What Is A Payroll Policy? Definition, Components, and How to Write One

Robbin Schuchmann

Co-founder, Employ Borderless

A payroll policy is the foundational document that governs how a business calculates, processes, and distributes employee compensation. A business without one operates on assumptions. Pay disputes go unresolved because there is no written standard to refer to. Tax deadlines get missed because no one owns the filing responsibility. Employees ask the same questions about deductions and overtime at every pay cycle because nobody documented the answers the first time.

This guide covers the definition of a payroll policy, the 18 components a complete policy includes, and the steps to write one from scratch. It also explains when payroll policy management becomes complex enough to warrant outside support.

What is a payroll policy?

A payroll policy is a documented set of rules that defines how an organization calculates wages, processes payroll, distributes payments, applies deductions, and assigns accountability for each step in the process.

A payroll policy covers all workers the company pays. This typically includes full-time employees, part-time employees, contractors, and seasonal staff. The scope should be stated explicitly in the policy document rather than assumed, because disputes about who the policy covers are among the most common payroll disagreements employers face.

A payroll policy and its supporting payroll procedures serve different functions. The policy defines the rules. The procedures describe the specific steps the payroll team follows each cycle to execute those rules. Both documents are required. A policy without supporting procedures produces inconsistent execution. Procedures without a governing policy have no written authority to resolve disputes.

Why is a payroll policy important?

A payroll policy is important because it removes ambiguity from compensation decisions, assigns clear compliance responsibility, and gives employees a documented reference for understanding how their pay is calculated.

For employees, a payroll policy answers the questions that come up most often. The payroll policy provides information about payday schedules, the calculation of overtime, and the deductions that are taken from each paycheck, along with their reasons. Employees stop bringing the same questions to HR every cycle when those answers exist in writing. New hires understand their compensation structure during onboarding instead of finding out inconsistently after the first paycheck.

A written payroll policy also assigns clear ownership to each step in the payroll process, from timesheet approval through payment release. This structure reduces recurring errors and prevents unauthorized access to sensitive compensation data. It also produces the documented compliance record that Department of Labor and IRS auditors expect to see when they investigate a wage complaint.

A documented pay schedule protects both the employer and the employee. Employees plan recurring expenses, including rent, loan repayments, and household bills, around the date wages arrive. Inconsistent pay dates increase financial stress, particularly for hourly workers. They also violate state wage payment timing laws in most jurisdictions, which specify the maximum permissible gap between work performed and wages paid.

What does a payroll policy include?

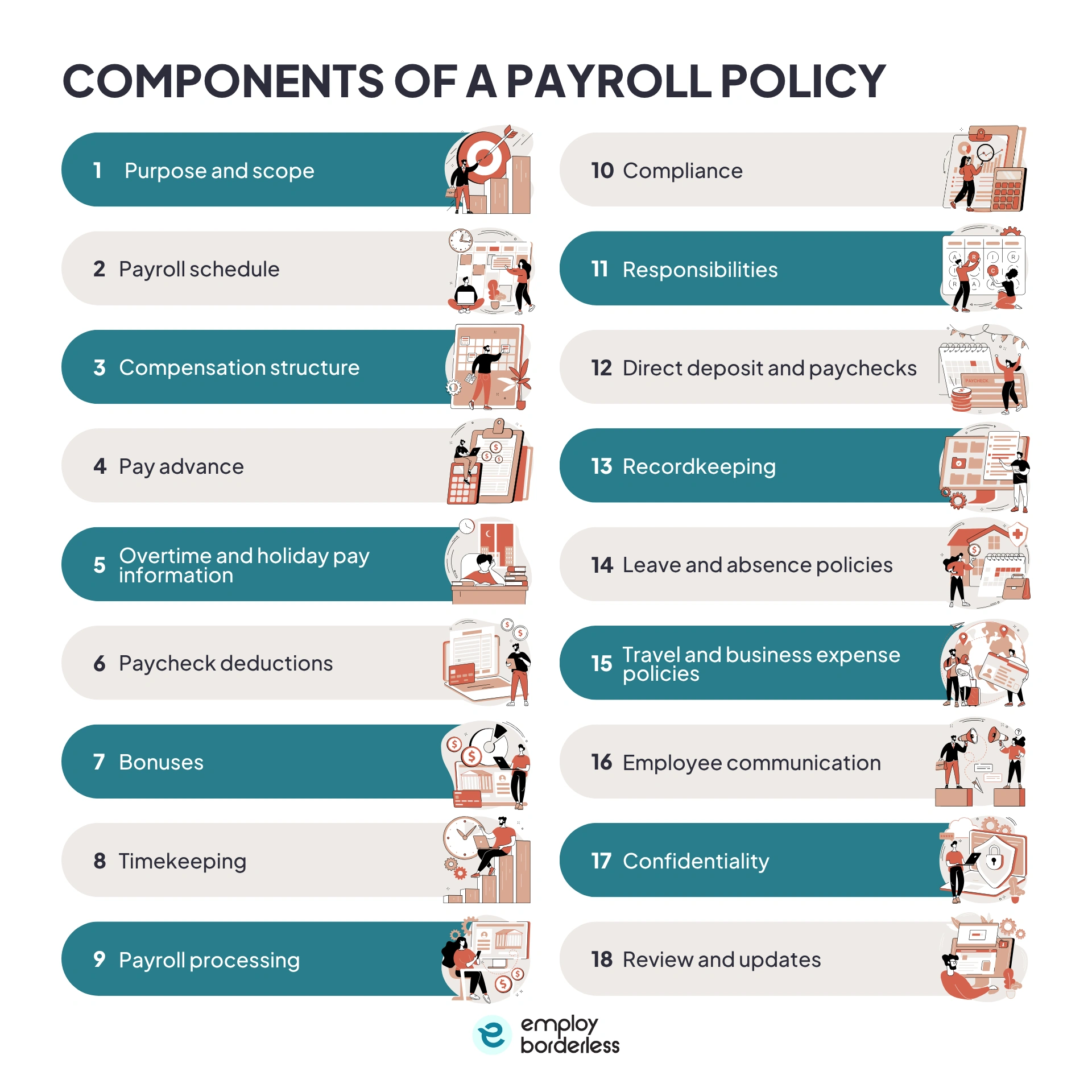

A payroll policy includes many important components. These cover purpose and scope, pay schedule, compensation structure, pay advance rules, overtime and holiday pay, deductions, bonuses, timekeeping, payroll processing, compliance, responsibilities, payment methods, recordkeeping, leave policies, expense policies, employee communication, confidentiality, and a review process.

A complete payroll policy template covers each of the following 18 areas. Businesses may adjust components based on workforce size and industry, but the list below represents the standard set applicable to most US employers.

Purpose and scope

The purpose and scope section states why the payroll policy exists and names every worker category it covers. It identifies the policy's objective, lists the employee types included (full-time, part-time, contractors, and seasonal), and names the person or department responsible for maintaining it. This section references the federal, state, and local laws with which the policy is written to comply. Disputes about policy applicability are significantly less common when the scope is stated in the first section rather than implied throughout the document.

Payroll schedule

The payroll schedule defines how frequently employees are paid and the exact date payment is issued each cycle. Common US pay frequencies are weekly, biweekly, semimonthly, and monthly. The policy should specify the pay period start and end dates, the payday for each cycle, and the cut-off deadline for payroll data submission. It should also document the protocol when a scheduled payday falls on a weekend or a federal bank holiday.

Compensation structure

The compensation structure section documents how the company determines wages, salaries, and all other forms of pay. This includes hourly rates, salary bands, the criteria that trigger a pay increase, commission structures, and any other variable pay components. The section should state how compensation is communicated to employees at the time of hire and how changes are documented and communicated going forward. A written compensation structure reduces inconsistent pay decisions across departments and supports pay equity compliance under applicable state laws.

Pay advance

The pay advance section defines whether the company offers paycheck advances and the rules that govern each request. The policy should specify eligibility criteria, the maximum advance amount, the repayment schedule, and whether any fees apply if advances are permitted. The policy should state that plainly if the company does not offer pay advances. Leaving this topic undocumented produces ad-hoc decisions that are applied inconsistently across employees, creating both morale and potential discrimination exposure.

Overtime and holiday pay information

The overtime and holiday pay section defines which employees qualify for overtime, the calculation method, and the pay treatment for holiday work. Non-exempt employees must receive at least 1.5 times their regular rate of pay for all hours worked beyond 40 in a workweek under the FLSA (Fair Labor Standards Act).

California calculates overtime daily as well, requiring premium pay for hours worked beyond eight in a single day. The policy should specify the overtime eligibility classification rules and how the regular rate of pay is calculated when bonuses or commissions are included. It should also state whether premium pay applies to work performed on designated company or federal holidays.

Paycheck deductions

The paycheck deductions section lists every deduction that can appear on an employee's pay stub and the authorization process for each. Mandatory deductions include federal income tax, state and local income taxes where applicable, Social Security tax at 6.2% of wages up to the annual wage base, and Medicare tax at 1.45% of all wages.

Voluntary deductions include 401(k) deferrals, health and dental insurance premiums, flexible spending account contributions, and any employee-authorized charitable deductions. The section should also address involuntary deductions, such as court-ordered wage garnishments and the legal limits that govern each type.

Bonuses

The bonuses section defines each type of bonus the company pays, the eligibility criteria, and the timing and method of payment. Bonus types include performance bonuses, signing bonuses, referral bonuses, and any other contractual or discretionary incentive payments. The section should clarify whether each bonus is guaranteed or discretionary.

Non-discretionary bonuses must be included in the regular rate of pay when calculating overtime under the FLSA. The policy should document the tax withholding treatment that applies to each bonus type so that payroll processes them consistently.

Timekeeping

The timekeeping section describes the method employees use to record hours worked and the rules for submitting and approving time records each cycle. It specifies the timekeeping system in use, the submission deadline before each payroll run, and the rounding rules the system applies to clock-in and clock-out times.

The section should address the procedure when an employee forgets to clock in or out and state the consequences for falsifying time records. Manager responsibilities for reviewing and approving timesheets before the payroll cut-off should be explicitly defined here.

Payroll processing

The payroll processing section documents the internal workflow that converts approved time and compensation data into employee payments. It covers the payroll calendar, names who are responsible for running each cycle, and defines the internal review and approval steps that must occur before funds are released. The section should also specify the process for issuing off-cycle or manual checks. It should document the correction procedure for errors discovered after a cycle closes, including which role has the authority to approve the correction.

Compliance

The compliance section identifies the federal, state, and local laws the payroll function must adhere to and names who is responsible for monitoring regulatory changes. The primary federal frameworks are the FLSA, the Internal Revenue Code, and the ERISA (Employee Retirement Income Security Act). State wage payment statutes add requirements on pay frequency, final paycheck timing, and permissible deduction types that vary significantly by state.

For businesses with employees in multiple states or remote workers in new locations, the compliance section should identify who tracks legislative changes in each jurisdiction and how quickly the policy is updated when laws change.

Responsibilities

The responsibilities section names who owns each function in the payroll process and defines what each role is accountable for. Payroll staff responsibilities cover data processing, tax filing, and recordkeeping. HR responsibilities cover employee classification, compensation changes, and onboarding data accuracy.

Manager responsibilities cover timesheet approval and reporting workforce changes before the payroll cut-off. Employee responsibilities cover accurate time recording, keeping personal information current, and reviewing pay stubs each cycle. Assigning these responsibilities in writing is the primary mechanism for reducing recurring errors because errors most often occur at handoff points between roles.

Direct deposit and paychecks

The direct deposit and paychecks section defines the payment methods the company uses and the rules that apply to each. Most US employers use direct deposit as the primary payment method. The policy should specify whether direct deposit is mandatory or voluntary, the deadline for submitting banking information before the first pay date, and the protocol when a direct deposit fails.

For employees paid by paper check, the section should address how checks are distributed and the process for handling uncollected checks. State pay stub content and disclosure requirements vary and should be addressed specifically for each state where the company operates.

Recordkeeping

The recordkeeping section defines what payroll records the company retains, how long each record type is kept, and who controls access to stored records. The FLSA requires employers to retain payroll records for at least three years, covering hours worked, pay rates, total wages paid, and the basis for any wage differentials.

Timekeeping records must be retained for at least two years under the same statute. Many states impose longer retention periods. California, for example, requires payroll records to be retained for three years, with other wage-related records kept for up to four years. The policy should specify the storage format, access controls, and response process for record requests from employees or government agencies.

Leave and absence policies

The leave and absence section defines how paid and unpaid leave is accrued, tracked, and reflected in payroll calculations. This covers paid time off, sick leave, vacation, parental leave, bereavement leave, and state-mandated leave types. The section should specify accrual rates, maximum balances, payout rules at separation, and the payroll treatment for unpaid absences for both exempt and non-exempt employees. Leave law requirements differ significantly across states. Businesses with employees in multiple states should address each state's specific requirements rather than applying a single nationwide leave rule.

Travel and business expense policies

The travel and business expense section defines which work-related costs the company reimburses and the process for submitting and approving each expense. It specifies what is reimbursable, what documentation is required, the submission deadline, and the approval chain. The tax treatment of reimbursements depends on the plan type.

Under an accountable plan, reimbursements are excluded from taxable wages under IRS Publication 463 rules. Under a non-accountable plan, reimbursements are treated as additional wages and are subject to income tax and payroll tax withholding. The plan type should be named explicitly in the policy.

Employee communication

The employee communication section defines how payroll information is shared with employees and what disclosures the company is required to provide. It covers the distribution of pay stubs, W-2 forms, and notices of compensation or deduction changes. The section should specify the method and timing for each type of disclosure, who is responsible for issuing them, and the process employees follow to raise a payroll question or report a discrepancy. A documented dispute process reduces the volume of informal payroll complaints and creates a paper trail that can be relied on if a dispute escalates to a formal wage claim.

Confidentiality

The confidentiality section defines who can access payroll data and the controls that protect employee compensation information from unauthorized disclosure. Payroll records contain Social Security numbers, bank account details, salary figures, and in some cases, medical data tied to leave or benefits.

The section should specify which roles have access to payroll data, how that access is granted and revoked, and the consequences for unauthorized disclosure. Businesses operating in California must also align their payroll data handling with the CCPA (California Consumer Privacy Act), which applies to employee data as of January 1, 2023.

Review and updates

The review and updates section defines how frequently the payroll policy is reviewed, who conducts the review, and how approved changes are communicated to employees. A payroll policy should be reviewed at least annually. Reviews should also be triggered by material changes to employment law, tax rates, or the company's workforce structure.

The section should name the responsible reviewer, the approval authority for changes, and the employee notification process when the policy is updated. A payroll policy that has not been reviewed in more than 12 months is likely out of compliance with at least one change in federal or state law.

How to write a payroll policy?

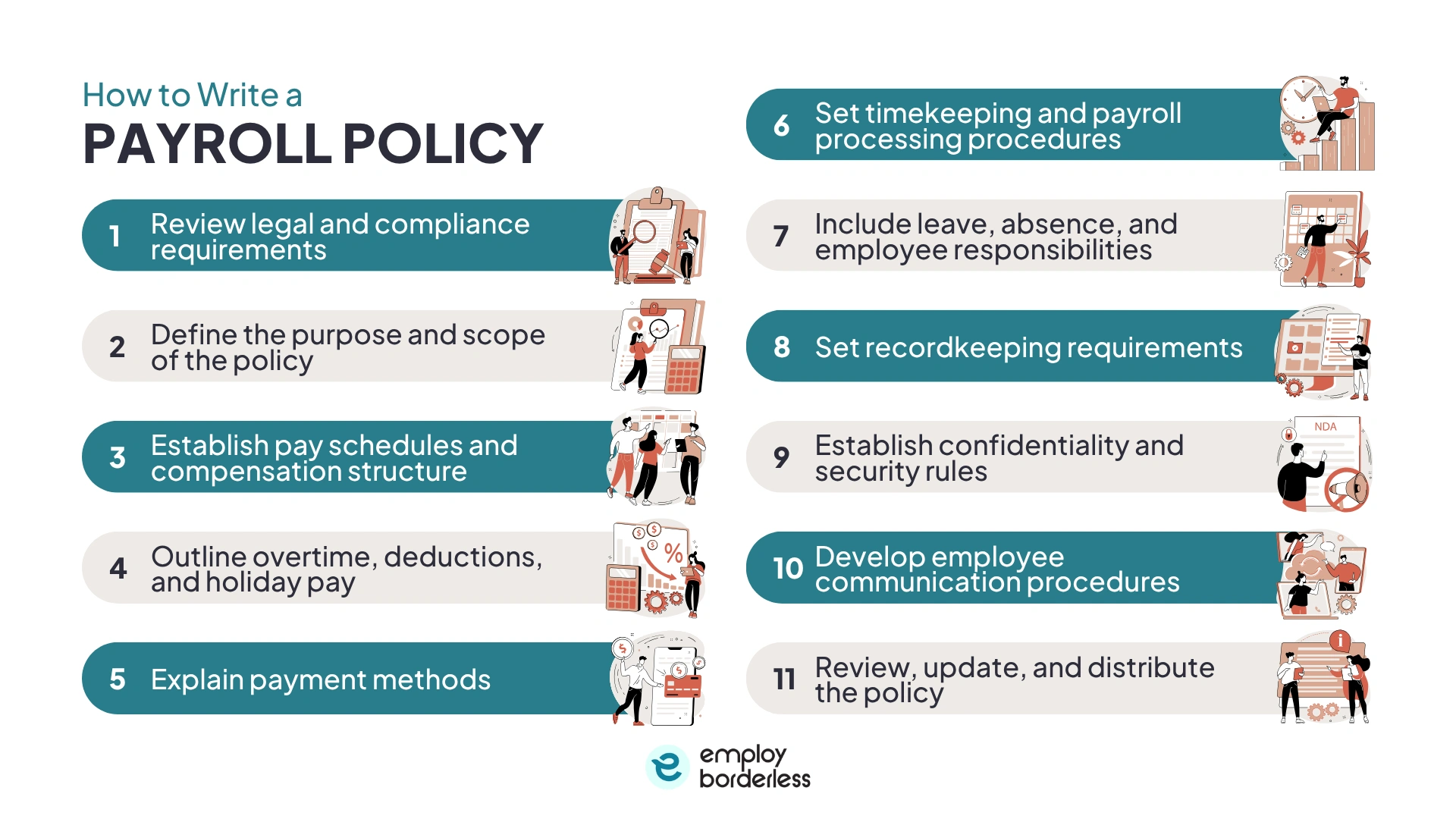

To write a payroll policy, review applicable laws first. Then work through each of the 18 components in sequence, assign review and approval ownership, conduct a legal review before distribution, and collect employee acknowledgments when the final document is issued.

Review legal and compliance requirements

The first step in writing a payroll policy is identifying every law that governs how the company pays its employees. Federal requirements come from the FLSA, the Internal Revenue Code, and ERISA. State requirements vary by jurisdiction and cover pay frequency, final paycheck timing, permissible deductions, overtime thresholds, and leave mandates. For multi-state employers, each state's requirements must be reviewed individually. An employment attorney or HR specialist with payroll compliance experience should review the completed policy before it's distributed.

Define the purpose and scope of the policy

The purpose and scope section should state what the policy governs and which workers it applies to before any other section is drafted. Write one clear statement of the policy's objective. List the employee categories covered, including any exceptions. Reference the legal frameworks the policy operates under. This section anchors every subsequent component. If the scope is ambiguous, each component section will generate its own scope dispute.

Establish pay schedules and compensation structure

Pay frequency should be confirmed against state minimum pay frequency requirements before it's documented in the policy. California, for example, requires most employees to be paid at least twice a month. Document the pay period start and end dates, the payday for each cycle, and the cut-off deadline for payroll data submission once pay frequency is confirmed. Then document each compensation type in use. These include hourly rates, salaries, commissions, and any other variable pay components. State the criteria that trigger a compensation change and how that change is documented.

Outline overtime, deductions, and holiday pay

Over time, deductions and holiday pay each carry distinct legal compliance requirements and should be documented separately rather than combined. Identify which employees are non-exempt under the FLSA and any applicable state overtime rules for overtime. List every mandatory and voluntary deduction and the authorization process for each deduction. Specify which holidays are recognized, whether working a holiday triggers premium pay, and whether holiday pay is factored into the regular rate of pay for overtime calculation purposes for holiday pay.

Explain payment methods

The payment methods section should document how employees receive wages and what each employee must do to set up their chosen payment method. Specify whether direct deposit is required or optional. State the deadline for submitting banking information before the first pay date. Document the alternative for employees who cannot use direct deposit. Address electronic versus paper pay stub delivery and confirm that the company's method meets the pay stub content disclosure requirements in each state where it operates.

Set timekeeping and payroll processing procedures

Timekeeping and processing procedures are the operational documents that support the policy rules, and both need the same level of specificity. Document the system, submission deadlines, rounding rules, and the process for disputed or missing clock entries for timekeeping. Document the full cycle workflow from data cut-off through payment release, including each review and approval step for payroll processing. The procedures should be detailed enough for a new payroll team member to run a pay cycle accurately without asking for guidance.

Include leave, absence, and employee responsibilities

Leave policy and employee responsibilities are two of the most frequently underdocumented areas in payroll policy, and both are common sources of formal wage complaints. For each leave type, specify the accrual rate, usage rules, payout at separation, and payroll treatment for partial pay periods. Document exactly what each employee must do for payroll to be accurate for employee responsibilities. This means timely timesheet submission, keeping personal and banking information current, reviewing pay stubs each cycle, and using the correct channel to report a discrepancy.

Set recordkeeping requirements

The recordkeeping section should document retention periods by record type, not as a single blanket rule. Payroll records require a minimum of three years under the FLSA. Timekeeping records require a minimum of two years. State requirements may be longer. Specify where records are stored, who has access, and the process for responding to a record request from an employee or government agency. Include a destruction schedule for records whose retention period has expired.

Establish confidentiality and security rules

Payroll data security warrants its own section because the legal exposure from a breach varies by state, and the compliance obligations are specific. Specify which roles can access payroll data, how access is granted and revoked, and what actions constitute a prohibited disclosure. Address data storage and transfer requirements for any third-party payroll providers the company uses. Update this section promptly when data protection laws in the company's operating states change.

Develop employee communication procedures

The communication procedures section should define both how the company delivers payroll information to employees and how employees escalate a payroll problem. Specify who issues pay stubs and W-2s, the method and timing for each, and the point of contact for payroll questions. Set a response time standard for payroll queries.

Document the correction process when an employee reports an error, including the timeline for issuing a correction payment. A documented escalation path reduces informal complaints and creates a record that can be referenced in a formal dispute.

Review, update, and distribute the policy

A payroll policy has no legal or operational effect until it is reviewed for compliance, distributed to all employees, and acknowledged in writing. Conduct a legal review before the first distribution. Issue the document to all employees with a written acknowledgment form. Store signed acknowledgments. Set the first review date for 12 months from distribution and schedule it as a recurring calendar event. When the policy is revised, issue the updated version, collect new acknowledgments, and log the revision date, the changes made, and the approving authority.

When should you get outside help managing your payroll policy?

You should get outside help managing your payroll policy when the company expands to multiple states, the workforce includes multiple compensation types, or the same payroll errors recur despite internal corrections.

Each state where employees work creates separate wage laws, pay frequency, and tax filing requirements. A payroll policy written for a single state will not cover another state without deliberate revision, and most internal HR teams do not have the capacity to track multi-state legislation on an ongoing basis.

Businesses with a mix of exempt and non-exempt employees, contractors, commission workers, and part-time staff need a policy that addresses each classification correctly. Most worker misclassification errors trace back to a payroll policy that did not define classification rules clearly, not to deliberate intent.

Recurring errors are the third trigger, when the same category of mistake appears across multiple pay cycles. The policy or the procedures that support it have a structural gap that an internal review is unlikely to identify without an outside perspective.

What are some examples of payroll policies?

Examples of payroll policies include a direct deposit policy, a pay advance policy, an overtime policy, and a payroll error correction policy. A direct deposit policy outlines if electronic payment is required and the deadline for submitting banking details. A pay advance policy defines maximum advance amounts and the repayment schedule. An overtime policy identifies which employees are non-exempt and names the approval step required before overtime is worked. A payroll error correction policy typically allows 24 to 48 hours for corrections after a discrepancy is reported.

How often should payroll be run?

Payroll should be run at the frequency that complies with the state law governing each employee's work location. Most states set a minimum pay frequency. California requires most employees to be paid at least twice a month. Biweekly payroll is the most common schedule among US private-sector employers, accounting for approximately 43% of businesses, according to the Bureau of Labor Statistics. Weekly schedules are more common in construction and hospitality. Monthly payroll is rare in the US and typically limited to certain exempt employee populations.

How does a payroll policy explain gross pay and net pay?

A payroll policy explains gross pay as total compensation earned before any deductions, and net pay as the amount the employee receives after all mandatory and voluntary deductions are applied. The policy should define both terms, list the deduction categories that reduce gross pay to net pay, and direct employees to where they can find a full breakdown of their own deductions.

What payroll deductions should be included in a payroll policy?

A payroll policy should include both mandatory deductions and voluntary deductions, along with the authorization process and legal limits that apply to each. Mandatory payroll deductions are federal income tax, state and local income taxes where applicable, Social Security tax at 6.2% of wages up to the annual wage base, and Medicare tax at 1.45% of all wages. An additional 0.9% Medicare surtax applies to wages above $200,000. Voluntary deductions include 401(k) contributions, health and dental insurance premiums, flexible spending account contributions, and employee-authorized charitable deductions.

How long should payroll records be kept under a payroll policy?

Payroll records should be kept for a minimum of three years, and timekeeping records for a minimum of two years under the FLSA (Fair Labor Standards Act). The payroll records covered by the three-year requirement include hours worked, pay rates, total wages paid, and the basis for any pay differentials between employees in similar roles. California requires payroll records for three years, while many states require longer retention periods than federal law.

What is the difference between a payroll policy and payroll procedures?

A payroll policy defines the rules that govern compensation decisions. Payroll procedures define the step-by-step actions the payroll team takes each cycle to execute those rules. The policy is the authority document. The procedure is the operational guide. A payroll policy might state that overtime requires manager approval before it's worked. The supporting procedure would define exactly how that approval is documented, where the record is stored, and how it flows into the payroll calculation.

What should a payroll overpayment policy include?

A payroll overpayment policy should define how overpayments are identified, how affected employees are notified, and the method and timeline for recovering the excess amount. Overpayment recovery is governed by state law, and the rules differ significantly across states. Most states require the employer to provide written notice to the employee before making any deduction to recover an overpayment. Many states cap how much can be recovered per pay period.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations