Payroll deductions: how they work, types & calculation

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll deductions are the amounts an employer withholds from an employee's earnings for taxes, benefits, garnishments, and other obligations, which reduce gross pay to net pay. These withholdings are processed each pay period and remitted to the relevant government agencies, benefit providers, or other designated recipients.

The types of payroll deductions are mandatory and voluntary payroll deductions. Mandatory payroll deductions include FICA (Federal Insurance Contributions Act) taxes, federal income tax, state and local income taxes, and wage garnishments. Voluntary payroll deductions include health insurance, retirement plans, and life or disability insurance.

Payroll deductions are calculated by determining gross pay, subtracting pre-tax deductions, calculating and withholding payroll taxes, applying additional required taxes, determining state and local income tax, subtracting post-tax deductions, and calculating net pay.

What are payroll deductions?

Payroll deductions are amounts taken from an employee's gross pay before the employee receives their net pay. These deductions include mandatory expenses, such as taxes, and optional contributions, like benefits or retirement savings. Employers are responsible for accurately calculating payroll deductions and making sure the withheld amounts are submitted to the relevant agencies or recipients.

Common examples of payroll deductions include federal, state, and local income taxes and benefit premiums, such as medical, dental, vision, or other insurance plans. Other examples are union dues, retirement plans like 401(k), garnishments for child support, alimony, or other legal obligations, and voluntary charitable donations.

How do payroll deductions work?

Payroll deductions work by processing each pay period according to relevant tax laws and withholding information provided by employees or pursuant to a court order. The payroll deduction calculations are performed manually or automatically using a payroll service provider. Many companies choose automation, as it reduces errors and makes sure that payments are filed with the appropriate authorities on time.

The amount of payroll deductions withheld from each employee is determined by the Form W-4 Employee's Withholding Certificate, applicable state and local withholding forms, benefits enrollment, and other relevant details. A standardized process for collecting this information helps employers maintain accuracy and compliance.

What are the types of payroll deductions?

The types of payroll deductions are mandatory and voluntary payroll deductions. Mandatory deductions include FICA (Federal Insurance Contributions Act) taxes, federal income tax, state or local income tax, and wage garnishments. Voluntary deductions are health insurance, retirement plans, and life or disability insurance.

Mandatory payroll deductions

Mandatory payroll deductions are amounts that employers are legally required to withhold from employee wages, regardless of employee choice. Common mandatory deductions include FICA taxes, federal income tax, state and local income tax, and court-ordered wage garnishments when applicable. Employers must withhold the required taxes for individuals classified as employees.

FICA (Federal Insurance Contributions Act) taxes

FICA taxes fund Social Security and Medicare programs. Employees pay Social Security tax at 6.2% up to a set wage limit and Medicare tax at 1.45% with no wage cap. These taxes total 7.65% of an employee's wages, and employers are legally required to match this amount. Some employees are also subject to the Additional Medicare Tax, so employers withhold an extra 0.9% once an employee's earnings exceed $200,000 within a calendar year. Employers are not required to match the Additional Medicare Tax.

Federal income tax

The federal government uses seven progressive income tax brackets, which range from 10% to 37%. An employee's income is taxed in stages, starting at the lowest rate and moving to higher rates as earnings reach each bracket threshold, up to their total taxable income. The income limits for each tax bracket differ based on the employee's filing status, as shown on Form W-4, such as single, married filing separately, married filing jointly, or head of household. Employers use one of two methods to withhold federal income tax each pay period, such as the wage bracket method or the percentage method.

State and local income tax

State and local income tax laws differ across jurisdictions. Some states apply a flat tax rate, others use multiple tax brackets, and a few do not impose state income tax. Certain states also follow federal tax guidelines rather than establishing separate rules. Businesses need to review the requirements of each state where they operate to stay compliant with local tax regulations.

Wage garnishments

Courts, regulatory agencies, and the IRS require employers to withhold a portion of an employee's net (post-tax) wages to cover obligations such as unpaid taxes, child support, alimony, or defaulted loans. Garnishment applies to wages, salaries, commissions, bonuses, pensions, and retirement payments. Employers must also comply with Title III of the CCPA (Consumer Credit Protection Act), which limits the amount of wages garnished each week and prohibits terminating an employee due to garnishment for a single debt.

Key takeaway: Mandatory deductions are non-negotiable - employers must withhold FICA taxes, federal income tax, state and local taxes, and court-ordered garnishments regardless of employee preference. Getting these wrong triggers penalties, not just errors.

Voluntary deductions

Voluntary payroll deductions are amounts employees choose to have withheld from their paychecks to cover benefits or other optional expenses. These deductions are sometimes taken on a pre-tax basis if allowed under tax rules or on a post-tax basis. Employers need to make sure employees fully understand them and provide written consent before withholding premiums or other benefits. Employers also have to show the deduction amount and year-to-date total on each pay statement and keep accurate records, as many states require this for compliance and auditing purposes.

Health insurance

Employees have their share of healthcare premiums deducted on a pre-tax basis if they enroll in the company plan and a Section 125 Premium Only Plan is in place. They also get to contribute pre-tax funds to HSAs (Health Savings Accounts) or FSAs (Flexible Spending Accounts) for medical expenses through a Section 125 plan.

Retirement plans

Two common retirement savings options employers offer are traditional 401(k) plans and Roth 401(k) plans. Contributions to a traditional 401(k) are made on a pre-tax basis for federal and most state income taxes but are still subject to FICA taxes, while contributions to a Roth IRA are made after taxes.

Life insurance and disability plans

Premiums for group life insurance or short- and long-term disability coverage are also withheld from employee pay. Some employers provide basic term life insurance to employees at no cost, usually up to $50,000 in coverage, and amounts above this are considered imputed income. Additional coverage for the employee or dependents is usually deducted from pay on a post-tax basis.

Other voluntary payments

Employers deduct payments for employee-chosen benefits such as charitable donations or wellness programs that state law permits. Unionized employees also have payroll deductions for union dues and any taxable benefits provided through the union. Other deductible job-related expenses include uniforms, meals, and travel, though some states restrict these types of deductions.

What are pre-tax payroll deductions?

Pre-tax payroll deductions are taken from an employee's paycheck before taxes are calculated. Pre-tax deductions reduce the employee's tax liability. Some pre-tax deductions, such as Section 125 cafeteria plan contributions for health insurance and FSAs, also reduce an employer's FUTA (Federal Unemployment Tax Act) and state unemployment insurance contributions. These deductions are excluded from taxable wages. Other pretax deductions, however, like traditional 401(k) contributions, remain subject to FUTA and unemployment taxes.

Common pre-tax deductions include health insurance, group-term life insurance, and retirement plan contributions. Employees mostly benefit from pre-tax contributions, as they save more compared with paying for benefits after taxes, while participation is optional. Pre-tax contributions, however, are subject to limits, as the IRS sets annual caps on the amount employees contribute to a 401(k) plan.

Deduction Type | Tax Treatment | Common Examples |

|---|---|---|

Pre-tax | Reduces taxable income before taxes are calculated | Health insurance, FSA, traditional 401(k) |

Post-tax | Deducted after all taxes are withheld | Roth IRA, disability insurance, union dues, wage garnishments |

What are post-tax payroll deductions?

Post-tax payroll deductions, also known as after-tax deductions, are amounts taken from an employee's paycheck after withholding all required taxes. Post-tax deductions do not reduce taxable income, unlike pre-tax deductions. Employers first apply all pre-tax deductions and tax withholdings when processing payroll, and then apply post-tax deductions to the remaining earnings.

Common post-tax payroll deductions include Roth IRA contributions, disability insurance, union dues, charitable donations, and wage garnishments. Employees are allowed to withdraw their consent to most post-tax deductions, but wage garnishments are mandatory for withholding.

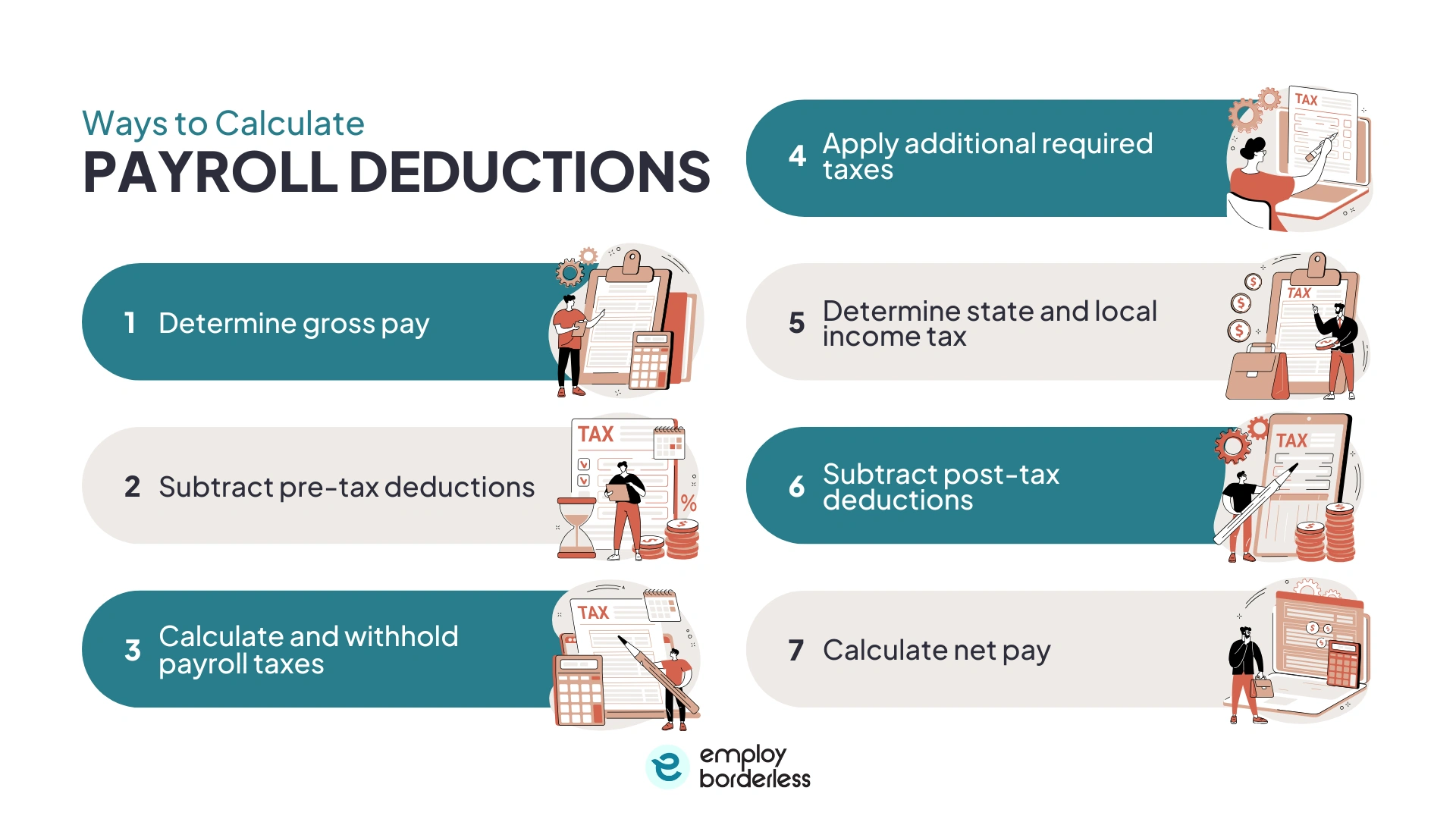

How to calculate payroll deductions?

To calculate payroll deductions, determine gross pay, subtract pre-tax deductions, calculate and withhold payroll taxes, apply additional required taxes, determine state and local income tax, subtract post-tax deductions, and calculate net pay.

The ways to calculate payroll deductions are listed below.

Determine gross pay: Determine the employee's total earnings for the pay period.

Subtract pre-tax deductions: Deduct contributions for health insurance, 401(k) retirement plans, and other voluntary benefits before taxes are applied.

Calculate and withhold payroll taxes: Use the employee's Form W-4 and the current year's IRS tax tables to calculate the correct federal tax.

Apply additional required taxes: Deduct 7.65% of adjusted gross pay (up to the Social Security wage limit), and apply an additional 0.9% Medicare tax if the employee's year-to-date earnings exceed $200,000.

Determine state and local income tax: Calculate any state and local income taxes based on your location's unique requirements and tax rates.

Subtract post-tax deductions: Deduct items such as Roth IRA contributions, wage garnishments, union dues, or other post-tax benefits.

Calculate net pay: The remaining amount after all deductions is the employee's take-home pay.

Key takeaway: Pre-tax deductions must be subtracted before you calculate payroll taxes - applying them in the wrong order means over-withholding federal income tax from every paycheck.

How to choose the right software for automating payroll deductions?

To choose the right software for automating payroll deductions, consider compliance and tax accuracy, automation features, integration with existing systems, customer support, cost and pricing, and growth capacity.

Select payroll software that automatically updates to show the most recent tax laws and regulations to make accurate tax filings and calculations. This up-to-date tax accuracy helps prevent fines and keeps the payroll compliant with federal, state, and local requirements.

Choose a system that automates routine payroll tasks, such as calculations, tax withholdings, and pay runs. Automation reduces manual errors and saves time for HR and finance teams.

Use payroll software that integrates smoothly with HR, accounting, time-tracking, and other business systems to avoid duplicate data entry and improve workflow accuracy.

Select software that helps with payroll setup, solving problems, and updates while making sure teams resolve issues quickly and keep payroll running smoothly.

Evaluate software by considering the total cost, which includes setup, licensing, per-employee fees, and any extra charges for advanced features. Make sure the pricing matches the budget without paying for unnecessary functionality.

Choose software that grows with the business, handles more employees, new locations, and additional payroll complexities without requiring a system change. This avoids future migration issues and supports long-term use.

How are payroll deductions reported?

Payroll deductions are reported to the federal government using specific forms when filing employee tax withholdings and employer tax payments. Common forms include Form 940 (Employer's Annual Federal Unemployment Tax Return), Form 941 (Employer's Quarterly Federal Tax Return), and Form 944 (Employer's Annual Federal Tax Return). These forms are filed on paper or electronically, and employers must follow state-specific rules for payroll reporting.

Are payroll deductions recorded as liabilities?

Yes, payroll deductions are recorded as liabilities on the company's books until they are paid to the appropriate recipients. The funds withheld from employee paychecks belong to tax authorities, benefit providers, or courts, not the employer. Accounting for these amounts as short-term liabilities offers accurate financial reporting and helps protect the business from payroll tax penalties.

When are employees allowed to change voluntary deductions?

Employees are allowed to change voluntary deductions, such as benefit premiums, during the employer's annual open enrollment period. These deductions are mostly managed through a Section 125 plan, which allows employees to set aside pre-tax funds for expenses like childcare or specific medical costs. Life events, such as the birth of a child, marriage, divorce, or loss of other coverage, also permit adjustments outside of open enrollment.

What is the LTD (Long-Term Disability) deduction on paychecks?

The LTD (Long-Term Disability) deduction on paychecks provides coverage for employees who are unable to work due to illness or injury for an extended period. Premiums are lower when deducted on a pre-tax basis, but benefits received are subject to federal income tax. Post-tax LTD deductions slightly reduce take-home pay, but benefits are tax-free.

What are examples of incorrect payroll deductions?

Examples of incorrect payroll deductions are misapplying garnishments, over-withholding taxes due to outdated W-4 forms, and failing to adjust for pre-tax benefits like 401(k) contributions.

What is the average payroll deduction?

The average payroll deduction includes federal and state income tax and Social Security (6.2%) and Medicare (1.45%). Common mandatory and voluntary deductions usually reduce gross pay by about 25% to 30% for many workers, though actual amounts differ widely by income level, location, and benefits selected.

How to stop a payroll deduction?

To stop a payroll deduction, employees need to contact the relevant companies or their personnel and payroll offices. Employees need to make sure changes are properly shown in payroll tax withholding.

Why did I receive a deduction from my paycheck?

You received a deduction from your paycheck because your employer withheld amounts for required taxes, benefits, retirement contributions, or other authorized expenses. Deductions are sometimes mandatory, like federal and state taxes, or voluntary, such as insurance premiums or retirement savings.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations