, and payroll taxes, all of which are pass-through costs billed separately from the PEO’s service fee.

A 2019 NAPEO-commissioned study (McBassi & Company, using 2018 cost data) estimated the average annual PEO administrative cost at approximately $1,395 per employee, with average annual savings of approximately $1,775 per employee and a cost savings ROI of roughly 27%. Separate NAPEO research (2024 white paper) found that PEO clients experience 12% lower employee turnover, are roughly 50% less likely to go out of business, and have growth rates more than twice as high as comparable non-PEO businesses.

These figures provide directional guidance, but the cost data is seven years old and was produced by a study sponsored by the PEO industry’s trade association. Current PEO pricing, particularly for healthcare pass-through costs, has risen meaningfully since 2018. Use these benchmarks as a starting point, not as current market rates.

What are the PEO pricing models?

PEOs use three primary pricing models. Flat fee per employee per month (PEPM), percentage of gross payroll, and hybrid structures that combine elements of both. The right model depends on your headcount, average salary levels, and how predictable you need your costs to be.

Model | Typical Range | Best For | Watch Out For |

Flat fee (PEPM) | $40–$250/mo ($40–$75 basic; $75–$150 mid-range; $125–$250 premium) | Mid-to-senior salary roles; predictable budgeting; companies that want cost certainty | Overpaying for low-salary or part-time roles; doesn’t scale down if headcount drops |

Percentage of payroll | 2%–12% of gross payroll | Businesses with variable pay, seasonal staff, or lower salaries | Costs escalate with raises, bonuses, and overtime; high-salary companies overpay |

Hybrid | Base fee + smaller percentage, or tiered PEPM | Companies with mixed workforce (salaried + hourly) | Less price transparency; harder to compare across providers |

Flat fee per employee per month (PEPM)

The PEPM model charges a fixed monthly amount per employee regardless of their salary. If you have 20 employees and the PEPM fee is $150, your monthly PEO administrative cost is $3,000. This model offers predictable budgeting and doesn’t penalize you for giving raises or paying bonuses. The trade-off is that you pay the same fee for a $30,000/year entry-level employee as for a $150,000/year director. For businesses with predominantly higher-salary employees, PEPM is almost always cheaper than percentage-based pricing.

PEPM rates vary significantly by provider tier. Basic PEOs (primarily payroll and compliance) typically charge $40 to $75 per employee. Mid-range providers (adding benefits administration, risk management, and HR support) charge $75 to $150. Premium PEOs (full-service HR including talent acquisition, training, and specialized consulting) charge $125 to $250. Smaller companies under 10 employees often face proportionally higher per-employee rates because the PEO’s fixed costs are spread across fewer workers.

Percentage of payroll

The percentage model charges 2% to 12% of total gross payroll each pay period, with rates varying by headcount, industry, and scope of services. For a company with $200,000 in monthly gross payroll at a 5% rate, the PEO fee would be $10,000/month. This model scales automatically with your workforce size. The risk is cost escalation. If you hire a senior executive at $180,000/year and your PEO charges 8%, the PEO fee on that single employee is $14,400/year, roughly triple what a $150/month PEPM rate would cost. Always run the math on both models using your actual payroll data before committing.

Alternative pricing models

Beyond the standard PEPM and percentage models, some PEOs offer tiered pricing (different service packages at varying price points, with higher tiers offering more services), value-based pricing (fees based on the perceived value and complexity of services rather than headcount or payroll alone), and usage-based pricing (charges based on actual service usage, such as number of HR inquiries handled or payroll transactions processed). Pricing strategy research suggests that PEO administrative fees tend to be under-scrutinized by clients because they’re small relative to insurance costs, which creates pricing power that many PEOs underutilize, and that clients should be more aware of when negotiating.

What does the PEO fee actually cover?

The PEO administrative fee covers payroll processing, HR support, compliance management, tax filing, HRIS technology access, and workers’ compensation administration. Benefits premiums, payroll taxes, and workers’ compensation insurance premiums are separate pass-through costs that the PEO collects and remits to carriers and tax authorities.

This distinction matters because a PEO quoting "$150 PEPM" is quoting the administrative fee only. Your actual monthly cost per employee also includes gross salary, employer FICA (6.2% Social Security on wages up to $184,500 in 2026, plus 1.45% Medicare), FUTA and state unemployment taxes, health insurance premiums (employer share), workers’ compensation premiums, and retirement plan contributions. Some PEOs bundle the administrative fee with certain pass-through costs into a single invoice. Others itemize everything separately. Ask your provider for a sample invoice showing exactly how costs are broken down before signing.

When comparing providers, request the "unbundled rate" rather than just the "bundled rate" that presents everything as a single per-employee figure. The unbundled rate shows state and federal unemployment insurance costs, current tax liabilities, workers’ compensation premiums, administrative fees, and benefits costs as separate line items. This transparency lets you compare each component against standalone alternatives and identify where the PEO adds value versus where you’re overpaying.

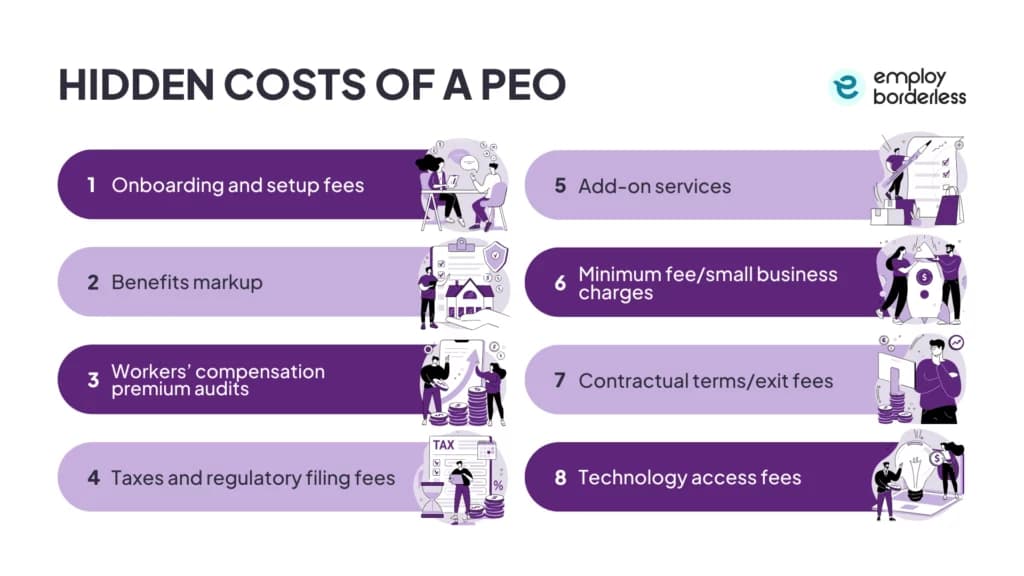

Set up and onboarding fees

Setup and onboarding fees typically range from $500 to $2,500. Some PEOs waive these for multi-year contracts or higher headcounts. The actual onboarding cost includes system integration and data migration, configuring the PEO’s software to align with your existing HR tech stack, employee enrollment processing, policy development and customization, and initial compliance audits. Small businesses with fewer than 10 employees often face monthly minimums of $1,000 to $3,000, making the effective per-employee cost disproportionately high. Many PEOs decline to onboard clients below 5 to 10 employees regardless of the fee.

Health insurance

Health insurance through a PEO is the largest cost variable, and it doesn’t always save money. Many PEOs operate self-insured ERISA master medical plans, not traditional small-group carrier plans. Under these arrangements, clients are pooled together and charged composite rates that blend the risk profiles of all employers in the pool. If your workforce is young and healthy, you may pay more through the PEO’s master plan than you would on a standalone small-group or level-funded plan. If your workforce is older or has higher utilization, the PEO’s pool likely saves you money. Among businesses with 10 to 49 employees, 52% of PEO users offer a retirement plan compared to just 23% of non-PEO businesses (NAPEO), which illustrates how PEO benefits extend beyond health insurance into retirement plans and other offerings that smaller companies typically can’t access independently.

Year-end and miscellaneous fees

Some PEOs charge additional fees for year-end tax documentation (W-2 preparation, ACA reporting), custom policy development, HR training sessions, and employee termination processing. These charges may not appear in the initial quote but show up on invoices throughout the year. Ask for a complete schedule of all possible charges, including those billed on an ad hoc basis, before signing.

Losing access to the PEO’s master medical plan

The most significant exit cost is often losing access to the PEO’s master medical plan. When you leave a PEO, employees lose their group health coverage, and you must set up a new plan at small-group market rates with no underwriting history. For companies with older or higher-utilization employees, this can increase health insurance costs by 20% to 40% on exit. This risk is larger than any early termination fee and should be factored into the total cost of the PEO relationship from the start.

How does PEO cost compare to other HR options?

The three main options for managing HR are a PEO, a payroll software stack with a benefits broker, and a full in-house HR team. Each has a different cost profile, and the right choice depends on your headcount, complexity, and how much HR control you need. For a detailed breakdown of how these models differ beyond cost, see our comparison of PEO and traditional HR.

Expense | In-House HR | PEO (20 employees) | Payroll Software + Broker |

HR manager salary | $55,000–$75,000 | Reduced (PEO covers admin; internal HR coordinator still needed at 15+ employees, $0–$30,000) | None or fractional ($10K–$20K) |

Benefits and taxes on HR salary | $14,000–$26,000 (25–35%) | None | None or minimal |

Payroll software | $2,000–$5,000/year | Included | $2,000–$5,000/year |

HRIS software | $5,000–$15,000/year | Included | $0–$5,000/year |

Compliance/legal services | $5,000–$15,000/year | Included | $3,000–$8,000/year |

Benefits broker | $3,000–$8,000/year | Included | $3,000–$8,000/year |

Workers’ comp admin | $1,000–$3,000/year | Included | $1,000–$3,000/year |

Estimated annual total | $80,000–$147,000 | $36,000–$90,000 (at $150–$250 PEPM + internal HR coordinator) | $20,000–$49,000 |

The payroll-software-plus-broker option is the most common choice for businesses with 10 to 30 employees that have straightforward HR needs. A PEO becomes more cost-effective when you need group benefits, purchasing power, workers’ comp management, or multi-state compliance support. NAPEO’s 2019 study found that PEO clients use approximately 40% fewer HR employees on average. The crossover point where in-house HR becomes cheaper than a PEO typically falls between 50 and 100 employees.

At 50 full-time employees, companies also trigger Applicable Large Employer (ALE) status under the ACA, which adds Form 1095-C reporting and Section 4980H penalty exposure. These requirements are complex enough that some companies stay with a PEO specifically for ACA compliance, even past the cost crossover point.

When is a PEO worth the investment?

A PEO is typically worth the investment for businesses with 10 to 75 employees that lack dedicated HR expertise, need access to group benefits, or operate in high-risk or multi-state environments. For larger organizations with established HR departments, the cost-benefit calculation shifts.

PEO Investment May Be Justified When | Alternatives May Be Better When |

Small businesses lacking dedicated HR expertise | Large organizations with well-established HR departments |

Companies experiencing rapid growth requiring scalability | Organizations with existing cost-effective HR solutions |

High-risk industries needing workers’ comp management and compliance support | Companies with complex, non-standard operational requirements |

Organizations seeking group-rate benefits packages (health, dental, 401(k)) | Highly specialized industries requiring niche HR expertise |

Current HR costs exceeding industry benchmarks | Businesses requiring maximum direct control over HR decisions |

Companies facing recruitment and retention challenges | Companies that already have low turnover and strong benefits programs |

What is the difference between CPEO and non-CPEO pricing?

A Certified Professional Employer Organization (CPEO) is IRS-certified under IRC Section 3511, which means the CPEO assumes federal employment tax liability on wages it pays to worksite employees and eliminates the wage-base restart problem when clients switch PEOs mid-year.

The wage-based restart is a high hidden cost of switching non-CPEO PEOs. Social Security tax (6.2%) applies to wages up to $184,500 per employee in 2026. If you switch from a non-CPEO PEO to a new provider mid-year, the new provider restarts the Social Security wage base from zero for the employer’s share, meaning the employer pays 6.2% again on wages already taxed under the old PEO. (Employees generally recover any excess withholding as a credit on their personal 1040.) FUTA ($7,000 wage base) and state unemployment wage bases also reset, which often creates additional duplicate tax exposure beyond Social Security.

For a 20-employee company with an average salary of $80,000 switching in July, the new PEO restarts the Social Security wage base from zero and pays 6.2% on wages that the old PEO already taxed. The employer-side duplicate Social Security cost is approximately 20 × $40,000 (wages already taxed Jan-June) × 6.2% = $49,600 in employer SS tax paid twice on the same wages, plus FUTA and SUTA restarts.

The employer doesn’t easily recover this duplicate because the wage-base restart creates a new employer obligation under the new PEO’s EIN. Employees generally recover any excess employee-side withholding as a credit on their personal 1040. With a CPEO, no wage-base restart occurs, and certain federal tax credits (R&D credit, Work Opportunity Tax Credit) flow through to the client, which may not be the case with non-CPEO arrangements.

CPEO and non-CPEO administrative fees are roughly comparable in current markets. The CPEO advantage is primarily the wage-base restart protection and federal employment tax liability assumption, not a pricing premium. Some industry commentators argue that CPEO tax-protection benefits have become less relevant for companies that don’t plan to switch PEOs mid-year. Evaluate CPEO value based on your likelihood of switching providers, your mid-year hiring volume, and whether you claim federal tax credits that require employer-of-record alignment.

What factors affect PEO pricing?

The main factors that affect PEO pricing are company size (headcount), employee employment status (full-time vs part-time mix), industry risk classification, geographic location, scope of services, existing benefit offerings, and employee salary levels.

Headcount

Headcount is the primary driver. PEOs offer volume discounts starting at 10 to 20 employees, with deeper discounts at 50+ and 100+. Very small companies (under 10 employees) often face higher per-head rates because the PEO’s fixed costs are spread across fewer workers.

Employee status (full-time vs part-time)

The ratio of full-time to part-time employees affects pricing because management and benefits costs differ between these classifications. PEO pricing is typically based on full-time equivalent (FTE) employees, meaning the cost decreases in proportion to the percentage of your workforce that is part-time. If a significant portion of your staff works part-time, your effective per-employee cost may be lower than the headline PEPM rate suggests.

Industry risk

Industry risk directly affects workers’ compensation rates, which are priced per $100 of payroll. Office-based businesses typically pay under $1 per $100. Light manufacturing and healthcare roles like nursing average $3 to $8 per $100. High-risk construction trades (roofing, structural steel, tree trimming) can exceed $20 per $100 in many states and reach $40 to $80 per $100 in high-rate states like California and New York. Rates also vary by state, as California uses its own rating bureau (WCIRB) rather than the NCCI system used by most other states.

Geographic location

Geographic location matters because state-specific compliance requirements add to PEO costs. Multi-state companies face higher fees than single-state operations. States and territories with mandatory paid family leave or disability programs (California, Colorado, Connecticut, Delaware, DC, Maine, Massachusetts, Minnesota, New Jersey, New York, Oregon, Rhode Island, and Washington; Maryland’s premium contributions begin in 2027 with benefits starting 2028) add pass-through costs and administrative complexity. Payroll taxes and withholding rules also vary among states, with nine states having no state income tax on wages (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming) and locations like New York City and Chicago having notably higher tax rates and workers’ compensation fees.

Existing benefit offerings

What you currently offer and budget for affects how PEO pricing compares to your existing costs. If you’re not already budgeting for 401(k) retirement plans or healthcare benefits, the PEO price tag may seem higher than expected because you’re adding benefits you didn’t previously offer. If you’re already providing these benefits independently, you’ll likely find cost savings by partnering with a PEO because their pooled purchasing power negotiates better rates than most small businesses can access alone.

How does co-employment affect PEO pricing?

Co-employment means the PEO shares certain employer responsibilities for HR functions like payroll tax, benefits administration, and compliance, and the pricing reflects that expanded scope of responsibility. Under a co-employment arrangement, the PEO becomes the employer of record for tax purposes while you remain the worksite employer who manages day-to-day operations. This shared responsibility model is fundamentally different from simply outsourcing payroll or hiring an HR consultant because the PEO takes on legal liability for employment tax compliance.

The co-employment structure is what enables PEOs to offer group-rate benefits in the first place. By aggregating employees across multiple client companies into a single pool, the PEO can negotiate insurance rates and retirement plans that individual small businesses can’t access. It’s also what creates the risk management value. PEOs assume shared responsibility for compliance with labor laws, workers’ compensation administration, and employment practices. PEO workplace safety programs can reduce claims frequency, which in turn lowers workers’ compensation premiums for client companies over time.

How do you choose the right PEO for your business?

Choosing the right PEO requires matching the provider’s strengths to your specific needs across four dimensions. Cost structure, benefits, quality, compliance capability, and technology.

Request a total cost of employment breakdown: Request a total cost of employment breakdown from at least three providers using the same employee census data. Compare the administrative fee, health insurance rates (and whether the plan is self-insured or fully insured), workers’ comp rates by classification code (including loss fund and assessment charges), and all one-time fees. Also consider whether a PEO is the right model at all. For companies with basic payroll and benefits needs, the comparison between a PEO and traditional HR setup (payroll software plus benefits broker) may favor the lower-cost option.

Evaluate PEO benefits carefully: The PEO’s group health plan isn’t automatically cheaper than what you can get on your own. Request plan details, network coverage, and premium comparisons against standalone quotes. If the PEO operates a self-insured master plan, ask about claim-to-premium ratios and whether you can bring your own broker’s plan instead.

Check if the provider is IRS-certified: Ask each provider whether they’re IRS-certified as a CPEO, what happens to your workers’ comp mod rate if you leave, what the minimum contract length and early termination penalties are, and what the transition process looks like for your health plan on exit. For a curated comparison of providers, see our guide to the best PEO for small businesses.

Assess technology and service level: Evaluate the PEO’s HRIS platform, self-service portal, reporting capabilities, and integration with your existing tools. Consider whether you need a basic self-serve model or premium white-glove support with dedicated HR professionals. The level of service directly affects pricing, so make sure you’re paying for the tier of support you actually need.

What is the average PEO cost per employee?

Current market PEPM rates for small and mid-sized businesses (10-100 employees) typically run $40 to $250 per employee per month for administrative fees, depending on the provider tier and scope of services. A 2019 NAPEO study (based on 2018 data) estimated the average at approximately $1,395/year ($116/month), but PEO pricing has risen since then, particularly for healthcare-related pass-through costs. Benefits, premiums, payroll taxes, and workers’ comp are additional.

Is a PEO worth the cost?

For most businesses with 10 to 75 employees, a PEO is worth the cost when the savings on group benefits purchasing, workers’ comp premiums, and HR administrative overhead exceed the PEO’s administrative fees. NAPEO’s 2019 study estimated roughly 27% ROI on cost savings alone. Separate NAPEO research (2024) found that PEO clients experience 12% lower turnover, are 50% less likely to go out of business, and have growth rates more than twice as high as non-PEO businesses. However, these results vary significantly by employer size, industry, and health plan demographics. Companies with young, healthy workforces may not see benefits savings through a PEO’s pooled master plan.

Do PEOs charge for terminations?

Most PEOs don’t charge per-employee termination fees, but many charge for exiting the PEO relationship entirely, including 30 to 90-day notice periods and penalties of one to three months’ administrative fees. The larger exit cost is usually losing access to the PEO’s master medical plan. You’ll need to re-establish health coverage at small-group market rates with no underwriting history, which can increase premiums 20% to 40% for higher-utilization workforces.

Can you negotiate PEO pricing?

Yes, PEO pricing is negotiable, especially for companies with 20 or more employees and clean claims histories. Volume discounts of 10% to 25% are common. Setup fees can often be waived for multi-year commitments. Workers’ comp rates may be adjustable based on your individual mod rate rather than the PEO’s pooled rate (depending on the state and PEO). The stronger your negotiating position (larger headcount, low-risk industry, good claims history), the more pricing flexibility you’ll find.

How does co-employment affect PEO pricing?

Co-employment means the PEO shares certain employer responsibilities, and the pricing reflects the expanded scope of legal liability the PEO assumes. Packages typically bundle ongoing administration and support tied to those shared duties. The co-employment structure is what enables group-rate benefits and workers’ comp pooling, which are the primary cost advantages of working with a PEO. Expect the pricing structure (PEPM or percentage of payroll) to map directly to the level of service and risk the PEO takes on.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Ready to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations