Payroll vs bookkeeping: definitions, working, differences, similarities, benefits, and drawbacks

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll is the system used by employers to pay a company’s employees. Bookkeeping involves the process of keeping and updating business financial records.

Payroll works by calculating wages, deducting taxes, handling benefits, and making payments. Bookkeeping works by recording and organizing transactions, reconciling accounts, and preparing financial reports.

Payroll focuses on employee compensation and compliance with labor laws, and prepares payslips, tax forms, and employee-benefit records. Bookkeeping follows financial transactions and accounting rules to produce balance sheets, income statements, and cash flow reports. Both procedures share similarities in managing financial data, supporting compliance, keeping records, and using specialized software.

Payroll helps businesses by improving time management, maintaining accurate employee records, securing data handling, and boosting employee satisfaction. Bookkeeping helps by simplifying tax preparation, ensuring audit readiness, monitoring cash flow, increasing financial transparency, and enabling early detection of errors or fraud.

The drawbacks of payroll are that it is time-consuming, complex, costly, and prone to compliance risk. Bookkeeping also has drawbacks, such as being time-consuming, incurring high costs for software or professional services, depending on client’s input, exposing the business to liability, and risking embezzlement.

What is payroll?

Payroll is the system that a business uses to manage and distribute employee salaries and compensation. It includes the calculation of wages or salaries, deductions for taxes, contributions to retirement plans, allocations for benefits such as health insurance, and the distribution of payments. Payroll also represents the set of records that tracks each employee’s earnings, withholdings, and net pay.

Payroll is a financial and legal responsibility of the employer, which connects directly to compliance with labor laws and tax regulations. An accurate payroll process builds trust and financial security between employees and employers, which improves workplace morale and professionalism.

How does payroll work?

Payroll works by a company defining its payroll policy with schedules, overtime rules, benefit eligibility, and deductions. The company then collects employee data, such as personal information, tax forms, bank account details, and attendance or records of working hours, to calculate gross pay. The payroll system deducts taxes and withholdings, such as income tax, social security contributions, and retirement funds. These deductions generate the net pay, which the company transfers to employees through direct deposit, checks, or alternative payment methods.

Payroll also performs reporting and compliance tasks, like submitting payroll tax returns, preparing year-end forms, and storing payroll records for audits and analysis. Some companies, especially those with larger teams, use payroll software or outsource providers to maintain accuracy and efficiency.

What is bookkeeping?

Bookkeeping is the systematic process a business follows to record, organize, and maintain all of its financial transactions. It includes tracking sales, purchases, expenses, and payments, classifying these entries into accounts, and reconciling ledger balances. These accurate and up-to-date financial records support business operations, tax reporting, and decision-making.

A bookkeeper records each transaction using source documents such as invoices, receipts, and bills, and enters the information into a general ledger that tracks assets, liabilities, equity, revenue, and expenses. Bookkeeping also supports basic financial reports like income statements and balance sheets. Bookkeepers use manual records or specialized software to keep track of the company’s financial information.

How does bookkeeping work?

Bookkeeping works by systematically processing and documenting every financial transaction that occurs in a business. A bookkeeper records sales, purchases, expenses, and payments using source documents such as invoices, receipts, bills, and bank statements, and organizes the transactions into accounts in a general ledger.

The bookkeeping process includes managing accounts payable and receivable, reconciling bank statements to verify balances, and maintaining accurate tax records throughout the year. Bookkeepers use these entries to prepare financial reports such as income statements, balance sheets, and cash flow statements that reflect the company’s finances. There are two methods that guide the bookkeeping process, and these are the single-entry system, which tracks transactions like a simple cash register, and the double-entry system, which records equal debits and credits to maintain balance and accuracy.

What are the services of payroll?

The main services of payroll include payroll reporting, workers’ compensation, employment tax forms, tracking employee benefits, time and attendance tracking, compliance expertise, and payment processing.

The services of payroll are listed below.

- Payroll reporting: Payroll reporting is a detailed summary of wages, deductions, and employer liabilities. These reports help HR managers and accounting professionals track labor costs, perform internal audits, and conduct financial planning and compliance checks for better decision-making.

- Workers’ compensation: Workers’ compensation insurance covers employees injured on the job by paying for medical bills, rehabilitation costs, and a portion of lost wages. Payroll service calculates insurance premiums based on employee wages and risk categories. It protects both employers and employees in case of workplace injuries.

- Employment tax forms: Payroll services include year-end reporting and preparing Forms W-2 and 1099-NEC for employees and contractors to report income and tax data to government agencies.

- Tracking employee benefits: This service monitors contributions to health insurance, retirement accounts, and other employee benefit programs. Tracking employee benefits ensures that payroll deductions accurately reflect each employee’s chosen benefits.

- Time and attendance tracking: Payroll systems track hours worked, overtime, and leave balances to calculate wages and ensure accurate payments each pay period.

- Compliance expertise: Payroll services keep up with regulatory changes, such as updates to wage and tax laws that affect businesses. They align payroll processes with changing tax codes, labor regulations, and filing deadlines, which reduces the risk of penalties.

- Payment processing: Automatic payment processing reduces manual work and allows companies to distribute salaries and wages through various methods, such as direct deposit, checks, or payroll cards, so employees are paid on time.

What are the services of bookkeeping?

The services of bookkeeping include general ledger management, transaction classification, vendor tracking and 1099 management, collection of overdue invoices, and posting payroll.

The services of bookkeeping are listed below.

- General ledger management: Bookkeepers maintain the general ledger, where all transactions are posted. This service creates a central record of assets, liabilities, equity, revenue, and expenses, to provide reliable financial reporting.

- Transaction classification: Bookkeeping categorizes each financial activity as income, expense, asset, or liability. This classification provides clarity in reports and makes sure tax filings match the nature of the transactions.

- Track vendors and manage 1099s: Bookkeepers track vendor payments and prepare contractor forms such as 1099-NEC, which helps businesses meet reporting requirements and maintain supplier relationships.

- Past invoice collection support: Bookkeepers monitor accounts receivable and assist in following up on overdue invoices. This service improves cash flow and reduces the risk of bad debt.

- Posting payroll: Bookkeepers record payroll entries into the financial system to align salary expenses with company accounts. This helps to demonstrate labor costs in profit and loss statements.

- Bank reconciliation: This bookkeeping service compares business records with bank statements to detect errors, missing entries, or fraud. Reconciliation makes sure that cash balances in ledger books match account balances.

- Financial reporting: Bookkeepers prepare basic reports, such as trial balances, income statements, and balance sheets. These reports provide management with insights into performance and support tax filings.

What are the differences between payroll and bookkeeping?

The differences between payroll and bookkeeping are based on their purpose and focus, compliance, core tasks, effect on records, reports, transaction type, and policy development.

| Feature | Payroll | Bookkeeping |

| Purpose and focus | Manages employee compensation and benefits. | Manages overall financial records of the business. |

| Compliance | Compliance with labor laws and tax withholding rules. | Compliance with accounting standards and tax reporting. |

| Core tasks | Calculates wages, deducts taxes, issues payments, and files payroll taxes. | Records transactions, reconciles accounts, and prepares financial reports. |

| Effect on records | Updates employee-level records and generates payroll summaries. | Updates the ledger and generates accurate and reliable financial statements. |

| Reports | Pay slips, tax forms, and employee benefit records. | Ledgers, balance sheets, income statements, and cash flow reports. |

| Interaction | Interacts with HR and compliance teams. | Interacts with accountants, auditors, and management. |

| Software | Uses payroll-specific tools like ADP, Gusto, or QuickBooks Payroll. | Uses accounting software like QuickBooks, Xero, or FreshBooks. |

| Timing | Occurs periodically (weekly, biweekly, or monthly pay cycles). | Occurs continuously as transactions happen. |

| Transaction type | Salary, tax, and benefits transactions. | Sales, purchases, expenses, and vendor payments. |

| Policy development | Company HR policies and government labor laws. | Based on accounting principles and financial regulations. |

Purpose and focus

Payroll focuses on employee compensation, benefits, and deductions in compliance with government regulations and tax laws. Bookkeeping covers financial activities, which include sales, expenses, assets, and liabilities. Bookkeeping maintains the business’s financial records to accurately show its economic health.

Compliance

Payroll aligns with labor laws, wage regulations, and tax withholding rules, while bookkeeping complies with accounting standards and tax reporting rules that apply to business transactions.

Core tasks

Payroll handles wage calculations, deductions, benefits integration, and payment processing. Bookkeeping categorizes all transactions, reconciles accounts, and prepares the basic financial statements that show business operations.

Effect on records

Payroll updates employee-level records, such as earnings, deductions, and benefits, that support tax filings and regulatory compliance. Bookkeeping updates and organizes entries in ledgers and journals to produce accurate financial reports and remove errors in records.

Reports

Payroll produces pay slips, payroll summaries, and tax forms that show employee compensation details. Bookkeeping produces balance sheets, income statements, and cash flow statements that present the business’s financial data.

Interaction

Payroll interacts with HR and compliance teams to manage compensation policies, while bookkeeping works with accountants, auditors, and management to maintain financial transparency and strategic insight.

Software

Payroll uses specialized tools such as ADP, Gusto, or QuickBooks Payroll for wage calculation, tax filing, and benefit management. Bookkeeping uses accounting systems like QuickBooks, Xero, or FreshBooks, which focus on general accounting and financial recordkeeping.

Timing

Payroll follows fixed pay cycles, such as weekly, biweekly, or monthly, according to the pay periods decided by the employer. Bookkeeping records transactions continuously as they occur.

Transaction type

Payroll deals with salary, tax, and benefit transactions, while bookkeeping handles revenue, expenses, vendor payments, purchases, and general business transactions outside of payroll.

Policy development

Payroll policies are based on HR rules, labor laws, and compensation strategies, while bookkeeping policies are based on accounting standards, internal controls, and financial regulation frameworks.

What are the similarities between payroll and bookkeeping?

The similarities between payroll and bookkeeping include financial data management, record keeping, compliance support, and the use of specialized software.

Financial data management

Payroll and bookkeeping both deal with sensitive financial information. Payroll manages data related to employee earnings, deductions, and benefits, while bookkeeping manages sales, expenses, and overall company accounts to give an accurate overview of a company’s financial health.

Record keeping

Payroll and bookkeeping functions support accurate record keeping, which includes employee compensation histories and all business transactions. These records are important for businesses during audits, tax filings, and financial reviews.

Compliance support

Payroll supports compliance with wage laws and tax withholdings, and bookkeeping maintains compliance with accounting standards and reporting rules. Inaccuracies in both payroll and bookkeeping can lead to penalties or legal issues.

Use of specialized software

Payroll and bookkeeping processes use technology to improve accuracy and efficiency. Payroll software automates wage calculation, deductions, and reporting, while bookkeeping software manages transaction categorization, reconciliation, and reporting. The integration of these systems also helps businesses create more reliable financial reports.

Audit readiness

Payroll and bookkeeping provide verifiable records for internal and external audits. Payroll provides documentation of wages, deductions, and tax filings, and bookkeeping supplies ledgers and financial statements.

What are the use cases of payroll?

The use cases of payroll are human resources teams, accounting and finance teams, PEOs, business owners and management, employees, and government agencies.

The use cases of payroll are listed below.

- Human resources teams: HR relies on payroll to organize employee compensation packages, manage benefits, and maintain compliance with labor laws. Accurate payroll supports employee satisfaction and reduces disputes related to wages or benefits.

- Accounting and finance teams: Accountants and finance teams use financial data that payroll provides for budgeting, expense tracking, and preparing tax filings. Payroll entries are recorded in the general ledger, which allows finance teams to keep labor costs aligned with overall company accounts.

- PEOs (Professional Employer Organizations): PEOs use payroll systems to manage compensation, tax filings, and benefits on behalf of their client companies. This allows small and medium-sized businesses to gain access to enterprise-level payroll accuracy and compliance expertise without maintaining a large in-house HR team.

- Business owners and management: Business owners and executives use payroll data to measure labor costs, plan staffing, and assess profitability. Reliable payroll systems help them make strategic decisions.

- Employees: Payroll supports employees by delivering timely and accurate compensation, along with clear pay stubs, tax forms, and benefit records that strengthen transparency and trust in the workplace.

- Government and regulatory agencies: Tax authorities and labor departments track payroll submissions, which include information on income tax, social security, and other contributions. Proper payroll reporting helps businesses stay compliant and avoid penalties.

What are the use cases of bookkeeping?

The use cases of bookkeeping include business owners and executives, accounting and finance teams, external bookkeepers, investors and lenders, vendors and suppliers, and auditors.

The use cases of bookkeeping are listed below.

- Business owners and executives: Business owners and executives use bookkeeping to understand cash flow, profit margins, and overall financial health. Clear records help them make decisions about investment, expansion, or cost-cutting strategies.

- Accounting and finance teams: Accountants rely on bookkeeping to prepare financial statements, file taxes, and conduct audits. These records also support budgeting and forecasting activities.

- External bookkeepers: External bookkeepers and bookkeeping firms provide outsourced bookkeeping services and financial expertise to help businesses manage their financial records.

- Investors and lenders: Investors and banks review bookkeeping reports such as balance sheets and income statements to assess the financial stability of a business. Reliable bookkeeping builds trust and makes it easier to secure funding or credit.

- Tax authorities and regulators: Tax authorities and regulators rely on bookkeeping to provide the transaction records needed to calculate and verify taxes.

- Auditors: External and internal auditors use bookkeeping entries to trace transactions, check for irregularities, and confirm that financial statements are accurate. Bookkeeping organizes records to shorten the audit process and improve credibility.

- Vendors and suppliers: Vendors and suppliers benefit from accurate bookkeeping, as it helps them assess whether to trade with the business. Businesses track accounts payable to make sure vendors are paid on time, which strengthens supplier relationships and leads to better credit terms.

What are the benefits of payroll?

The benefits of payroll are better time management, accurate record keeping, and improved employee engagement. It keeps employee data secure and reduces costs.

Better time management

Payroll automation saves hours spent on repetitive manual tasks such as salary calculations, preparing tax slips, and other paperwork. It allows HR and finance staff to focus on workforce planning, compliance monitoring, and other strategic activities that add more value to the business.

Accurate record keeping

Payroll systems maintain structured records of employee earnings, deductions, tax withholdings, and benefit contributions. These records create an audit trail to support compliance, simplify tax preparation, and provide reliable documentation for both internal and external reviews.

Keeps employee data secure

Payroll involves sensitive data like salary details, identification numbers, and bank accounts. Modern payroll systems use encryption, access controls, and secure storage practices to reduce risks of fraud, identity theft, and unauthorized disclosure of employee information.

Improved employee satisfaction

Payroll supports timely and accurate salary payments that build trust between employees and management. Transparency in pay slips and benefit deductions increases employee satisfaction, improves morale, and increases staff retention. Strong workplace relationships build a positive employer reputation.

Reduced costs

Payroll automation and outsourcing lower administrative expenses by reducing the need for large HR teams and minimizing compliance mistakes. Accurate payroll saves money by preventing penalties, streamlining tax reporting, and maintaining reliable compensation and financial records.

Compliance with regulations

Payroll systems track wage laws, tax codes, and filing deadlines across jurisdictions. They automatically update deductions and contributions based on local regulations to reduce compliance risks, avoid costly penalties or legal disputes, and make sure employees and tax authorities receive accurate information on time.

Transparency for management

Payroll reports present a clear breakdown of labor costs, overtime spending, and benefits usage. This transparency gives managers accurate insights into workforce expenses, which helps them plan budgets, control costs, and make workforce decisions based on real-time financial data.

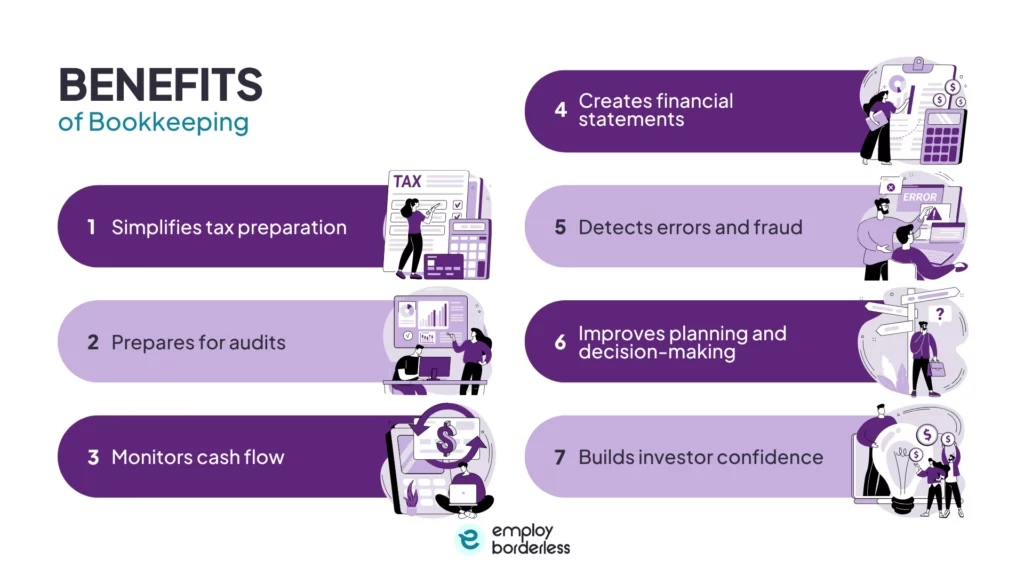

What are the benefits of bookkeeping?

The benefits of bookkeeping include simplifying tax and audit preparation. It also monitors cash flow, creates financial statements, and detects errors and fraud.

Simplifies tax preparation

Bookkeeping provides a clear, accurate, and organized record of income and expenses. This makes filing tax returns faster, minimizes missed deadlines, reduces errors, and helps claim eligible deductions. Bookkeeping also makes it easier to produce consistent, audit-ready documents and helps avoid last-minute financial crises.

Prepares for audits

Bookkeeping offers consistent and accurate records that provide auditors with detailed, chronological transaction records. This organization helps to trace activities back to the original documents. These reliable records also shorten the audit process and reduce the risk of penalties.

Monitors cash flow

Bookkeeping tracks inflows and outflows of money to help business owners understand and manage the company’s financial health and take immediate action. This clear visibility of cash flow gives real-time insights to prevent shortfalls and support smarter spending decisions.

Creates financial statements

Bookkeepers generate reports like balance sheets, income statements, and cash flow statements that reflect the business’s financial position. These reports give business owners insight into performance and help them secure loans or investments on time.

Detects errors and fraud

Regular bookkeeping and account reconciliation make it easier to spot unusual transactions or discrepancies. This early detection of errors helps to prevent small mistakes from becoming major issues, reduces the risk of any potential fraud or financial loss, and protects business credibility.

Improves planning and decision-making

Bookkeeping data highlights trends in revenue and expenses, which helps evaluate profitability and pricing strategies. Business owners and managers use this information to create budgets, set goals, and forecast growth. It allows executives to align business operations with future goals more effectively.

Builds investor confidence

Bookkeeping offers reliable, transparent, and consistent financial records that provide confidence to investors and reassure lenders about the financial stability of the business. Clean records showcase credibility and simplify credit evaluation to increase the chances of attracting funding.

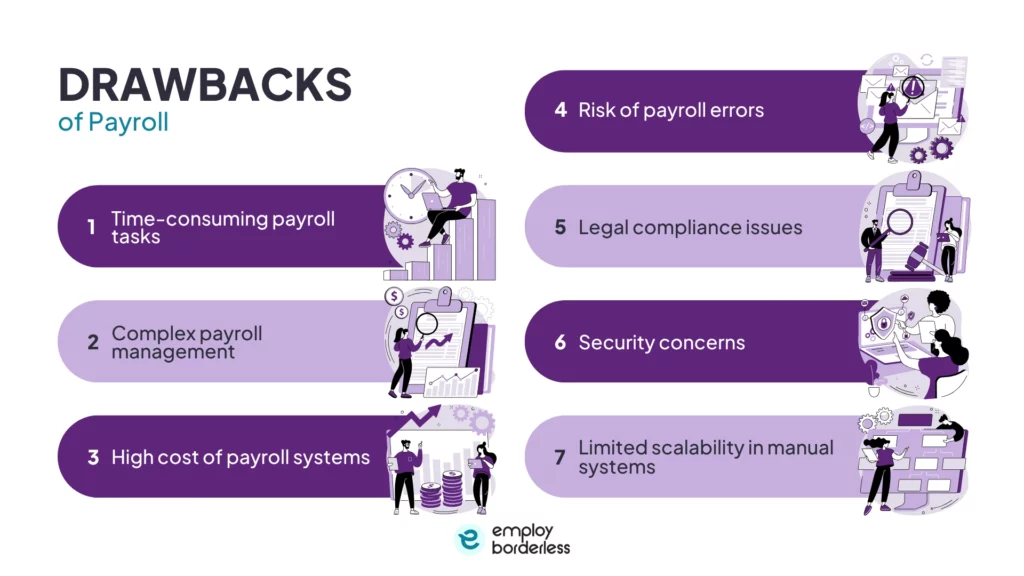

What are the drawbacks of payroll?

The drawbacks of payroll include time-consuming payroll tasks, complex payroll management, high cost of payroll systems, risk of payroll errors, and legal compliance issues.

The drawbacks of payroll are listed below.

- Time-consuming payroll tasks: Payroll requires gathering employee data, reviewing working hours, and handling exceptions like overtime or bonuses. Small businesses without dedicated staff struggle to keep up with these recurring tasks.

- Complex payroll management: Payroll involves multiple rules for taxes, benefits, and wage laws that vary by state or country. These complexities increase the risk of mistakes if management does not update the payroll system regularly.

- High cost of payroll systems: Running payroll software, maintaining compliance tools, or hiring payroll specialists is expensive for smaller firms, as these costs heavily impact budgets compared to manual methods.

- Risk of payroll errors: Payroll errors such as incorrect tax withholdings, miscalculated overtime, or missed benefit deductions cause employee dissatisfaction and trigger compliance issues. Errors also take extra time and money to correct.

- Legal compliance issues: Frequent changes to labor and tax laws require constant updates in the payroll system, as failure to comply can lead to audits, fines, or even lawsuits that damage business credibility.

- Security concerns: Payroll stores sensitive employee data, such as salaries and social security numbers, so weak data protection exposes businesses to cyber risks and identity theft.

- Limited scalability in manual systems: Manual payroll systems become slow and prone to errors in growing businesses. A manual system also limits scalability, delays payroll processes such as payments, and disrupts operations.

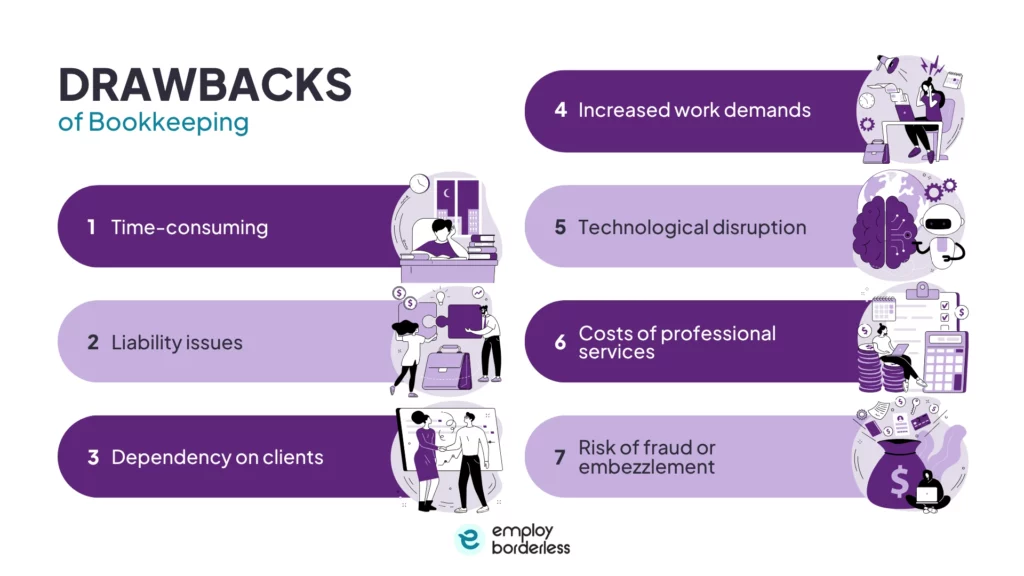

What are the drawbacks of bookkeeping?

The drawbacks of bookkeeping include being time-consuming, liability issues, dependency on clients, increased work demands, and technological disruption.

The drawbacks of bookkeeping are listed below.

- Time-consuming: Bookkeeping involves recording every transaction, reconciling accounts, and preparing reports, all of which are time-consuming. Small business owners who manage their own books spend a lot of time on bookkeeping, which reduces the time they can spend on core operations.

- Liability issues: Mistakes in bookkeeping result in incorrect financial statements or tax filings. These errors create liability risks, such as penalties, audits, and damage to relationships with lenders and investors.

- Dependency on clients: In outsourced bookkeeping, accuracy depends on how quickly clients provide invoices, receipts, and bank statements. Delays or incomplete documents slow down the process and compromise reporting.

- Increased work demands: Scaling bookkeeping without a proper system in a growing business overburdens staff, as the volume of transactions also increases. This often leads to missed or incorrect entries and delayed reconciliations.

- Technological disruption: Businesses that rely on outdated systems face disruptions in bookkeeping processes, but learning new tools or switching to modern platforms can be costly and stressful.

- Costs of professional services: Hiring qualified bookkeepers or accountants is expensive for smaller firms, and software comes with subscription costs and requires oversight.

- Risk of fraud or embezzlement: Lack of internal control in bookkeeping makes it easier for unauthorized changes or fraudulent activities to go unnoticed. This weak oversight increases the risk of financial loss.

When should a business consider outsourcing payroll and bookkeeping?

A business should consider outsourcing payroll and bookkeeping when it lacks internal expertise, has compliance risks, needs to reduce costs, is scaling rapidly, struggles with delayed financial closing, or wants to refocus on its core operations.

A business should evaluate the workload during tax season or financial closing, as these periods require accurate filings and leave no room for error. Outsourcing allows faster reporting, real-time dashboards, and financial clarity.

A business should assess its current team’s ability to keep up with changing tax codes, labor laws, or reporting standards without subjecting the company to compliance risks. The financial impact of manual errors should also be considered, as mistakes in payroll or bookkeeping can lead to costly penalties or strained employee relationships.

The companies should also consider their business size as internal payroll and bookkeeping teams require salaries, benefits, software, training, and infrastructure costs.

Outsourcing also becomes a strategic choice when a company scales rapidly, expands into new regions, or introduces more complex benefit structures that require specialized knowledge.

The businesses should also consider delegating payroll and bookkeeping to professional providers to save time and focus on growth, planning, and customer relationships rather than administrative tasks.

Which is better: Payroll or bookkeeping?

Payroll and bookkeeping are both important for a business to function properly, as each serves a different purpose. Payroll manages employee compensation and compliance with labor laws, while bookkeeping manages overall financial records and reporting. A business needs both functions to operate effectively.

What are the types of payroll systems?

The types of payroll systems are manual payroll systems, payroll software systems, online payroll services, payroll card systems, and outsourced payroll systems.

Does a bookkeeper pay invoices?

Yes, a bookkeeper pays invoices as part of managing accounts payable. They record supplier bills, schedule payments, and make sure vendors are paid on time. This role keeps business expenses organized, maintains vendor relationships, and prevents late fees.

Is payroll more HR or accounting?

Payroll involves different functions of both HR and accounting. HR provides employee data, manages benefits and compliance with labor laws, while accounting records payroll expenses, files tax reports, and integrates payroll data into the company’s financial system. It is a joint practice of both HR and the accounting department, which depends on the company’s size, structure, and work culture.

Does a small business need bookkeeping?

Yes, a small business needs bookkeeping for recording sales, expenses, and cash flow, which keeps the financial documents clear and helps to file taxes correctly. Businesses risk inaccurate records, compliance issues, and poor decision-making without bookkeeping. Proper bookkeeping also makes it easy to apply for loans, attract investors, and plan for sustainable growth.

Is outsourcing payroll more cost-effective?

Yes, outsourcing payroll is more cost-effective for many businesses, as it reduces the need to hire specialized staff, lowers software and training expenses, and removes the risk of compliance penalties. Outsourcing payroll offers expertise and automation that save time and money, especially for small and medium-sized businesses with limited resources or complex payroll requirements.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations