Payroll risk management: definitions, strategies, and benefits

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll risk management is the process of identifying, assessing, and mitigating risks in your payroll operations, including fraud, compliance violations, calculation errors, data security threats, and business continuity failures. Each risk category carries specific financial exposure, from IRS deposit penalties (2% to 15%) and Trust Fund Recovery Penalty personal liability (100% of unpaid trust fund taxes) to employee lawsuits, data breach costs, and reputational damage.

PwC’s 2022 Global Economic Crime and Fraud Survey found that 46% of surveyed organizations experienced fraud, corruption, or other economic crimes in the preceding 24 months (across all fraud types, not payroll-specific), with approximately 31% of cases involving an internal employee. For payroll specifically, a December 2022 EY analysis (commissioned by Paycom) of 508 US companies found self-reported average payroll accuracy of approximately 80%, with an average of 15 corrections per pay period. At approximately $291 per correction (EY’s estimate of direct and indirect costs), a company running biweekly payroll could face over $113,000 per year in correction costs alone.

Nearly two-thirds (63%) of firms say compliance is their biggest payroll-related challenge, according to PrimePay research. More than half (53%) of companies have been penalized for payroll noncompliance in the last five years, with the total cost of noncompliance exceeding $845 per employee annually when accounting for fines, back wages, penalties, and internal remediation. One in three US workers has left a company due to payroll problems, making payroll risk management not just a compliance concern but a retention issue.

What are the main categories of payroll risk?

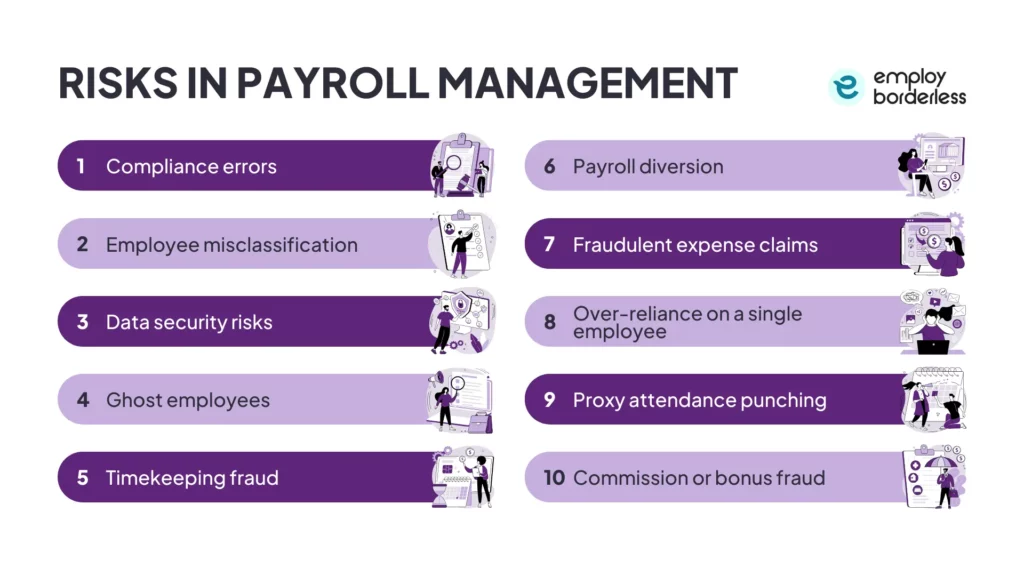

Payroll risks fall into five categories, each requiring different controls.

Risk Category | Examples | Financial Exposure | Primary Control |

Fraud | Ghost employees, timekeeping fraud, payroll diversion, buddy punching, commission fraud | Direct financial loss + investigation costs. Indianapolis Bond Bank case: $400K stolen via unauthorized pay. | Segregation of duties, audit trails, MFA, mandatory vacation for payroll staff |

Compliance | Incorrect tax withholding, missed filing deadlines, worker misclassification, wage garnishment errors | IRS penalties 2%-15%, TFRP 100% personal liability, state fines, class action exposure | Automated tax updates, regular compliance audits, compliance calendar |

Process | Calculation errors, missed deductions, incorrect overtime, data entry mistakes | ~$291 per error (EY/Paycom 2022); $113K+/year at 15 corrections per biweekly cycle | Payroll automation, pre-run validation, approval workflows, variance analysis |

Data Security | Phishing, payroll diversion, insider threats, system breaches, outdated security software | $2.77B in BEC losses reported to FBI IC3 in 2024; avg $4.88M per data breach (IBM 2024) | MFA, encryption, role-based access, security training, dedicated payroll system |

Continuity | System outages, provider failures, key-person dependency, disasters, staff turnover | Late payroll penalties + employee trust damage + operational disruption | Provider SLA review, cross-training, cloud redundancy, documented SOPs |

What are the most common payroll fraud risks?

The most common payroll fraud risks are ghost employees, timekeeping fraud (including buddy punching), payroll diversion, and fraudulent expense or commission claims. Each exploits different weaknesses in payroll controls.

Ghost employees

Ghost employees are fictitious workers added to the payroll by someone with system access. The perpetrator creates or alters records to issue paychecks to nonexistent employees, routing payments to their own account or an accomplice’s. In 2018, two former employees of the Indianapolis Bond Bank were charged with theft after stealing nearly $400,000 in unauthorized pay. One employee, who handled payroll, was paid $170,000 in 12 months despite an annual salary of $57,500. Ghost employee fraud is most common in organizations where one person controls both payroll data entry and payment authorization, which is why segregation of duties is a foundational defense.

Timekeeping fraud

Timekeeping fraud involves employees falsifying their recorded work hours to receive pay for time not worked. Buddy punching (one employee clocking in for another) is the most basic form. Automated time and attendance systems with biometric verification or GPS-based clock-in reduce this risk significantly, but employers must evaluate biometric privacy laws before deploying biometric timekeeping. Illinois’s BIPA has generated class action settlements in the tens of millions (including BNSF’s $228M jury verdict after the Cothron decision affirming per-scan violations), and Texas, Washington, New York, Oregon, Maryland, and Colorado also have biometric privacy laws. GPS-based alternatives avoid biometric exposure while still preventing buddy punching.

Payroll diversion fraud

Payroll diversion fraud occurs when attackers use phishing to obtain employee login credentials and redirect direct deposit payments to fraudulent bank accounts. The FBI’s Internet Crime Complaint Center reported approximately $2.77 billion in total business email compromise (BEC) losses in 2024 across 21,442 complaints. Prevention requires multi-factor authentication on all payroll systems, a two-channel verification rule for any direct deposit change (if the request comes via email, verify via phone or video call), and employee security training focused on phishing recognition.

What compliance risks do payroll operations face?

Payroll compliance risks include incorrect tax withholding, missed deposit deadlines, failure to file quarterly and annual returns, worker misclassification, wage garnishment errors, violations of wage and hour laws, and unclaimed property obligations.

Federal deposit penalties

Federal deposit penalties under IRC Section 6656 escalate from 2% (1-5 days late) to 5% (6-15 days late) to 10% (16+ days late) to 15% (10 days after IRS notice and demand). These are separate from failure-to-file penalties on Form 941 under IRC Section 6651(a)(1) (5% per month, capped at 25%) and failure-to-pay penalties under Section 6651(a)(2) (0.5% per month, capped at 25%). When both apply, the failure-to-file rate is reduced by the failure-to-pay amount. Both penalty types can stack on the same quarter.

Trust fund recovery penalty

The Trust Fund Recovery Penalty (TFRP) under IRC Section 6672 creates personal liability for any responsible person who willfully fails to remit withheld income taxes and the employee share of FICA. The assessment equals 100% of the unpaid trust fund amount (not including the employer’s FICA match). This liability is generally not dischargeable in bankruptcy under 11 U.S.C. § 523(a)(1)(A) and § 507(a)(8)(C) and can be pursued for the 10-year collection period under IRC Section 6502.

Worker misclassification

The National Employment Law Project estimates that 10% to 30% of employers misclassify at least some workers. Misclassifying employees as independent contractors avoids FICA, FUTA, benefits, and workers’ comp obligations, but creates back-tax liability, retroactive penalties, and potential class action exposure. PwC has found that businesses underpay staff by approximately $1.35 billion in aggregate each year, with misclassification contributing significantly to that figure. IRC Section 3509 provides reduced-rate relief for non-willful misclassification, but willful cases are prosecuted under IRC § 7201 or § 7202.

Wage garnishment compliance

Wage garnishment compliance under Title III of the Consumer Credit Protection Act requires employers to correctly calculate the 25% disposable earnings cap, apply the correct withholding order priority (child support takes precedence over creditor garnishments), and avoid retaliating against employees for garnishment orders. Garnishment errors are among the most common sources of payroll-related litigation. Employers routinely face lawsuits for failing to process garnishments correctly, improperly terminating withholding orders, or exceeding the legal cap.

Unclaimed property obligations

Unclaimed property obligations arise when paychecks go uncashed or terminated employee payouts aren’t claimed within state-defined dormancy periods (typically 1 to 3 years). Multi-state employers must track each state’s escheat requirements and report unclaimed property to the appropriate state. Failure to escheat creates audit exposure, as state unclaimed property auditors increasingly target payroll records during examinations.

Multi-state payroll complexity

The rise of remote and distributed workforces has significantly increased multi-state payroll complexity. Employees working in states different from the company’s headquarters trigger new tax registrations and reporting duties. State and local tax differences, paid leave mandates, and wage laws vary widely. Some states legally require employers to pay employees twice a month. If you open a new branch or hire someone remotely in such a state, you face compliance obligations you may not have anticipated. Maintaining a compliance calendar that tracks filing deadlines across all jurisdictions where you operate is essential for managing this complexity.

How do you implement segregation of duties in payroll?

Segregation of duties means splitting the payroll process across multiple people so that no single individual controls data entry, approval, payment authorization, and bank reconciliation. The ACFE’s Report to the Nations consistently ranks it as one of the most effective anti-fraud controls, alongside management review, internal audit, and anonymous reporting hotlines.

Divide payroll into four roles

At a minimum, divide payroll into four roles. The data entry role adds and modifies employee records, pay rates, and banking details. The processing role runs payroll calculations and generates the payroll register. The approval role reviews the payroll register and authorizes payment. The reconciliation role compares the bank statement to the payroll register after payment. No person should hold more than one of these roles.

Compensating controls for small businesses

In small businesses where headcount makes full segregation impractical, implement compensating controls. The most effective small-business control is requiring the business owner to personally review the payroll register against an independent source (bank statement or prior-period comparison) before every payroll run. Additionally, require a second person to sign off on any change to employee banking information. Run monthly variance reports and investigate any paycheck that varies by more than 5% or $500 from the prior period, whichever is lower. If your business has only one payroll employee, assign a qualified backup (such as someone in accounting) and consider outsourcing to create a natural separation between authorization and processing.

What internal controls should every payroll system have?

Beyond segregation of duties, effective payroll risk management requires a layered set of internal controls that work together to prevent, detect, and correct payroll errors and fraud.

Regular payroll audits: Conduct both scheduled and surprise payroll audits. ACFE data shows surprise audits reduced median fraud loss by 51% and fraud duration by 50%. During audits, cross-reference the payroll roster against the HR employee directory, verify leave accrual balances, compare budget reports against actual benefit expenditures, and run exception reports for unusual overtime or pay rate changes.

Dedicated payroll bank account: A separate bank account for payroll reduces the number of company assets at risk. Even if payroll fraud occurs, losses are limited to that account. The account should only contain enough funds to process and complete payroll. All other business funds should be in a separate account. This also simplifies audits and reconciliation.

Variance analysis: Organizations should know how much they spend each payroll cycle. If payroll in one period significantly deviates from the average, that could indicate errors or fraud. Segregate payroll data by department and compare against both the current budget and prior-year actuals. Any major variance should trigger an investigation.

Check signing authority: Implement a dual-control system where two authorized individuals must sign payroll checks or approve electronic payment releases. Maintain a documented list of authorized signatories and compare against every payment before release.

Management review: A member of company management (or the business owner) should periodically review payroll records. Managerial oversight ensures proper record-keeping and reduces fraud risk. Review should include comparing W-2 counts against the active employee roster and verifying that payroll totals align with budgeted amounts.

Digitized time tracking: Time and attendance software addresses incorrect timekeeping, payroll mistakes, and fraud. Require supervisor approval on every employee’s time card before it can be sent to payroll for processing. Once approved, the employee should not be able to modify the timesheet.

What data security controls does payroll require?

Payroll data security requires multi-factor authentication (MFA), role-based access control (RBAC), encryption at rest and in transit, and regular security audits to protect Social Security numbers, bank account details, salary information, and tax records.

Role-based access: Each user can only see and modify the data required for their specific function. A department manager might have view-only access to approve timecards, while only the payroll administrator can change bank details. For any change to direct deposit routing, implement a two-channel verification rule. If the request arrives by email, confirm via phone or video call. Never verify through the same channel from which the request came. All users should have individual login credentials (never shared), with every sign-in and event tracked and logged.

SOC 2 Type II and ISO 27001: When evaluating payroll providers, ask specifically for SOC 2 Type II reports (which cover controls over a reporting period of 6 to 12 months) rather than Type I (point-in-time only). Also, confirm the scope of any ISO 27001 certification, as scope definitions can be narrow. The California Consumer Privacy Act (CCPA) governs payroll data for California employees. GDPR applies to any employee in the EU regardless of employer location. Compliance with these frameworks should be verified during provider due diligence, not assumed. When choosing a payroll provider, make security certifications a non-negotiable evaluation criterion.

System security hygiene: Ensure all computers used for payroll have regularly updated anti-virus and anti-malware software and are behind a firewall. Consider performing payroll and banking tasks on a separate, dedicated system used only for those purposes. Change passwords to payroll-related systems whenever there is a change in payroll administration personnel. Outdated security software renders your payroll system vulnerable to cyberattacks, making regular updates a non-negotiable control.

How do you conduct a payroll risk assessment?

A payroll risk assessment identifies where your current payroll process is vulnerable, assigns a severity and likelihood score to each risk, and prioritizes which controls to implement first.

Map your entire payroll workflow: Start by mapping your entire payroll workflow from data collection through payment and reconciliation.

Identify every vulnerability point: Identify every point where data is entered, transferred, calculated, approved, or paid. Each of these is a potential point of leakage or error.

Score each risk: For each step, ask three questions. Who has access? What could go wrong? What would it cost? Score each risk on a 1-5 scale for both likelihood and financial impact. Multiply the two scores to get a priority ranking. A risk with likelihood 4 and impact 5 (score 20) gets addressed before a risk with likelihood 2 and impact 3 (score 6).

One important exception to scoring. Regulatory compliance obligations (FICA withholding, Form 941 filing, state tax deposits) are non-negotiable regardless of their risk score. These are mandatory mitigations that sit outside the prioritization framework. Focus scoring on discretionary controls like the level of automation, the frequency of audits, or the scope of security training. Review the assessment quarterly (or immediately when your payroll process changes through new states, new benefit programs, system migration, or headcount changes).

What should a payroll business continuity plan include?

A payroll business continuity plan ensures employees get paid on time even when normal payroll operations are disrupted by system outages, provider failures, key-person absences, or cyberattacks.

Provider and technology risks

For companies using cloud-based payroll (Gusto, Rippling, ADP, Paychex), the real continuity risks are provider outages, provider financial failure (as when MyPayrollHR collapsed in 2019, stranding employer funds), and cyberattacks on the provider (as in the December 2021 UKG Kronos ransomware incident, which disrupted payroll for weeks). The continuity plan should include a review of your provider’s SLA and uptime guarantees, verification that payroll funds are held in escrow or trust accounts (not commingled with provider operating funds), a documented switch-provider contingency plan, and an export of current payroll data and configurations stored independently.

Key-person dependency and staff turnover

Key-person dependency remains a fundamental risk regardless of technology. If only one person knows how to run payroll and they’re unavailable, the business can miss a payroll cycle. Cross-training so that at least two people can execute every step of payroll, combined with documented standard operating procedures, eliminates this single point of failure. Test the backup procedure at least once per year. Staff turnover in the payroll function creates additional risk. If a payroll administrator leaves, immediately revoke their system access, change all payroll-related passwords, and ensure the transition is documented. Manual payroll systems are especially vulnerable to brain drain because institutional knowledge lives in one person’s head rather than in the system.

Disaster and emergency preparedness

Disasters and emergencies (fires, storms, pandemics, cyberattacks) can disrupt payroll operations entirely. If you are doing payroll outsourcing, confirm that the provider has a contingency plan for meeting designated payroll duties during disasters. For in-house payroll, maintain off-site backups of all payroll data, document manual fallback procedures, and identify which employees must be paid first in a partial-capability scenario.

Why is accurate payroll management important for businesses?

Accurate payroll management is important because payroll errors create financial penalties, legal exposure, employee turnover, and reputational damage that compound faster than most business risks. Understanding payroll importance from both the employee and regulatory perspectives explains why payroll risk management deserves the same attention as financial controls and cybersecurity.

The most critical point that businesses miss is that even when payroll processing is outsourced, the employer retains ultimate legal responsibility for tax compliance, data security, and employee classification. Regular payroll audits verify that both internal processes and external providers are performing accurately and in compliance with current law.

How does technology reduce payroll risk?

Modern payroll technology reduces risk across every category by automating calculations, enforcing access controls, maintaining audit trails, and updating compliance rules automatically.

Deloitte has found that automating payroll can reduce errors by up to 50% and processing time by 25%. Even conservative estimates show automation reducing errors by 30%. Automated systems calculate taxes based on each employee’s specific location, track legislative changes in real-time, and flag inconsistencies before payments are processed. Integration with time-tracking, HRIS, and accounting systems eliminates the manual data re-entry that creates most process errors.

Despite these capabilities, nearly three-quarters (71%) of employers indicate that their current payroll solution does not meet even basic needs (PrimePay research). Organizations still relying on spreadsheets and manual processes face significantly higher error rates, weaker audit trails, and greater compliance exposure. On-demand pay (earned wage access) is one emerging technology that reduces risk by giving employees access to earned wages before payday, reducing off-cycle payment requests and the manual processing errors they create.

What is the biggest payroll risk?

The biggest payroll risk by personal liability exposure for business owners is the Trust Fund Recovery Penalty, which can assess 100% of unpaid trust fund taxes against individuals with financial authority. At the organizational level, wage-and-hour class actions and data breach exposure (IBM’s 2024 Cost of a Data Breach Report found an average of $4.88M per breach) can exceed TFRP amounts. The most frequent payroll risk is calculation errors, with EY’s 2022 survey finding an average of 15 corrections per pay period among respondents.

How often should you audit payroll?

Review payroll after every cycle for errors, conduct a formal internal audit at least quarterly, and perform a full annual audit before year-end W-2 generation. Companies subject to SOX or undergoing SOC 2 Type II reporting should align payroll audits with their control testing schedules. Companies with high error rates should audit more frequently until root causes are resolved.

Can you outsource payroll risk management?

You can outsource payroll processing, but the employer retains ultimate legal responsibility for tax compliance, data security, and employee classification. A Certified Professional Employer Organization (CPEO) under IRC Section 3511 can assume federal employment tax liability specifically on remuneration paid to worksite employees, but this does not cover state taxes, non-worksite employees, or classification disputes. When choosing a payroll provider, verify SOC 2 Type II certification, confirm their incident response procedures, and understand exactly which liabilities transfer and which remain with you.

What payroll controls are required for SOX compliance?

SOX requires publicly traded companies to maintain internal controls over payroll as a component of financial reporting, including segregation of duties, documented approval workflows, audit trails for all payroll changes, and regular testing of payroll controls by internal or external auditors. Payroll is typically classified as a significant account because it’s one of the largest expenses on the income statement.

What should a payroll risk management checklist include?

A payroll risk management checklist should cover ghost employee validation (compare payroll list against HR directory), tax filing verification (ensure filings match bank withdrawals), access log review (audit who has administrative access), overtime auditing (flag unapproved spikes), classification review (re-evaluate long-term contractors), variance analysis (compare current cycle against budget and prior year), leave accrual review (verify balances match actual time off), and compliance calendar review (confirm all jurisdictional deadlines are tracked). Use this checklist during monthly or quarterly reviews to ensure no gaps have formed in your controls.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations