Global payroll taxation: systems, challenges, and management strategies

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll taxation refers to taxes imposed on employees’ wages, salaries, or compensation. Payroll taxation is important globally because it funds social insurance programs like Social Security, healthcare, and unemployment benefits, which support economic stability and provide long-term security for employees.

The different global payroll tax systems vary from each other in terms of complexity, tax burden, statutory requirements, and the types of social programs funded. These include the payroll tax system of different countries such as France, Germany, Belgium, Switzerland, and the United States.

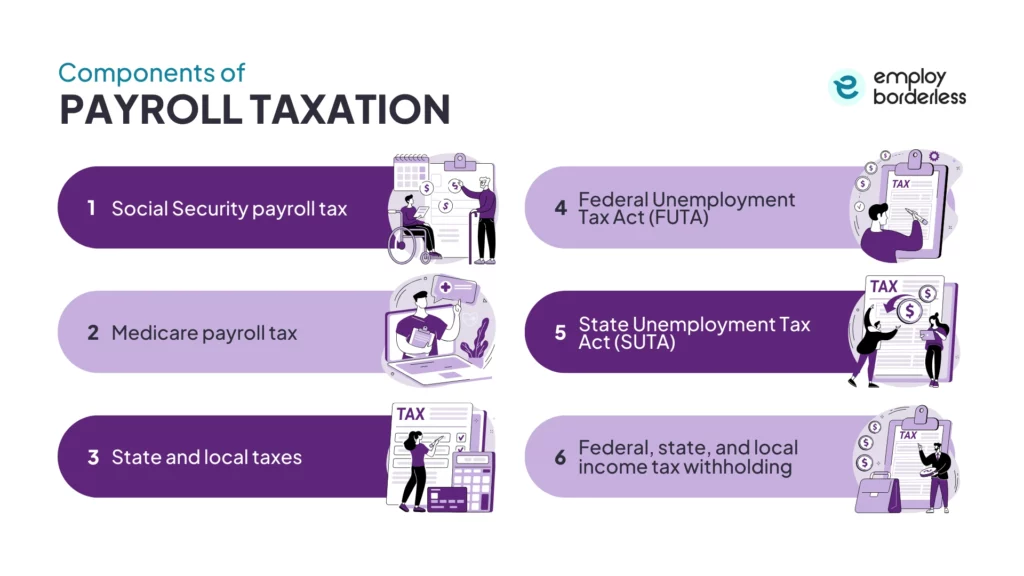

The main components of payroll taxation are Social Security payroll tax, Medicare payroll tax, state and local taxes, Federal Unemployment Tax Act (FUTA), State Unemployment Tax Act (SUTA), and federal, state, and local income tax withholding.

Payroll taxation comes up with many different challenges including diverse tax regulations, double taxation, fluctuations in currency, compliance with digital economy taxation, worker classification issues, and varying taxable wage bases.

The strategies to enhance global payroll tax management include automating payroll processes, consolidating payroll services, leveraging advanced tax technology, conducting regular audits, and staying informed on tax legislation updates.

What is payroll taxation?

Payroll taxation is a tax imposed on wages and salaries paid to employees, collected through withholding from employee paychecks and contributions by employers, to fund social insurance programs such as Social Security, Medicare, and unemployment benefits.

In payroll taxation, both employees and employers share the responsibility of paying taxes based on employee compensation. These taxes are deducted directly from employees’ earnings by employers, who then remit the amounts to government authorities. The funds collected through payroll taxes support various public programs, including retirement benefits, healthcare coverage, and unemployment insurance. Payroll taxes can include federal, state, and local components, each with specific rules and rates.

How does payroll tax work?

Payroll tax works by employers withholding specific amounts from employees’ wages for taxes like federal income tax, Social Security, and Medicare. Employers also contribute their share of Social Security and Medicare taxes. The withheld amounts and employer shares are then reported and deposited with tax authorities according to specific deadlines.

How does the global payroll tax system differ?

Global payroll tax systems differ significantly across countries in terms of complexity, tax burden, statutory requirements, and the types of social programs funded. European countries, such as France, Germany, and Belgium, have the most complex payroll requirements, which usually involve multiple layers of statutory reporting, data retention, and submissions to various authorities, according to a report titled, “2021 Global Payroll Complexity Index” published by Alight.

In most OECD countries, payroll taxes have a larger share of the total tax burden on labor than income taxes. The tax burden on labor is usually higher in Europe, as Belgium has one of the highest payroll tax burdens, with a tax wedge of approximately 52.7% of labor costs, according to a report titled “Taxing Wages 2024” published by OECD, while countries like Switzerland have much lower rates around 23.5% in 2023 according to a report titled, “Taxing Wages – Switzerland” published by OECD.

In the United States, payroll taxes fund Social Security and Medicare through the Federal Insurance Contributions Act (FICA). Employers and employees both pay 6.2% for Social Security and 1.45% for Medicare, with additional Medicare surtaxes for high earners, as confirmed by the IRS Topic No. 751 and IRS Publication 926.

What are the components of payroll taxation?

The components of payroll taxation are Social Security payroll tax, Medicare payroll tax, state and local taxes, Federal Unemployment Tax Act (FUTA) tax, State Unemployment Tax Act (SUTA) tax, and federal, state, and local income tax withholding.

Medicare payroll tax

Medicare payroll tax is a mandatory tax withheld from employees’ wages and contributed by employers to fund the federal Medicare program.

Medicare payroll tax is 1.45% for both employers and employees, totaling 2.9%, with no income cap, according to IRS Topic No. 751. Self-employed individuals pay the full 2.9% directly, according to a report titled, “Self-employment tax (Social Security and Medicare taxes” published by IRS (International Revenue Service). For example, if an employee earns $50,000 in a year, $725 ($50,000*1.45%) is withheld from their pay for Medicare tax, and the employer matches this amount for a total annual contribution of $1,450. The 0.9% Additional Medicare Tax applies to employees earning over $200,000, but employers do not match this surtax, according to IRS Topic No. 751.

State and local taxes

State and local taxes, or State and Local Tax Deduction (SALT Deduction), are taxes imposed by U.S. state and local governments, including income, property, and sales taxes, to fund public services and institutions.

State and local taxes are imposed by state and municipal governments in various forms, such as income, sales, and property taxes, with rates, rules, and collection methods that differ by jurisdiction to fund local and state services.

These tax laws vary based on the specific rates set by their respective local jurisdictions. For example, 41 states and the District of Columbia charge individual income taxes that usually begin with the federal AGI (Adjusted Gross Income), but each state calculates taxable income differently by excluding some items or allowing special deductions that the federal government does not, according to an article titled, “How do state and local individual income taxes work?” published by Tax Policy Center.

Federal Unemployment Tax Act (FUTA)

The Federal Unemployment Tax Act (FUTA) is a U.S. federal law that imposes a payroll tax on employers to fund unemployment benefits through state workforce agencies.

FUTA finances the federal share of unemployment insurance (UI) and job service program administration in every state. It also pays half the cost of extended unemployment benefits during periods of high unemployment and maintains a trust fund that states can borrow from to cover benefit payments when needed. As of 2025, the FUTA tax rate is 0.6% on the first $7,000 of wages paid to each employee annually, according to a report titled, “Topic no. 759, Form 940, Employers Annual Federal Unemployment (FUTA) Tax Return – filing and deposit requirements” published by IRS (International Revenue Service).

State Unemployment Tax Act (SUTA)

The State Unemployment Tax Act (SUTA) is a state-level tax law that requires employers to pay a state tax that helps fund unemployment benefits for workers who have lost their jobs.

SUTA tax rates are experience-rated, meaning each employer’s rate is adjusted annually based on their recent history of layoffs and unemployment claims. The taxable wage base varies for State Unemployment Tax Act (SUTA) taxes vary by state. For example, Texas has a wage base of $9,000 with employer tax rates ranging from 0.25% to 6.25%, according to an official government statistics report titled, “Unemployment Insurance Tax Rates” by Texas Workforce Commission.

Federal, state, and local income tax withholding

Federal, state, and local income tax withholding is the process where employers deduct estimated income taxes from employees’ paychecks and remit them to the respective federal, state, and local tax authorities like the IRS, based on applicable laws and employee information.

Income tax withholding at different levels is determined by employers using information from employees’ Form W-4 and relevant state forms, with the amount withheld based on wages, pay period, and declared allowances. State and local income tax withholding rates vary by jurisdiction, with some states having flat rates, others progressive brackets, and a few states imposing no income tax at all. For example, Colorado uses a flat tax rate of 4.4%, while others like Wyoming have no state income tax, according to a research article titled, “State Individual Income Tax Rates and Brackets, 2025” published by Tax Foundation.

What are the challenges of managing global payroll taxes?

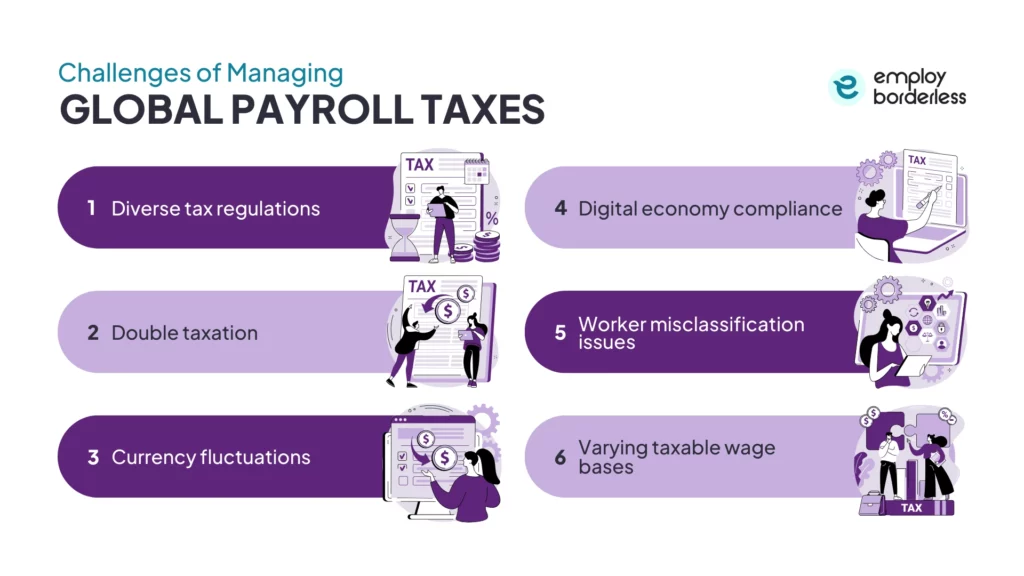

The challenges of managing global payroll taxes include diverse tax regulations, double taxation, fluctuations in currency, compliance with digital economy taxation, worker classification issues, and varying taxable wage bases.

The challenges of managing global payroll taxes are listed below.

- Diverse tax regulations: Diverse tax regulations are the varying rules and guidelines established by different governments that dictate how taxes are calculated, reported, and paid across jurisdictions. For example, new global tax rules called Pillar Two require big companies to pay at least a 15% tax rate in every country they operate, making tax calculations and reporting more complicated for these businesses, according to an article titled, “Global Anti-Base Erosion Model Rules (Pillar Two)” published by OECD.

- Double taxation: Double taxation is when taxes are paid twice on the same source of income. It can be taxed when an income is taxed at the corporate or personal level. This usually affects multinational companies with operations, subsidiaries, or investments across various countries. For example, in 2022, U.S. multinational corporations faced an average effective foreign tax rate of about 17.6% on their foreign profits, while also being subject to U.S. taxation on worldwide income, according to an article titled, “How Heavily Taxed Are U.S. Multinationals?” published by Tax Foundation.

- Currency fluctuations: Currency fluctuations mean the changes in the value of one currency relative to another. Exchange rate fluctuations can increase or decrease the actual amount employees receive. It also causes inconsistencies in compensation and difficulties in budgeting for businesses. A 10% appreciation in the value of the U.S. dollar causes significant wage declines for less-educated U.S. workers who change jobs, according to a research titled, “Exchange Rates and Wages” by Federal Reserve Bank of New York.

- Digital economy compliance: Digital economy compliance refers to the adherence to tax and regulatory obligations for digital transactions, goods, and services, usually across borders and without a physical presence. These digital business models make it difficult to determine where taxes should be paid and how profits and payroll should be allocated. For example, U.S. companies face significant barriers and legal uncertainty when foreign regulations require local data storage and processing for digital transactions, according to a report titled, “2024 National Trade Estimate Report on Foreign Trade Barriers (NTE Report)” by USTR.

- Worker misclassification issues: Worker misclassification occurs when an employer treats a worker who is an employee as an independent contractor. When a business misclassifies its workers, it faces payroll taxation consequences, including liability for unpaid employer and employee portions of Social Security and Medicare taxes (FICA), as well as back taxes. The penalty is $50 per failure to file a correct information return (such as Form W-2) if filed within 30 days of the due date, with higher penalties for later filings or intentional disregard, according to a report titled, “Information return penalties” published by IRS.

- Varying taxable wage bases: Variable wage bases refer to the maximum amount of an employee’s income that can be taxed for specific payroll taxes. Wage bases differ by country, state, or even city, and businesses find it difficult to comply with multiple limits across jurisdictions. For example, there are major variations in wages across over 395 metropolitan areas and all 50 states, which shows the complexity companies face in managing payroll and tax compliance across diverse locations, according to a statistics report titled, “Overview of BLS Wage Data by Area and Occupation” by U.S. Bureau of Labor Statistics.

What strategies can enhance global payroll tax management?

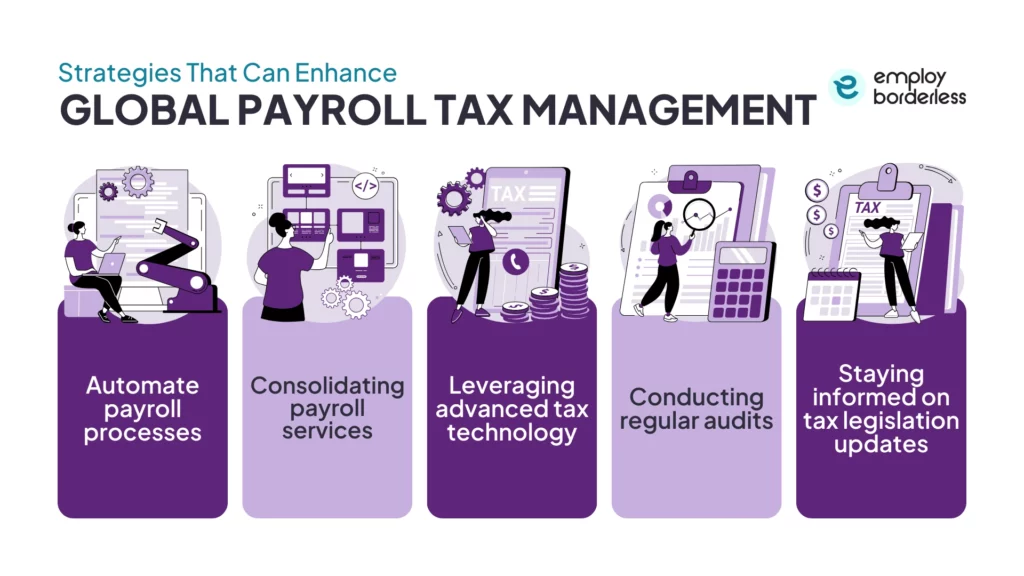

The strategies that can enhance global payroll tax management are automating payroll processes, consolidating payroll services, leveraging advanced tax technology, conducting regular audits, and staying informed on tax legislation updates.

Automate payroll processes

Payroll automation means using technology and specialized software to automate different payroll tasks, such as calculating wages, tracking hours, deducting taxes, and creating paychecks.

Companies operating in multiple countries have to follow the tax codes of each jurisdiction, which takes a lot of time and resources to manage. Automating the payroll process saves time and reduces manual errors. They also provide real-time insights into businesses’ global payroll operations at any given time. Automation also reduces the costs that are associated with manual payroll errors and also prevents compliance penalties. Companies that use automated payroll systems do not need to hire large, specialized payroll teams to process their payroll.

Consolidating payroll services

Consolidating payroll services means centralizing payrolls of different countries by combining different payroll vendors and systems an organization uses to manage payroll across all geographies into a single centralized platform.

This consolidation process puts all payroll functions of different countries into one platform and makes it easier for companies to comply with local tax laws and keep data accurate. Businesses that consolidate their payroll services avoid any confusion of dealing with multiple vendors and systems, so HR teams can handle compliance, reporting, and tax updates for every country from a single source.

Leveraging advanced tax technology

Leveraging advanced tax technology means using specialized software and digital tools to simplify, automate, and improve various tax-related processes such as compliance, planning, and management.

Advanced tax technologies help companies automate complex tax calculations, provide real-time updates of local tax laws, and reduce human errors across multiple regions. This improves compliance with different regulations, makes payroll processing faster, and lowers the risks of costly penalties. For example, cloud-based payroll systems provide centralized access to payroll data worldwide, automatically apply country-specific tax rates, and update regulatory changes.

Conducting regular audits

Conducting regular audits means a professional accountant systematically reviews and verifies a company’s financial records and processes regularly.

Businesses perform audits to find errors, verify accurate tax withholdings, and ensure compliance with tax laws and rules. Auditors start by reviewing the company’s payroll processes and procedures. This step includes examining the policies and procedures about payroll activities, such as determining pay rates, calculating overtime, and administering employee benefits.

Staying informed on tax legislation updates

Staying informed on tax legislation updates means keeping up-to-date with changes in tax laws, regulations, and payroll requirements that affect how businesses process and report payroll taxes.

Businesses stay aware of changing tax laws and payroll regulations in each country they operate. This knowledge allows companies to calculate and withhold taxes accurately, adjust payroll processes quickly, and maintain compliance with local requirements. This strategy helps businesses avoid financial penalties and legal issues and also shows business as a trustworthy and reliable employer.

What is a payroll?

Payroll is the process through which businesses manage and distribute employee salaries and compensations. Payroll is calculated and processed by following related company policies and legal regulations to ensure it goes smoothly and the employees are paid accurately.

Calculating payroll involves tracking employee work hours, adding up the earnings, withholding taxes, and ensuring salary payments are given on time. Having a proper payroll system guarantees that employees are paid correctly and on time and also helps businesses meet tax obligations, maintain financial records, and comply with labor laws.

What are the different types of payroll?

The different types of payroll are salary payroll, hourly payroll, commission-based payroll, piece rate payroll, and hybrid payroll. These payroll types help businesses accurately calculate employee earnings according to various work arrangements and compensation models.

What are the benefits of outsourcing payroll services?

The benefits of outsourcing payroll services are time-saving, cost-saving, accuracy and precision, compliance with laws, access to expertise, improved data security, employee satisfaction, focus on business, reduced stress, and faster payroll processing.

What is payroll compliance and why is it important?

Payroll compliance involves following the rules and regulations related to employee pay, tax deductions, benefits, and reporting. It requires employers to correctly calculate and pay taxes, keep accurate payroll records, and follow labor laws like minimum wage, overtime pay, and social security contributions. It is important because it helps businesses avoid penalties, audits, and legal disputes.

What information is needed to process payroll?

The information needed to process payroll includes employee personal details like Social Security number, marital status, and bank information. The payroll process also includes information about base salary, overtime rates, benefits, hours worked, PTO (Paid Time Off) taken during the pay period, and any compensation changes and updates to employee personal information.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations

Social Security payroll tax

Social Security payroll tax is a tax applied on employers and employees, including self-employed individuals, to fund the Social Security program in the United States.

The Social Security tax funds the Social Security program, which pays for retirement, disability, and survivorship benefits to more than 69 million Americans every month, according to a fact sheet published by SSA (Social Security Administration) in 2025. For example, in the U.S., employees and employers each pay 6.2% on earnings up to $168,600 in 2024, so someone earning $100,000 would contribute $6,200 ($100,000*6.2%), matched by their employer, according to a report titled, “2024 Social Security and Medicare Tax Withholding Rates and Limits” published by USPS (United States Postal Service).