Blockchain in payroll: applications, benefits & challenges

Robbin Schuchmann

Co-founder, Employ Borderless

Blockchain is a decentralized digital ledger that records transactions in blocks by securing each block through a cryptographic hash. These blocks are chronologically linked and form an immutable chain.

Blockchain in payroll refers to using this ledger to manage payroll processes. Employee records, work hours, wages, and tax details are stored as encrypted transactions on-chain. Each entry is time-stamped and verified across the network which helps in secure and tamper-proof payroll data.

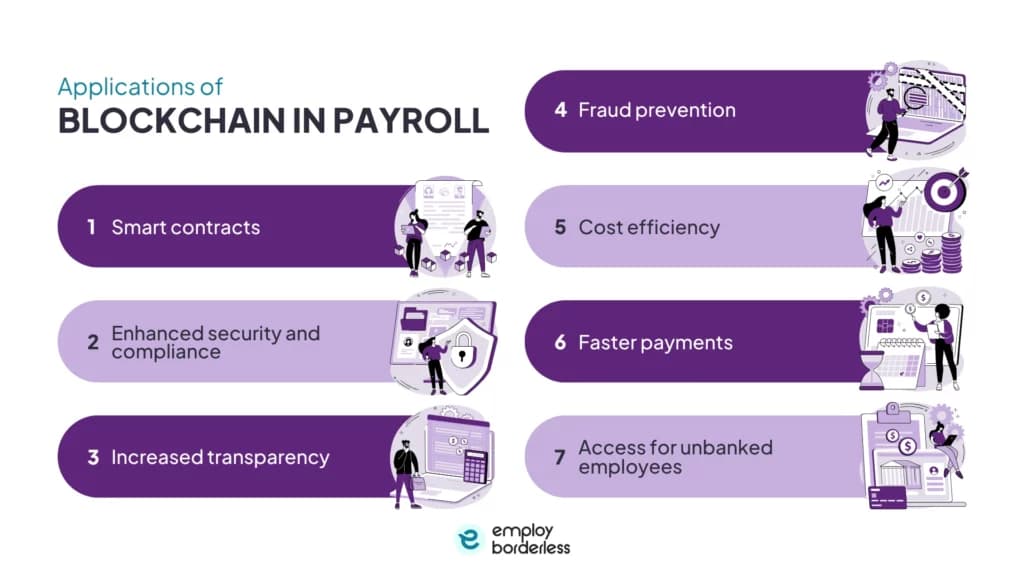

Blockchain has different applications in payroll, such as smart contracts for automation, enhanced security and compliance, increased transparency, fraud prevention, cost efficiency, faster payments, and access for unbanked employees.

Using blockchain-based payroll solutions offers significant benefits, such as reduced payroll errors, real-time access to payment records, simplified audit processes, improved employee trust and satisfaction, and regulatory compliance. Despite these benefits, businesses face challenges by using such payroll solutions, including regulatory uncertainty, integration with legacy systems, capacity issues, security concerns, technological adoption, and volatility exposure.

What is blockchain?

Blockchain in payroll is a decentralized and distributed ledger technology that securely records and stores payroll transactions. Data is grouped into blocks, and each block is linked to the previous one using cryptographic hashes, to form a continuous chain. Once data is recorded, it cannot be altered without changing all next blocks, which is difficult due to the network's consensus protocols. Blockchain operates across a peer-to-peer network, which means no single entity controls the system.

Blockchain replaces traditional and centralized payroll databases by distributing identical copies of payroll records across a network of computers, which makes sure that all participants have access to the same and up-to-date information.

This technology groups each payroll transaction, such as salary payments, tax withholdings, and benefits disbursements, into a block, and links it to previous blocks cryptographically. It also validates those transactions through consensus mechanisms before being added to the chain permanently.

What are the applications of Blockchain in payroll?

The applications of blockchain in payroll are smart contracts for automation, enhanced security and compliance, increased transparency, fraud prevention, cost efficiency, faster payments, and access for unbanked employees.

Smart contracts

Smart contracts are self-executing agreements that automate payroll processing based on predefined conditions, such as work hours or project milestones.

Blockchain helps businesses use smart contracts to process timely salary payments, remove errors, and reduce administrative burdens. Smart contracts also help multinational companies perform global payroll processes without any transaction fees and delays. Employers can pay directly to their employees without being dependent on intermediaries like banks and clearing houses.

This automation reduces administrative overhead, minimizes errors, and keeps payments on time. For example, a smart contract can be programmed to make payment to an employee's account immediately after they complete a set number of work hours.

An example of businesses using smart contracts is that they pay freelancers or contract employees for a set amount of work or hours. The smart contract itself processes their payroll without the intervention of payroll teams. It decreases trust issues between both parties involved.

Enhanced security and compliance

Enhanced security and compliance means using blockchain in payroll to improve its security and meet changing payroll regulations.

Payroll data contains sensitive information, such as bank details, Social Security numbers, and salary information. Blockchain uses cryptographic techniques like hashing and encryption to protect this data. This structure enhances data integrity and security, making unauthorized alterations virtually impossible.

Businesses are required to adopt strict data protection measures to comply with regulations like the GDPR (General Data Protection Regulation) and the CCPA (California Consumer Privacy Act). Blockchain is transparent and tamper-proof so it provides a verifiable trail of all payroll transactions, supports audits, and keeps companies compliant.

Organizations verify employees' credential details and work history by using blockchain as a secure database for employee records, storing credentials, certifications, and work history in an immutable format. Organizations can verify employees' qualifications quickly with blockchain technology in payroll without relying on third-party services.

Increased transparency

Increased transparency means that all payroll transactions are recorded on a decentralized, immutable ledger, which is visible and traceable to authorized parties in real-time. Each transaction, such as salary payments, tax deductions, or bonuses, is encrypted and time-stamped, which creates a permanent record that is virtually tamper-proof.

This allows employees to track their earnings from employer to account, reduces the potential for disputes, and increases trust between employers and employees.

The transparent record also simplifies audits, supports compliance with regulations, and provides an ultimate source of truth in case of discrepancies or fraud.

Blockchain also simplifies the audit process, as auditors can quickly access a complete and chronological record of all payroll activities without relying on different data sources or manual reconciliation. Traditional payroll requires lengthy processes to audit and verify transactions, but blockchain records all transactions instantly which can be accessible all the time. This auditing process also supports compliance with regulations as regulators can access transparent records without delays.

Fraud prevention

Fraud prevention means using blockchain technology in payroll to secure data from frauds or data breaches by using advanced security measures, like encryption and immutability.

Companies use blockchain technology in payroll because it makes payroll records immutable and decentralizes data management. Blockchain reduces the risk of tampering with the records by internal employees or cybercriminals. Each payroll transaction is securely time-stamped and linked to the previous one, making unauthorized changes easily detectable. It also helps employees and employers to verify transactions in real time by creating a secure and reliable central system.

Blockchain works on a decentralized ledger and data is distributed across multiple nodes, not in a single location. So it is difficult for fraudsters to make changes in the payroll system as there is no chance of a single point of failure.

The use of blockchain in payroll also simplifies the process of audit by logging every transaction in real time. This helps auditors quickly track and verify records, identify discrepancies, and detect fraudulent activities without delays.

Cost efficiency

Blockchain technology in payroll helps companies reduce transaction fees and administrative costs of payroll management by eliminating the need to depend on intermediaries like banks and payroll processors. Payments can be processed instantly and securely with the help of blockchain, which reduces delays and service charges associated with traditional banking systems.

Blockchain technology allows professionals to pay their global workforce with alternative forms of payment, such as currencies like Bitcoin. This helps them make their cross-border transactions easy and avoid foreign exchange fees and processing delays.

Crypto payroll systems also expand access to unbanked or underbanked employees. Individuals in regions with limited or unreliable banking access can receive payments directly and securely. Blockchain supports direct, peer-to-peer transactions, which allow payroll teams to not rely on middlemen entirely.

Faster payments

Faster payments mean the ability to process salary transactions instantly, as blockchain eliminates intermediaries like banks and payment processors.

Traditional payroll systems take several days to process payments, especially for cross-border transactions. Blockchain-based payroll allows transactions to be completed within minutes, even across international boundaries. This approach bypasses delays from banking hours, holidays, or currency conversions.

Smart contracts further automate and speed up the process by triggering payments immediately when predefined conditions, such as hours worked, are met. Employees receive their wages quickly, which increases overall satisfaction.

Access for unbanked employees

Access for unbanked employees means the ability of individuals who do not have traditional bank accounts to receive their wages and manage their income through alternative financial technologies, such as blockchain-based payroll systems.

Blockchain technology helps unbanked employees access their wages by allowing employers to make salary payments directly into digital wallets by using cryptocurrencies or stablecoins. Blockchain does not require a central authority or physical access points, so it is ideal for reaching employees in remote or underserved regions. For example, workers in areas with limited or no banking access can still receive payments instantly and securely through blockchain networks.

Blockchain also empowers unbanked employees by giving them full control over their finances. They can store, transfer, and convert their earnings into local currencies as needed through mobile-accessible digital wallets. This financial autonomy not only improves day-to-day money management but also allows them to save money and make investments.

What are the benefits of blockchain in payroll?

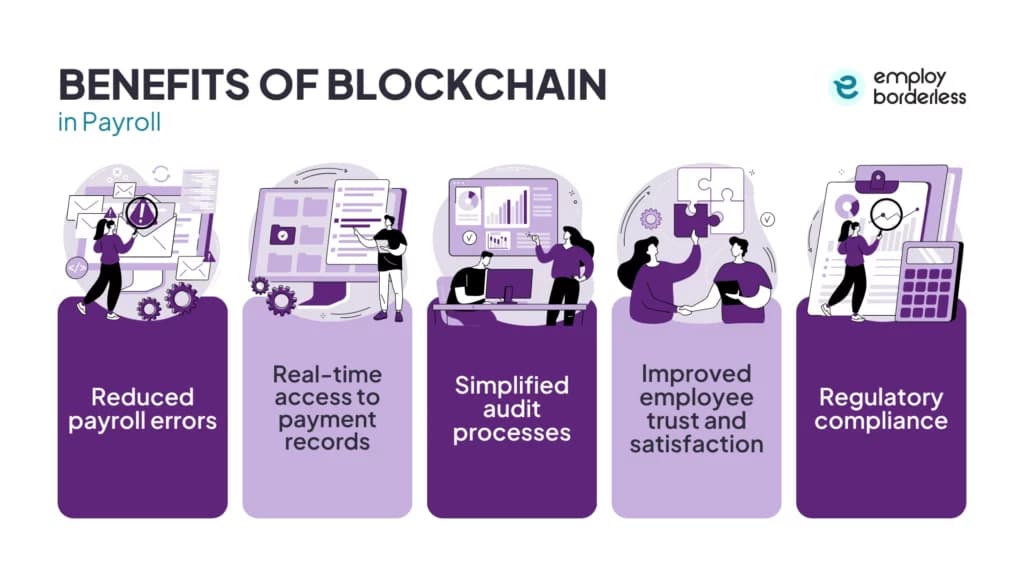

The benefits of blockchain in payroll are reduced payroll errors, real-time access to payment records, simplified audit processes, improved employee trust and satisfaction, and regulatory compliance.

The benefits of blockchain in payroll are listed below.

- Reduced payroll errors: The immutable ledger of blockchain automates the recording and calculations of payroll transactions. Companies do not need to manually input the data so there is no risk of unauthorized changes. This helps them reduce payroll discrepancies and mistakes.

- Real-time access to payment records: Blockchain-based payroll allows employees and employers to view payroll transactions instantly. This helps them access up-to-date and tamper-proof payment information at any time. It increases transparency and empowers employees to verify their earnings.

- Simplified audit processes: Blockchain technology in payroll records all payroll transactions permanently and allows audit teams to easily access them for review. Auditors can quickly trace and validate payments without relying on fragmented data, which helps organizations stay compliant with payroll regulations and also reduces the time and cost of audits.

- Improved employee trust and satisfaction: Companies use blockchain in payroll to process their payroll quickly and with transparency to build confidence among employees. Workers can track their payments and resolve disputes with clear and verifiable records, which helps companies develop a sense of fairness in employees and boost their overall morale.

- Regulatory compliance: Using blockchain technology in payroll supports regulatory compliance by improving transparency, security, and efficiency of the payroll process. The shared architecture and security of blockchain eliminate the need for payroll teams to manually check the payroll data and also make the regulatory process easy for both parties involved.

What are the challenges of blockchain in payroll?

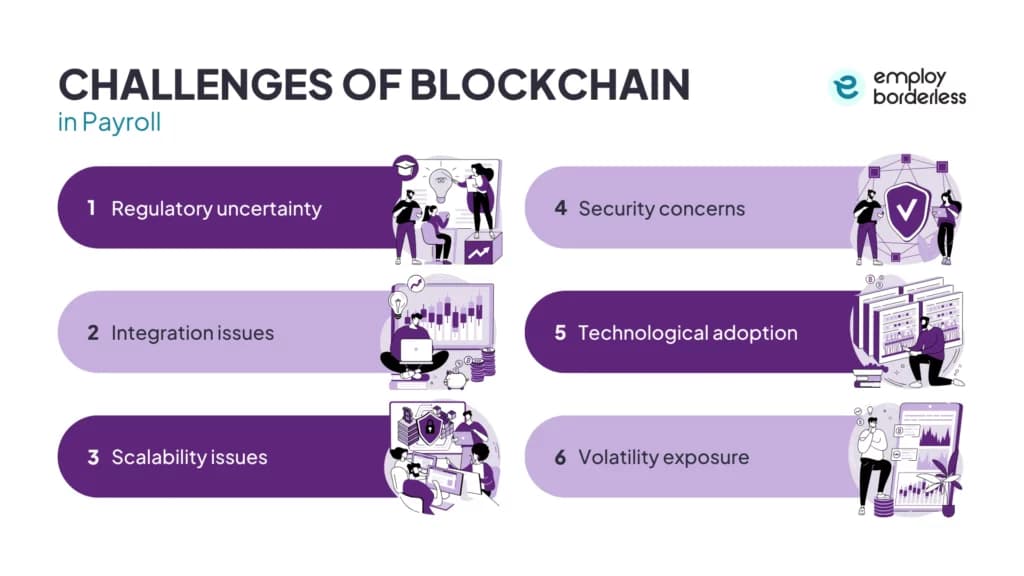

The challenges of blockchain in payroll are regulatory uncertainty, integration with legacy systems, scalability issues, security concerns, technological adoption, and volatility exposure.

The challenges of blockchain in payroll are listed below.

- Regulatory uncertainty: Blockchain payroll faces complex and changing regulations across different countries, including ambiguity in tax treatment, labor laws, and compliance requirements. Organizations must constantly monitor regulatory developments and need legal counsel to avoid fines or legal issues.

- Integration issues: Most organizations still use legacy payroll and HR systems that are not designed to work with blockchain technology. Companies have to overcome challenges to integrate blockchain, such as data compatibility, system interoperability, and migration of historical payroll data. So they have to make significant investments in middleware, training, and careful change management.

- Scalability issues: Businesses that use public blockchains, like Bitcoin and Ethereum, face issues as their usage grows because these blockchains have limited transaction throughput. This leads to slow processing times, high transaction fees, and challenges in handling large-scale payroll operations.

- Security concerns: Blockchain-based payroll solutions are usually secure, but sometimes they are vulnerable to risks as well, such as risks from poorly coded smart contracts or compromised private keys. The digital wallets of companies can be targeted by hackers and payroll data can be exposed if security protocols are not strictly implemented.

- Technological adoption: Organizations face challenges in using blockchain as it requires specialized skills for development, integration, and maintenance. Companies usually do not have such professionals so they have to invest in upskilling the existing staff or hire new talent.

- Volatility exposure: Cryptocurrencies used in blockchain payroll are highly volatile, so employees receive fewer amounts than their agreed-upon wage if the cryptocurrency value drops before conversion to fiat. The value of digital currencies can fluctuate rapidly, which creates uncertainty around wage value and employee satisfaction.

How does payroll work?

A payroll system works by helping businesses pay their employees on time and accurately by following tax laws. First, companies set up the system to match the company's specific needs by adding employee details, pay schedules, and tax rules. Then they move old payroll data into the new system to keep records accurate.

Employees are trained to use the system, and tests are done to make sure everything works properly. Once running, the system collects employee work details, calculates gross pay, deducts taxes and benefits, and determines net pay. After checking, payments are sent through direct deposits or checks. Finally, payroll records are updated, and reports are made for tracking and compliance.

What steps help improve payroll accuracy?

The steps to improve payroll accuracy are automating payroll processes, conducting regular payroll audits, maintaining accurate payroll records, and implementing advanced time-tracking systems. Payroll accuracy can also be improved by providing ongoing training to payroll staff, staying updated with payroll legislation, and using a unified payroll system.

What are payroll compliance frameworks?

The payroll compliance frameworks are employee classification, wage and hour compliance, tax withholding and reporting, and record-keeping practices. Payroll compliance frameworks also include benefits administration, direct deposit regulations, and compliance with tax regulations.

How do I choose a payroll provider?

To choose a payroll provider, you have to understand payroll needs, compliance and tax filing capabilities, technology integration and ease of use, security and data protection, customer support and SLAs (Service Level Agreements), pricing transparency, experience and reputation, growth capacity, and availability of employee self-service portals.

What are the types of payroll systems?

The types of payroll systems are manual payroll systems, payroll software systems, online payroll services, payroll card systems, and outsourced payroll systems. These systems help businesses manage employee salaries, taxes, and deductions properly while reducing errors and saving time.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations