Payroll fraud: definition, types, key indicators, and how to prevent it

Robbin Schuchmann

Co-founder, Employ Borderless

Payroll fraud is the deliberate manipulation of a payroll system to obtain unauthorized payments, committed by employees, managers, or external attackers. The ACFE's Occupational Fraud 2024 report puts the global median occupational fraud loss at $145,000, with a median duration of 12 months before detection. In the United States and Canada, payroll fraud schemes make up 15% of all occupational fraud cases, with a median duration of 18 months and median losses of $2,800 per month. Payroll schemes account for approximately 9% to 10% of reported occupational fraud cases globally.

- Global median fraud loss: $145,000 per case, with a 12-month median before detection (ACFE 2024).

- US and Canada payroll fraud share: 15% of all occupational fraud cases, $2,800 median monthly loss.

- Who commits it: Managers account for 39% of cases (median loss ~$184,000); owners/executives 19% (median loss $500,000+).

- BEC losses: The FBI's IC3 reported $2.77 billion in business email compromise losses across 21,442 complaints in 2024.

- Detection impact: Surprise audits reduce median fraud loss by 51% and fraud duration by 50% (ACFE 2024).

Smaller companies (under 100 employees) are disproportionately affected because they typically lack segregation of duties, formal audit processes, and dedicated payroll controls.

Three factors drive payroll fraud. Motivation (a financial pressure like unexpected debt, resentment over a missed promotion, or simple greed), opportunity (weak controls, lack of oversight, single-person payroll processing), and rationalization (the perpetrator convinces themselves the fraud is justified). Understanding this fraud triangle helps explain why even trusted, long-term employees commit payroll fraud and why controls must be structural, not based on trust alone.

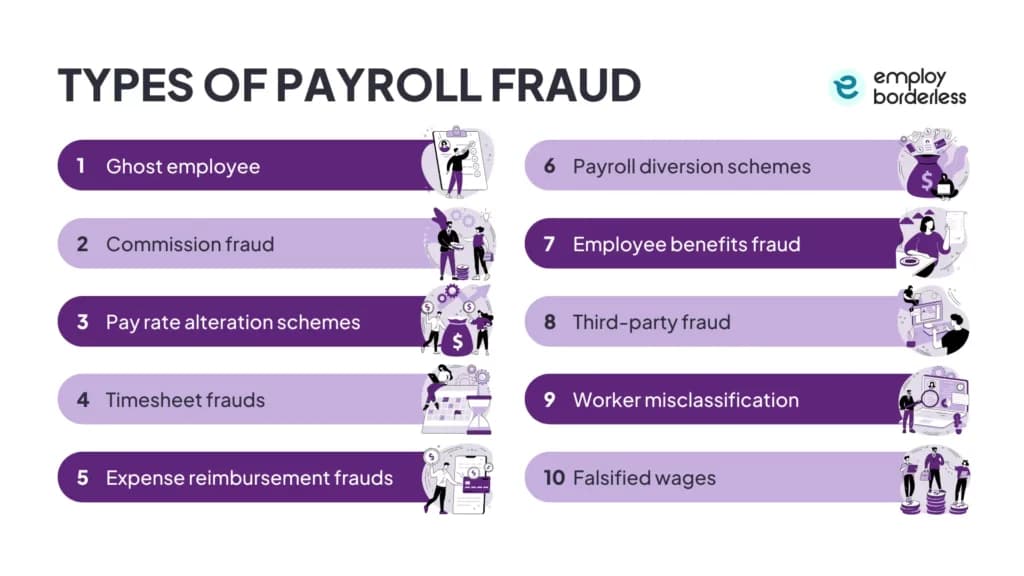

What are the types of payroll fraud?

Payroll fraud takes ten primary forms, each with a distinct mechanism, typical perpetrator, and detection method.

Fraud Type | How It Works | How to Detect It |

Ghost employees | A payroll insider adds a fictional, deceased, or terminated employee to the system and routes payments to an account they control. A Wendy's manager in Pennsylvania created a ghost employee named "William Bright" who "worked" 128 shifts over 22 pay periods, earning $19,898 deposited to the manager's Cash App. | Cross-reference payroll roster against HR headcount. Check for duplicate bank accounts, addresses, or SSNs. For remote workforces, require manager attestation of team roster against payroll each period. |

Timesheet fraud | Employees overstate hours worked, falsify overtime, or have coworkers clock them in (buddy punching). A Boston police captain had his unit's officers each claim 4 hours of overtime when they worked only 2, splitting shifts so each officer was paid for double the hours actually worked. The scheme generated over $120,000 in fraudulent overtime over 3.5 years. A USPS postal worker falsified court paperwork to claim jury duty he didn't serve, collecting nearly $40,000 in unearned wages between 2003 and 2006. | Compare timesheets against badge/access logs and supervisor schedules. Flag employees with consistently high overtime in low-volume periods. Run exception reports on unusual shift lengths. |

Pay rate alteration | An employee or payroll insider changes a pay rate in the system without authorization, collects one or more paychecks at the inflated rate, then may revert it after the pay run to avoid detection. | Audit trail on all pay rate changes. Require dual approval for any rate modification. Flag any rate change and reversal within the same pay period. |

Payroll diversion (external attacks) | External attackers redirect employee paychecks through phishing emails (BEC), credential harvesting via cloned websites, or account takeover. In late 2022 and early 2023, cybercriminals targeted USPS employees with a cloned payroll website, harvesting login credentials and rerouting paychecks totaling approximately $1 million across at least 460 affected workers. | Require out-of-band verification (phone call to the employee's HR-system-of-record number, not a number from the request) for all direct deposit changes. Apply MFA on all payroll portals. Monitor for login activity outside business hours. |

Expense reimbursement fraud | Employees submit fabricated or inflated expense claims through accounts payable or payroll. A former payroll manager at a New Orleans law firm embezzled more than $2.5 million over six years by embedding unauthorized "non-taxable reimbursements" into the ADP payroll system, effectively using the payroll platform as the vehicle for the theft. | Require original receipts with vendor name, date, and itemization. Flag duplicate submissions, same-vendor patterns, and year-over-year expense anomalies. Set approval thresholds. Separate expense approval from payroll processing. |

Worker misclassification | Employers classify full-time workers as 1099 independent contractors to avoid FICA, FUTA, benefits, and workers' comp obligations. In June 2024, the DC Attorney General sued general contractor Whiting-Turner and its subcontractor Welch Mechanical Contractors, along with three labor brokers, for misclassifying over 370 workers as independent contractors to avoid minimum wage, overtime, and sick leave obligations. Welch and the labor brokers performed the misclassification; Whiting-Turner was named as benefiting from the scheme as the general contractor. | Compare 1099 worker hours and supervision patterns to W-2 norms. Check whether contractors use company equipment, follow set schedules, or have tenures exceeding 12 months. |

Workers' comp fraud | Employee fakes or exaggerates an injury, or claims a non-work injury occurred on the job. Common in construction and mining industries. | Investigate all claims with witness statements, medical documentation, and security camera footage. Monitor for inconsistencies between claimed injury and observed activity. |

Commission/bonus fraud | An employee falsifies sales records, inflates performance metrics, or fabricates completed milestones to claim commissions or bonuses they didn't earn. This fraud is common in sales-heavy organizations where commission structures are complex and verification of individual deal contributions is difficult. | Verify all commission and bonus claims against source data (CRM records, POS data, client confirmations) before payout. Run exception reports on unusually high commission percentages or sudden spikes in claimed sales. |

Advance payment fraud | An employee obtains a salary advance but never repays it, or someone with payroll access records the advance as a different expense to hide the unrepaid amount. | Track all advances in a separate ledger with automatic deduction from the next paycheck. Require written authorization for all advances and reconcile monthly. |

Embezzling withholdings | The employer or payroll administrator pockets legitimate withholdings from wages (income tax, 401(k) contributions, insurance premiums) instead of remitting them. A Michigan insurance agency operator stole payroll deductions earmarked for employee SIMPLE IRA contributions and never made the required employer matching payments. | Separate the roles of entering deductions and remitting contributions. Employees should verify their benefit statements directly with providers. The IRS will notify employers when tax deposits don't match filed returns. |

What are the red flags of payroll fraud?

The warning signs of payroll fraud are often behavioral, not just financial. A payroll employee who never takes a vacation, resists sharing duties, or becomes defensive about audit requests is exhibiting classic concealment behavior. ACFE 2024 data show that surprise audits reduced the median fraud loss by 51% and the fraud duration by 50%, making unannounced payroll reviews one of the most effective detection tools.

Financial red flags: Employees with identical bank account numbers or addresses. Unexplained changes to direct deposit information (especially multiple changes in a short period). Pay rate changes without corresponding HR authorization. Consistent overtime logged by the same employees during slow business periods. Payroll totals that exceed budgeted amounts without explanation. W-2 counts that don't match the active employee roster. Leave accrual balances that don't decrease despite known time off. Budget reports showing benefit expenditures higher than expected.

External threat red flags: Emails requesting direct deposit changes from slightly misspelled domains or unfamiliar addresses. Urgency language ("please process today"). Requests that bypass normal approval channels. Preview emails for payrolls you didn't submit. Unexpected payroll transmissions. Employees reporting excessive or unexpected funds in their bank accounts. The FBI's IC3 reported $2.77 billion in BEC losses across 21,442 complaints in 2024. Payroll diversion is among the more common BEC subcategories because it requires no malware, only social engineering.

Behavioral red flags: A payroll administrator who insists on handling all payroll tasks alone and resists cross-training. An employee who never takes vacation (because the fraud requires continuous concealment). Unauthorized access to payroll records by individuals who have no valid business reason. Staff who become unusually defensive when asked routine questions about payroll processes. These behavioral indicators are often the earliest warning signs, appearing before financial anomalies become visible.

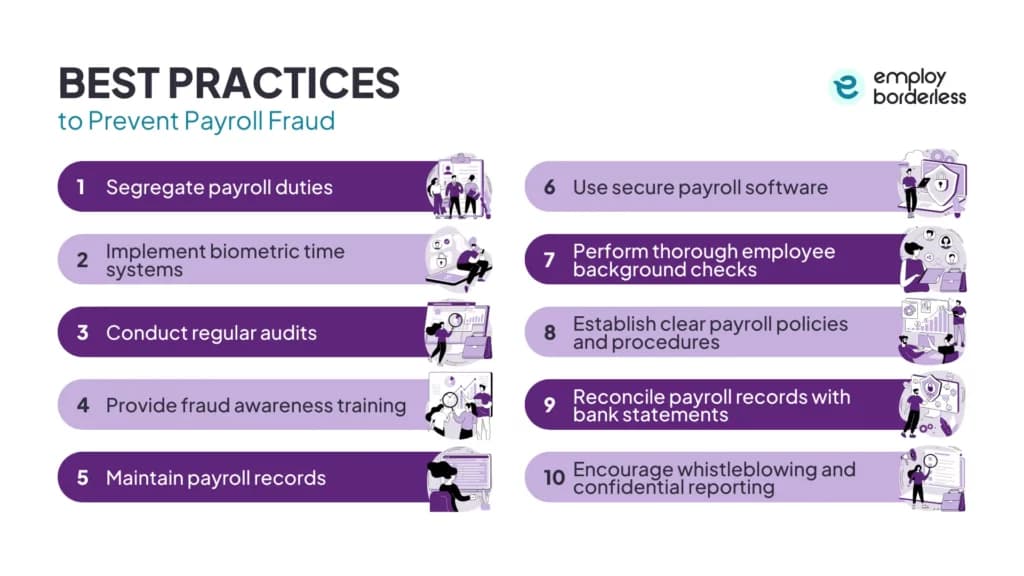

How do you prevent payroll fraud?

Payroll fraud prevention requires layered controls across multiple dimensions. Segregation of duties (no single person controls the entire payroll process), payroll systems access controls (role-based access with audit logging), regular audits (both scheduled and surprise), and a written anti-fraud policy with clear consequences.

Segregation of duties

Segregation of duties is the single most effective control. The person who enters payroll data should not approve it. The person who approves payroll should not distribute payments. The person who reconciles the payroll bank account should not be involved in processing. In small businesses where one person handles all payroll, implement a compensating control: have the owner or a separate manager review every payroll run before processing, comparing the register against the prior period for any changes.

Mandatory vacation for payroll staff

Mandatory vacation works because many payroll fraud schemes require continuous concealment. The perpetrator must intercept notices, alter reports, or re-enter adjustments to hide the fraud from routine monitoring. When forced to leave for at least one uninterrupted week per year (during which someone else processes payroll), the concealment activities break and anomalies surface. If irregularities appear only when the regular payroll person is absent, that's a significant red flag.

Direct deposit change verification

Direct deposit change verification should require out-of-band confirmation for every request. This means calling the employee at the phone number already on file in the HR system of record, not a number provided in the change request itself (which an attacker can insert). Never process a direct deposit change based solely on an email, even if it appears to come from the employee or an executive. This single control eliminates the most common BEC-based payroll diversion attacks.

Biometric time-tracking

Biometric time-tracking (fingerprint or facial recognition) eliminates buddy punching but creates obligations for biometric privacy under state biometric privacy laws. Illinois' Biometric Information Privacy Act (BIPA), Texas' CUBI (Capture or Use of Biometric Identifier Act), Washington's biometric identifier law, and newer provisions in New York City (Biometric Identifier Information Law for commercial establishments), Colorado (Colorado Privacy Act biometric amendments, effective July 2025), and state privacy laws in Oregon and Maryland that treat biometric data as sensitive all regulate biometric data collection. The Illinois Supreme Court's Cothron decision (2023) affirmed per-scan violations, and BNSF Railway faced a $228 million jury verdict under BIPA in 2022, though that verdict was later vacated by the court and the case settled for $75 million in 2024. Before deploying biometric timekeeping, verify your state's biometric privacy requirements and obtain written consent from employees.

Written anti-fraud policy

Establish a clearly defined, written anti-fraud policy that is easily accessible to all staff. The policy should outline the consequences of committing payroll fraud (both internal disciplinary action and legal consequences), the process for reporting suspected fraud (including anonymous reporting channels), and the specific controls in place. Train all employees, especially those who process payroll, on the policy. Staff who understand the monitoring controls and consequences are less likely to attempt fraud.

Background checks and access controls

Conduct background checks on all employees who will handle payroll data or have access to the payroll system. All users should have individual login credentials (never shared access), with every sign-in and event tracked and logged. Apply role-based authorization so employees can only access the specific functions they need. Change passwords to payroll-related systems whenever there is a change in payroll administration personnel. Consider performing payroll and banking tasks on a separate, dedicated computer used only for those purposes.

Regular audits and monitoring

Conduct both scheduled and surprise audits. ACFE data shows surprise audits reduce median fraud loss by 51% and fraud duration by 50%. During audits, review employee addresses and bank account numbers for duplicates. Review leave accrual balances for reasonableness (have employees taken leave? do reports reflect it?). Compare budget reports against actual benefit expenditures. Run exception reports that flag unusual shift lengths, excess overtime, or pay rate changes without HR tickets. Monitor overtime payments for proper approval and reasonableness. Review the vendor database for payroll vendors to confirm expenditures are legitimate.

What are payroll fraud risks?

Payroll fraud risks are the vulnerabilities in your payroll process that allow fraud to occur and the financial, legal, and operational consequences when it does. The core risks are weak segregation of duties (one person controls the full payroll cycle), inadequate access controls, manual data entry points with no audit trail, and overreliance on trust rather than structured oversight. Smaller organizations face higher risk because they typically lack the controls that larger companies have. When fraud does occur, losses run a median of $145,000 globally (ACFE 2024), and schemes run an average of 12 to 18 months before detection - compounding the damage significantly.

What is payroll leakage?

Payroll leakage is the loss of money through payroll errors, overpayments, or fraud that go undetected because no one is reconciling outputs against what should have been paid. It differs from deliberate fraud in that some leakage is unintentional - duplicate payments, uncorrected pay rate errors, unreturned advances - but the financial impact is the same. Ghost employees, unrepaid salary advances, embezzled withholdings, and undetected timesheet fraud are all forms of payroll leakage. Regular reconciliation of payroll registers against HR headcount and budget is the primary control.

What should you do if you discover payroll fraud?

If you discover or suspect payroll fraud, preserve the evidence immediately before confronting anyone. Export payroll records, audit logs, bank statements, and any communications related to the suspected fraud. Do not alter any records or tip off the suspected perpetrator.

Engage a CFE or forensic accountant

Engage a Certified Fraud Examiner (CFE) or forensic accountant to conduct a formal investigation. CFEs gather evidence that meets legal standards, interview witnesses, calculate losses, and prepare reports for law enforcement or litigation. Break the investigation into four phases: planning, information gathering, analyzing evidence, and reporting.

Report the fraud

Report the fraud through the appropriate channels. For any BEC-related fraud (payroll diversion, phishing), file immediately with IC3.gov. The IC3 Recovery Asset Team can coordinate financial institution freezes within 24 to 48 hours of the report if funds haven't cleared, with a reported success rate of approximately 66% for BEC-related freezes. For internal theft cases, contact local law enforcement and your local FBI field office for significant losses. For tax-related fraud, file IRS Form 3949-A (Information Referral). If the fraud involved payroll tax deposits that were collected from employees but not remitted, self-reporting to the IRS can reduce the risk of criminal prosecution under IRC § 7202 (willful failure to collect/pay tax), though the Trust Fund Recovery Penalty under IRC Section 6672 equals 100% of the unpaid trust fund taxes by statutory formula and isn't reduced for voluntary disclosure.

Where does fraud enter the payroll process?

Understanding payroll fundamentals is an essential context for recognizing where fraud enters the system. Payroll fraud exploits specific steps in the payroll process. Ghost employees exploit the employee-setup step. Timesheet fraud exploits the hours-collection step. Pay rate alteration exploits the compensation-configuration step. Payroll diversion exploits the payment-distribution step. Embezzling withholding exploits the tax-remittance step. Each fraud type maps to a specific process vulnerability, which is why payroll importance extends beyond getting employees paid correctly and into organizational risk management.

How does payroll software help prevent fraud?

Automated payroll systems reduce fraud risk through role-based access controls, audit trails, and integration with time-tracking and HRIS that eliminate manual data entry points where fraud typically occurs. Cloud-based payroll platforms add automatic software updates, centralized data, and provider-managed security.

Many payroll platforms include duplicate bank account detection and audit logging as standard features. More advanced anomaly detection (flagging pay rate changes without HR tickets, payroll runs exceeding budget thresholds) typically requires enterprise-tier platforms or integration with separate fraud monitoring tools. For small businesses, the most effective software-based control is a simple audit trail that records every change to employee records, pay rates, and direct deposit information with timestamps and user IDs.

The ACFE's 2024 Anti-Fraud Technology Benchmarking Report found that the use of AI and machine learning for fraud detection is expected to nearly triple over the next two years, with 83% of organizations planning to use AI solutions. AI-powered payroll platforms can scan hundreds of records in seconds, flag behavioral patterns that look anomalous, and identify fraud earlier than manual audits. Even with these advances, human oversight remains essential. Technology offers solutions, but technology also offers new tools for perpetrating fraud.

How common is payroll fraud?

Payroll fraud is a subcategory of asset misappropriation and historically accounts for approximately 9% to 10% of reported occupational fraud cases globally, and 15% in the United States and Canada per ACFE data. The ACFE's 2024 global data shows a median occupational fraud loss of $145,000 and a median duration of 12 months. In the US and Canada specifically, payroll fraud schemes average 18 months before detection with median losses of approximately $2,800 per month. A 2018 Hiscox Embezzlement Study found that 39% of respondents who experienced embezzlement saw more than one case, suggesting that overconfidence in existing controls is itself a risk factor. No industry is immune, but the ACFE's 2024 data shows the highest case counts in banking and financial services, manufacturing, and government/public administration. Construction ranks among the industries with the highest median losses per case.

Who typically commits payroll fraud?

ACFE 2024 data shows that employee-level perpetrators account for approximately 37% of fraud cases (median loss ~$60,000), managers account for 39% (median loss ~$184,000), and owners/executives account for 19% (median loss $500,000+). Higher-ranking perpetrators cause larger losses because they can override controls. External BEC attackers are a growing category that doesn't require any system access. For a deeper look at operational vulnerabilities, see our guide to payroll challenges.

What are the legal consequences of payroll fraud?

Payroll fraud can result in criminal charges (wire fraud, tax evasion), civil liability, and IRS penalties. Wire fraud under 18 U.S.C. § 1343 carries a maximum sentence of 20 years per count, or 30 years if the fraud affects a financial institution. Willful failure to collect or pay tax under IRC § 7202 carries up to 5 years imprisonment and fines up to $250,000 for individuals or $500,000 for corporations under 18 USC §3571. For worker misclassification, IRC Section 3509 provides reduced-rate relief (1.5% of wages for income tax plus 20% of employee FICA if 1099s were filed) rather than full back-tax liability, but only when misclassification was not willful. Willful misclassification is prosecuted under IRC § 7201 (tax evasion) or § 7202, not Section 3509. Under the FLSA, employees have a statute of limitations of two years for non-willful wage violations and three years for willful violations to recover back pay.

Can outsourcing payroll reduce fraud risk?

Yes, outsourcing payroll creates separation between the people authorizing payments and those processing them, which is the core principle of segregation of duties. The provider's system enforces access controls and audit trails that a small business might not build on its own. However, outsourcing doesn't eliminate fraud risk entirely. You still need to audit the provider's output, verify employee rosters, and maintain direct deposit change verification procedures. For guidance on reducing payroll errors alongside fraud, see our guide to improving payroll accuracy.

Which industries are most affected by payroll fraud?

The ACFE's 2024 data shows the highest case counts in banking and financial services, manufacturing, and government/public administration. Construction ranks among the industries with the highest median losses per fraud case ($250,000), driven by high workforce turnover, prevalence of subcontracting, cash-based payments, and the complexity of prevailing wage requirements. Government entities face risk from large employee populations and rigid bureaucratic processes that can mask fraud. However, no industry is immune. Healthcare, education, retail, and hospitality all report significant payroll fraud cases.

How can AI help detect payroll fraud?

AI and machine learning can analyze payroll data patterns far faster than manual audits, flagging anomalies like unusual overtime spikes, duplicate bank accounts, or pay rate changes without corresponding HR tickets. The ACFE's 2024 Anti-Fraud Technology Benchmarking Report projects that AI use in fraud detection will nearly triple in the next two years. AI doesn't replace human judgment, but it dramatically shortens detection time, which is critical since the average fraud scheme runs 12 to 18 months before discovery.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations