11 reasons your small business should consider using a PEO

Robbin Schuchmann

Co-founder, Employ Borderless

A PEO (Professional Employer Organization), also known as an HR outsourcing service, is a third-party company that provides HR services to businesses under a co-employment arrangement. These HR services include payroll processing, employee benefits administration, compliance, and risk management.

A PEO works by entering into a co-employment model, where it handles administrative employer tasks, such as filing and remitting taxes under its own tax ID and administering benefits, while the business maintains control of daily operations, like hiring, firing, and managing staff.

The main reasons your small business should consider using a PEO include access to competitive employee benefits, employee recruitment and onboarding, and improving employee retention and company growth.

The 11 reasons your small business should consider using a PEO are listed below.

- Access to competitive employee benefits: PEOs pool employees from small businesses to access competitive employee benefits, simplify enrollment, carrier management, and compliance.

- Save time and cost: Outsourcing administrative tasks to a PEO saves time and reduces HR overhead costs for small businesses, which also allows them to focus on strategic growth and core business activities like marketing and product development.

- Compliance and risk mitigation: A PEO makes sure small businesses comply with federal, state, and local employment laws to reduce the risk of non-compliance, legal disputes, fines, and reputational damage.

- Automate payroll process: The PEO automates payroll processes using advanced technology and software tools to simplify complex tasks and reduce administrative burden.

- Manage workers' compensation: This HR outsourcing model manages workers' compensation, insurance, and benefits for small businesses, to secure affordable insurance, handle claims accurately, and reduce downtime.

- Employee recruitment and onboarding: This third-party service provider helps small businesses in recruitment and onboarding by offering digital platforms, like ATS (Applicant Tracking System), to simplify the hiring and onboarding process.

- Improve employee retention and company growth: PEOs help small firms reduce employee turnover by offering competitive benefits and wellness programs for long-term growth and employee retention.

- Access to HR expertise and technology: A PEO provides HR expertise and technology to small businesses, which simplifies HR processes and provides guidance on recruitment, onboarding, and compliance. They also set up integrated HR technology platforms for employee management.

- Attract investors and raise capital: This HR outsourcing model helps small companies attract investors and raise capital by offering structured HR systems and increasing financial transparency for growth and securing external resources.

- Reduce employer liability: The PEO reduces employer liability as it shares employment responsibilities, puts risk management practices in place, and offers compliance support.

- Access to insurance options: PEOs offer small businesses a wide range of insurance coverage, such as health, retirement, and disability insurance.

1. Access to competitive employee benefits

Access to competitive employee benefits means PEOs pool employees from multiple small businesses to increase their collective purchasing power, negotiate better rates, and access a wide range of benefits. These benefits include health insurance, retirement plans like 401(k), life and disability insurance, and voluntary benefits.

Small businesses face challenges in providing attractive employee benefits due to their limited resources and bargaining power, so it is difficult for them to compete for top talent and retain existing employees. The PEO helps small businesses with benefits administration by simplifying enrollment, carrier management, and compliance.

PEOs offer Fortune 500-level benefits, such as health, dental, and vision insurance, EAPs (Employee Assistance Programs), and paid parental leave, that are usually too expensive for small businesses. These benefits become affordable through a PEO, which also improves employee satisfaction and retention without straining the company's budget.

2. Save time and cost

Saving time and cost means outsourcing complex administrative tasks, such as payroll processing and employee time tracking, to a PEO helps small businesses save time and reduce HR overhead costs.

Partnering with a PEO allows small businesses to delegate complex HR tasks, such as payroll processing, compliance management, and employee paperwork. This delegation of human resources functions reduces the time internal teams spend on administrative work, lowers the risk of penalties and legal costs, and results in overall cost savings. Outsourcing these responsibilities also frees up company resources to focus on strategic growth and core business activities, like marketing, sales, and product development, for operational accuracy and productivity.

3. Compliance and risk mitigation

Maintaining compliance and managing risk means PEOs make sure small businesses follow all relevant federal, state, and local employment laws to reduce the risk of non-compliance, legal disputes, fines, and reputational damage.

Small businesses lack the resources or specialized HR support to comply with changes in federal, state, and local employment laws, from wage requirements and paid leave to contractor classification and anti-discrimination mandates. This limitation increases the risk of non-compliance, fines, lawsuits, or reputational harm. PEOs protect small businesses by conducting regular compliance audits and risk assessments to identify classification errors, outdated policies, or compliance gaps before they lead to penalties.

The PEO helps create and maintain employment handbooks and HR policies, such as anti-harassment guidelines and leave protocols, according to the current laws. It also manages important regulatory areas, such as OSHA (Occupational Safety and Health Act) workplace safety standards, healthcare reform requirements, wage and hour laws, and anti-discrimination policies. PEOs help small businesses mitigate legal risks and maintain a compliant and safe work environment by expertly handling these complex regulations.

4. Automate payroll process

Automating the payroll process means PEOs use advanced technology or software tools to manage and process workers' payments automatically.

Small companies face an administrative burden when they handle complex payroll responsibilities in-house, like calculating wages, overtime, deductions, and following multi-state tax filings. PEOs simplify payroll by using cloud-based platforms to automate wage and overtime calculation, manage benefits and deductions, process direct deposit payments, file taxes on time, and create reliable reporting and payslips. This automation reduces manual errors, provides timely and compliant payments, and lowers the administrative burden on internal staff.

PEOs integrate advanced payroll systems with time-tracking tools to directly transfer employees' hours worked into payroll and reduce duplicate data entry. They also provide detailed reporting and self-service portals for employees to access pay stubs, tax forms, and earnings history. This integration increases transparency, improves workplace productivity, and allows HR to shift its focus from manual calculations to strategic initiatives.

5. Manage workers' compensation

Managing workers' compensation means the PEO handles insurance, wage replacement, and benefits when workers suffer from an injury or a disease at their worksite.

Small businesses face rising insurance premiums, complex claims processes, and unexpected year-end payments due to limited resources and expertise, which affect their financial budgets and also shift their focus away from core operations. PEOs help small businesses secure affordable insurance by pooling multiple employers under a single policy to lower workers' compensation rates through group buying power.

PEOs fully handle the claims process, which includes accident reports, medical documentation, coordination with medical providers and insurers, and providing timely resolution. PEOs create and manage return-to-work programs to help injured employees continue work quickly, reduce downtime, and claim expenses. They also support small businesses with safety audits, training, loss prevention practices, and fraud prevention to reduce both the frequency and severity of workplace incidents.

6. Employee recruitment and onboarding

Employee recruitment and onboarding mean that PEOs help small businesses with hiring new talent and smoothly integrating them into the workplace.

Small businesses experience challenges in attracting and hiring skilled employees in a competitive job market. PEOs help small firms by providing recruitment support, such as access to ATS (Applicant Tracking System), job posting assistance, screening candidates, and scheduling interviews.

PEOs improve the onboarding process through digital platforms that help with manual paperwork, support policy compliance, and create positive first impressions for new employees.

This third-party service provider supports employee growth through training programs, professional development initiatives, and performance management systems. These services help employees improve their skills, understand clear performance expectations, receive regular feedback, and achieve long-term business objectives.

7. Improve employee retention and company growth

Improving employee retention and company growth means that PEOs help small businesses reduce employee turnover by providing competitive benefits, wellness programs, and structured HR support. This support helps businesses retain top talent, maintain workforce stability, and promote long-term growth and productivity.

Small firms usually experience higher employee turnover than larger companies, which disrupts operations and increases the workload on remaining staff. This disruption results in lower productivity and raises hiring and training costs, as businesses have to frequently recruit and onboard new employees. PEOs help small firms by providing benefits packages, such as health insurance, retirement plans, dental and vision coverage, and wellness programs, which improve employee retention.

This third-party service provider also puts employee engagement initiatives in place, like recognition programs and career development opportunities. It also administers performance management systems, training programs, and work-life balance initiatives to increase job satisfaction and maintain a healthy work-life balance. This stability supports company growth and improves the organization's competitive position in the market.

8. Access to HR expertise and technology

Access to HR expertise and technology means PEOs offer professional HR support, software, and automation tools to businesses for simplifying the HR processes, such as payroll administration and employee benefits enrollment.

Small companies lack dedicated HR professionals and modern tools to manage complex HR functions accurately. They also struggle with compliance, employee relations, and payroll processing without specialized HR teams. The PEO provides small firms with access to experienced HR professionals who offer guidance on different HR issues, like recruitment, onboarding, performance management, and compliance. This partnership allows small businesses to use expert knowledge and resources usually available only to larger organizations.

PEOs set up integrated HR technology platforms that simplify HR processes, such as payroll, benefits administration, and time tracking. These platforms also include self-service portals for employees to manage their benefits, request time off, and update personal information. PEO integrated systems provide valuable data insights that help small businesses make informed operational decisions and improve workforce management.

9. Attract investors and raise capital

Attracting investors and raising capital means PEOs help small businesses partner with financiers and secure funds from external resources to meet a business's financial needs.

Small businesses struggle to attract investors, who usually favor companies that show operational stability, strong compliance, and financial transparency. These qualities prove that a business is well-organized, follows regulations, and is trusted for a safer and quicker choice for investment. PEOs allow small businesses access to structured HR systems, with accurate payroll, workforce reporting, and clear documentation. This transparent and accurate data reassures investors, builds confidence, and supports capital acquisition.

A partnership with a PEO supports small business growth as it simplifies HR operations and maintains compliance across the board. It also helps small businesses present themselves professionally to investors, which shows they are able to manage growth effectively and increases their investment appeal.

10. Reduce employer liability

Reduced employer liability means the PEO shares employment-related responsibilities with the client company to lower legal risks by putting effective risk management practices in place, such as safety training programs and risk assessment plans.

Small companies face serious financial risks from lawsuits and employee claims related to discrimination, wage disputes, and wrongful termination. These claims carry costly legal fees, settlements, and disrupt operations without proper defenses. PEOs offer expert compliance support for risk assessments, policy development, training, insurance coverage, and workplace safety programs to help businesses comply with employment regulations, like OSHA (Occupational Safety and Health Act). This active guidance helps resolve issues early, prevent disputes that damage the company's legal position, and protect employees.

PEOs provide access to EPLI (Employment Practices Liability Insurance), which covers costs from lawsuits such as discrimination, wrongful termination, and harassment, defense, and settlement expenses. They also manage workplace disputes by coordinating with insurers, maintaining documentation, and guiding resolution through structured processes. PEOs reduce small businesses' exposure to litigation and financial penalties while protecting overall operations and finances.

11. Access to insurance options

Access to insurance options means PEOs provide small businesses with many insurance coverage options, like health insurance, retirement plans, and disability insurance.

Small businesses lack broad insurance coverage for their employees, so partnering with the PEO provides them with different insurance options. These options usually include health Insurance, often ACA-compliant (Affordable Care Act), vision Insurance for eye exams, glasses, and corrective surgeries, and dental Insurance that covers preventive, basic, and major services.

The PEO also offers small businesses life insurance in terms of accidental death or dismemberment, and optional whole-life plans, disability Insurance, which involves short-term and long-term disability coverage. The PEO also provides workers' compensation, EPLI (Employment Practices Liability Insurance), and retirement plans, such as 401(k), through group arrangements.

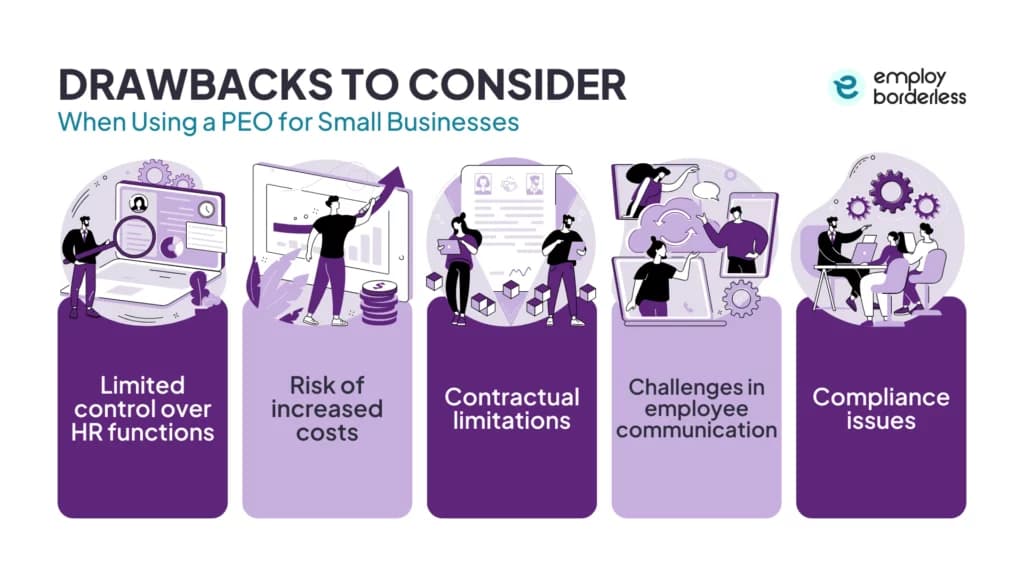

What drawbacks should small businesses consider when using a PEO?

The drawbacks that small businesses should consider when using a PEO include limited control over HR functions, risk of increased costs, contractual limitations, challenges in employee communication, and compliance issues.

The drawbacks that small businesses should consider when using a PEO are listed below.

- Limited control over HR functions: Limited control over HR functions means that when a small business outsources to a PEO, it manages important HR tasks such as payroll, benefits administration, onboarding, and policy setting under a co-employment agreement. This arrangement reduces the employer's control and direct management, since many of the services are standardized and sometimes do not match the company's unique culture or specific needs.

- Risk of increased costs: Risk of increased costs means that small businesses face rising expenses when using a PEO, with fees ranging from 2% to 12% of gross payroll or a flat per-employee rate, which makes it costly as the employee count rises. Extra charges, such as onboarding, benefits markups, premium audits, technological access, and early-termination penalties, also increase the cost. PEOs provide valuable bundled services, but these benefits decrease as the business expands, so a careful cost-benefit analysis is important before committing to a long-term partnership.

- Contractual Limitations: Contractual limitation refers to the long-term commitment of small businesses and restrictive termination terms that are found in PEO contracts. Many PEO agreements include extended contract durations and challenging exit clauses, which make it difficult and costly for small businesses to end the agreement quickly if it becomes unsatisfactory.

- Challenges in employee communication: Challenges in employee communication occur when PEO manages HR functions rather than businesses managing them directly. Employees experience delays or confusion in receiving answers about payroll, benefits, or policies since inquiries have to go through the PEO instead of internal HR, which affects employee satisfaction and trust.

- Compliance issues: Compliance issues occur when small businesses rely on a PEO to manage labor laws, tax filings, and regulatory requirements. For example, if the PEO makes errors or fails to stay updated on changing regulations, the small business is held legally responsible, which creates risks and legal penalties even when outsourcing compliance support to a PEO.

What factors should small businesses consider when choosing a PEO?

The factors that small businesses should consider when choosing a PEO are service offerings, pricing structure and transparency, industry expertise, accreditation and financial stability, and growth capacity.

Small businesses should consider the range and flexibility of services a PEO provides, such as payroll, compliance, benefits, risk management, and HR support. They should also evaluate whether these services match the business's current and future needs.

PEOs usually charge either a percentage of payroll or a flat per-employee fee, so small businesses need to understand the pricing of each service included in the PEO agreement. They also need to carefully review the PEO contract for hidden charges, such as onboarding fees, benefits markups, or technology costs, to assess the true affordability and long-term value of the partnership.

A small company should choose a PEO with experience in its specific industry to confirm the provider understands relevant regulations, compliance requirements, and recommended practices related to the industry.

A small business should also evaluate a PEO's credibility and reliability by checking for accreditations such as ESAC (Employer Services Assurance Corporation) or IRS certification as a CPEO. Strong financial stability of the PEO gives assurance that it is able to accurately handle payroll, benefits, and long-term operations.

The small firm should also assess a PEO's ability to grow with the business by making sure its services can expand as the company hires new employees, moves into new states, or faces more complex HR needs.

How much does a PEO cost for small businesses?

A PEO usually costs 2% to 12% of total payroll or a flat fee of $100 to $200 per employee per month for small businesses. The PEO cost depends on the pricing model, the range of services included, the number of employees, and the complexity of payroll and HR needs.

What does a PEO stand for in HR?

A PEO stands for Professional Employer Organization in HR, which is a third-party organization that partners with businesses through a co-employment arrangement. PEO in HR handles important functions, like payroll processing, benefits administration, compliance, and risk management.

How can PEOs benefit startups?

PEOs can benefit startups as they offer support in attracting and recruiting top talent, provide compliance, handle cost-effective benefit packages, and reduce HR and administrative costs. PEOs for startups also provide health insurance options, retirement plan administration, accurate payroll, tax filing, and deductions, and modern HR technology and tools.

What types of services do PEOs offer to small businesses?

The types of services that PEOs offer to small businesses are access to high-quality and affordable employee benefits, payroll administration, regulatory compliance, and risk management. PEO services to small businesses also include recruitment and talent management, employee training and development, and HR consultancy.

In what ways do PEOs support nonprofits differ from small businesses?

The ways in which PEO support for nonprofits differ from small businesses are in terms of mission objectives, grant compliance, and volunteer management. PEOs for nonprofits provide compliance support related to grants, help manage both staff and volunteers, and reduce administrative tasks so leaders stay focused on serving the people and advancing their mission.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 9 articles

PEO fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations