Labor laws impacting payroll: key regulations to know

Robbin Schuchmann

Co-founder, Employ Borderless

Labor laws set guidelines on employee rights and employer duties which include issuing payment, working hours, safety conditions, and benefits. These laws are important for payroll processing to make sure that employers follow the regulations and employees are paid fairly and accurately.

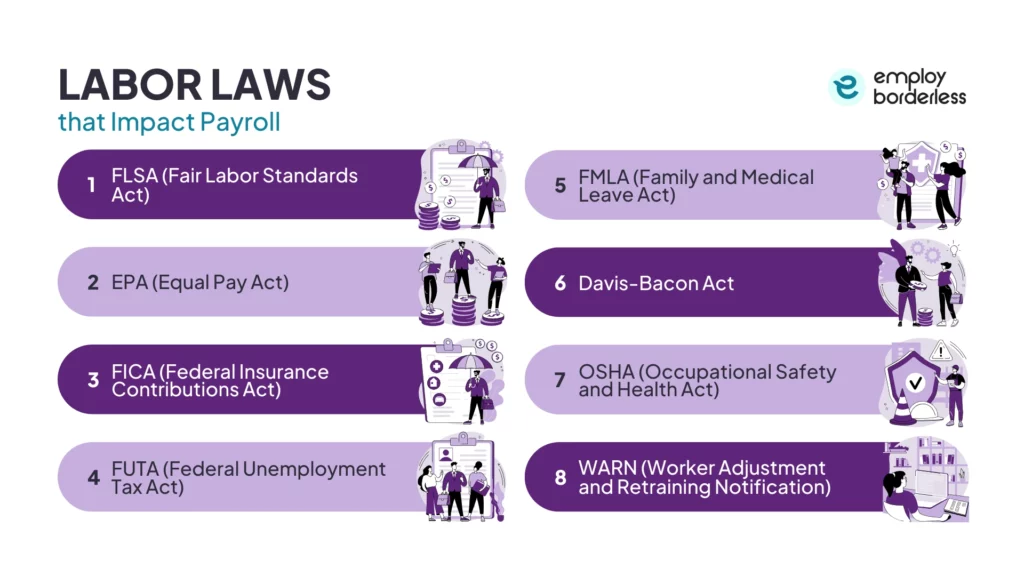

The labor laws that impact payroll processing are FLSA (Fair Labor Standards Act), EPA (Equal Pay Act), FICA (Federal Insurance Contributions Act), FUTA (Federal Unemployment Tax Act), FMLA (Family and Medical Leave Act), Davis-Bacon Act, OSHA (Occupational Safety and Health Act), and WARN (Worker Adjustment and Retraining Notification).

Each labor law determines the requirements for minimum wage, overtime compensation, equal salary, tax compliance, and leave benefits. Payroll systems have to follow these guidelines to guarantee that wages are accurate, taxes are managed appropriately, leave is tracked, and the company stays compliant to avoid legal penalties.

What are labor laws?

Labor laws are employment laws that are a clear set of rules and regulations for employee rights, employer duties, and the role of trade unions. These laws deal with different areas such as worker’s health and safety, working conditions, terms of employment, minimum wages, and workers’ rights.

Countries have established different systems of labor laws, and each of these countries reflects their own specific cultural, political, and economic context. For example, Sweden, Denmark, and Germany protect employee rights through Social Security measures, cooperative labor arrangements, and union involvement. Other countries such as Australia and Japan favor employer rights focusing more on workplace harmony.

Labor laws determine the requirements for payroll, including wage rates, conditions for overtime, allowed deductions, and on-time payment of salaries. Payroll systems function accurately as they obey these requirements. Payroll helps avoid legal consequences, maintains trust in the workforce, and ensures all employees are treated fairly in compliance with these labor laws.

Why are labor laws important for payroll management?

Labor laws are important for payroll management because they establish a legal framework that makes sure employers fulfill their duties and employees are accurately compensated.

FLSA (Fair Labor Standards Act) is an important component of payroll management, which establishes guidelines for child labor, overtime compensation, minimum wage, youth employment standards, and recordkeeping.

Companies have to pay their covered non-exempt workers the federal minimum wage and overtime compensation equal to one and a half times the usual rate of pay for hours exceeding 40 in a workweek, according to a fact sheet titled “Fact Sheet #56A: Overview of the Regular Rate of Pay Under the Fair Labor Standards Act (FLSA)”, by the DOL (U.S. Department of Labor).

Payroll management needs to follow these labor laws to avoid penalties, fines, and legal action that occur from wage breaches or improper payroll processing. Businesses also fulfill their federal, state, and local tax duties and stay compliant with the law. Labor laws also require accurate tax withholding and reporting. These laws uphold a company’s morale and legal responsibilities by protecting employees’ needs and encouraging fair treatment.

What are the labor laws that impact payroll?

The labor laws that impact payroll are the FLSA (Fair Labor Standards Act), the Equal Pay Act of 1963, FICA (Federal Insurance Contributions Act), FUTA (Federal Unemployment Tax Act), FMLA (Family and Medical Leave Act), Davis-Bacon Act, OSHA (Occupational Safety and Health Act), and (WARN) Worker Adjustment and Retraining Notification Act.

FLSA (Fair Labor Standards Act)

The FLSA (Fair Labor Standards Act) of 1938 is a foundational U.S. labor law that sets important pay and working conditions guidelines. The law affects full-time and part-time employees in the commercial sector and federal, state, and municipal governments. It also establishes federal standards for minimum wage, overtime compensation, recordkeeping, and child labor protections.

Employers must ensure that non-exempt employees are paid the federal minimum wage of $7.25 per hour, according to an article titled “Minimum Wage” by the DOL (U.S. Department of Labor).

Employers have to pay a higher federal minimum wage when state law sets a higher rate. Non-exempt employees receive overtime pay at one and a half times their regular hourly rate for any hours worked above 40 in a workweek.

Payroll records are kept for at least three years, while documents used to determine compensation are kept for two years. Employers are liable for back pay and damages if they violate these requirements. Payroll management has to follow all FLSA regulations to ensure compliance.

EPA (Equal Pay Act)

The EPA (Equal Pay Act of 1963) is a federal law in the United States that requires men and women to be paid equally for performing the same amount of labor in the same place. This law forbids gender-based wage discrimination and covers all types of compensation, which includes benefits, overtime pay, bonuses, salaries, and other types of payment.

The EPA impacts payroll management by requiring employers to make sure that men and women receive equal pay for performing equal work. This legal obligation pushes organizations to implement fair and transparent payroll systems that categorize jobs based on skill, responsibility, effort, and working conditions rather than job titles alone.

Payroll managers conduct regular pay audits, adjust compensation structures, and maintain accurate records to stay compliant and avoid legal penalties. Payroll systems are created to prevent gender-based wage discrimination and support equity, monitor pay differences, and provide documentation that follows the act’s requirements.

FICA (Federal Insurance Contributions Act)

The FICA (Federal Insurance Contributions Act) is a law of the United States that was passed in 1935. This act requires payroll taxes to finance the Social Security and Medicare systems.

Employers and employees each provide a portion of their wages under FICA, 1.45% for Medicare, and 6.2% for Social Security. Employees who make more than $200,000 a year are responsible for paying an additional 0.9% Medicare tax, according to an article titled “Topic no. 751, Social Security and Medicare withholding rates” published by the IRS.

The portions withheld from both the employers’ and employees’ wages are given to retired workers, people with disabilities, and employees who depend on these donations. Employers are in charge of deducting these taxes from employee paychecks and sending them to the IRS to guarantee compliance with federal laws.

Payroll departments keep their systems updated to track employee wages, apply the appropriate tax rates, and produce necessary tax forms like Form 941 and W-2. Payroll operations have to prioritize compliance since inaccurate FICA processing causes legal problems, audits, and fines.

FUTA (Federal Unemployment Tax Act)

FUTA (Federal Unemployment Tax Act) is a federal law that requires employers to pay a federal tax to support and benefit unemployment insurance programs. It is important to understand FUTA as it guarantees compliance with federal laws and promotes worker financial stability.

This tax is paid by employers and it is not withheld from workers’ paychecks. There are exceptions for some wages that do not fall under FUTA, such as income from a deceased spouse and charitable organizations.

Employers who pay their state unemployment taxes on time obtain a credit of up to 5.4%, which effectively lowers the federal rate to 0.6%. The regular FUTA tax rate is 6% on the first $7,000 of each employee’s yearly wages, according to an article titled “FUTA credit reduction” published by the IRS.

A lower credit leads to a higher FUTA tax rate for employers in states that have not paid back federal loans for unemployment compensation. Employers are required to file IRS Form 940 each year to report and pay FUTA taxes.

Employers have to use the EFTPS (Electronic Federal Tax Payment System) to deposit the tax before the end of the following month if their FUTA tax burden is over $500 in a given quarter, according to an article titled “Topic no. 759, Form 940, Employers Annual Federal Unemployment (FUTA) Tax Return – filing and deposit requirements, published by the IRS.

FUTA impacts payroll by requiring certain reporting and deposit procedures, imposing an employer-paid tax on earnings up to $7,000 per employee, and providing a potential credit for timely state unemployment tax payments, according to an article titled “Payroll Tax Training; IRS Basic Employment Lesson Modules – Payroll Taxes; Form 940, Federal Unemployment Tax (Lesson 10)” published by the IRS.

FMLA (Family and Medical Leave Act)

The FMLA (Family and Medical Leave Act) is a 1993 labor law that requires employers to provide employees with unpaid time off for serious family health conditions or situations. The FMLA allows a qualified employee to take up to 12 weeks for reasons such as childbirth, adoption, military leave, foster care placement, and family or personal illness, according to a fact sheet titled, “Fact Sheet #28I: Counting Leave Use under the Family and Medical Leave Act, published by the DOL (U.S.Department of Labor).

Employers are required to maintain their health insurance coverage during FMLA absence, even if the employee is not paid during this time. Employers manage premium payments and deductions to employees who are working actively. Employees use accrued paid leave, such as vacation or sick days, concurrently with FMLA leave, meaning payroll departments have to accurately coordinate paid and unpaid leave balances.

Employers maintain thorough records of FMLA leave usage and communications for compliance purposes, which increases administrative complexity to payroll operations. FMLA increases financial burdens such as benefit continuation, hiring temporary replacements, or paying overtime to cover absent workers. FMLA provides important protections for employees, and it also adds financial responsibilities to employers’ payroll systems.

Davis-Bacon Act

The Davis-Bacon Act of 1931 is a federal law that requires workers working on federal or federally supported construction projects worth more than $2,000 to be paid a standard wage and fringe benefits. The U.S. Department of Labor sets the standard wage, which is the average salary paid to similarly employed people in the area where the work is done.

The act helps keep local workers from being replaced by lower-paid workers from other regions and guarantees that federal contracts do not undercut local wage standards. It also covers a range of construction-related operations, such as building, repairing, or altering public structures. Contractors and subcontractors have to present weekly certified payroll records to guarantee compliance with the standard wage.

Contractors are required to provide certified payroll reports using Form WH-347, every week that include information on employee classifications, hours worked, wages paid, and fringe benefits offered, according to an article titled “Instructions For Completing Davis-Bacon and Related Acts Weekly Certified Payroll Form, WH-347” published by the DOL (U.S. Department of Labor).

Noncompliance leads to penalties such as withholding payments, contract termination, or exclusion from future contracts. Contractors offer real benefits like health insurance or retirement programs, or they give fringe perks as cash earnings. Fringe benefits do not include payments mandated by municipal, state, or federal legislation.

OSHA (Occupational Safety and Health Act)

OSHA (Occupational Safety and Health Act) of 1970 is a federal law in the United States that provides safe and healthy working conditions for workers by establishing and implementing standards as well as offering education, training, outreach, and support. The act requires employers to keep the workplace free from known dangers that cause death or serious physical harm, and also requires employees to follow safety and health regulations.

Employers need to keep workers’ compensation claims and possible absences using the records of work-related illnesses and injuries for calculation. The expense of providing PPE (Personal Protective Equipment) and other safety training programs has an impact on overall compensation costs.

Employers are also required to make sure that workers are accurately compensated for time spent on safety training or for time off work due to accidents at work. Payroll systems have to accurately measure and report these factors to maintain OSH Act compliance and efficiently manage related expenses.

WARN (Worker Adjustment and Retraining Notification)

WARN (Worker Adjustment and Retraining Notification) Act is a U.S. federal law that was passed in 1988 and requires companies employing 100 or more full-time workers to give written notice at least 60 days before a major termination or company shutdown.

The employer has to give the mass layoff written notice to the affected workers, their representatives (such as unions), the state displaced worker unit, and the local government. This law helps workers and their families prepare for unexpected job loss and offers people time to pursue new employment or participate in retraining programs. The act helps communities prepare for and adapt to changes in the workforce, which promotes economic stability.

Employers violating the WARN Act by failing to give 60 days’ notice of a factory closure or mass layoff, are held accountable for up to 60 days’ worth of back pay and benefits for each impacted employee, according to an article titled “Plant Closings and Layoffs” published by the DOL (U.S. Department of Labor). The WARN Act encourages preparation and warning to protect communities and workers during unemployment.

Payroll departments need to carefully track these liabilities to guarantee compliance and appropriate compensation. This act has an impact on payroll planning and budgeting because companies have to take into consideration the expected financial responsibilities associated with layoffs and factory closings.

What is payroll?

Payroll is the process through which companies calculate and pay workers for performing work over a given time. It means keeping track of hours worked, calculating gross pay, deducting taxes and benefits, and issuing net pay. Payroll also includes maintaining records, following tax laws, and making sure payments are made on time. Accurate payroll management is important for legal compliance, staff satisfaction, and efficient financial planning.

The process of payroll involves gathering information about employees such as their working hours, calculating their gross payment, deducting taxes and other withholdings, and paying a net salary. It also includes attendance monitoring, distributing payments, and maintaining records for tax compliance and withholding. The process makes sure that employees are paid on time while meeting the legal requirements.

Why is payroll important?

Payroll is important because it guarantees that workers receive their payments on time and accurately, which builds employee satisfaction and trust. It helps companies keep accurate financial records, avoid fines, and adhere to labor and tax regulations. Payroll management helps in budgeting, data security, operational efficiency, and protecting a business’s reputation.

What are the common payroll processing steps?

The common payroll processing steps are gathering employee information, choosing a payroll step, setting up direct deposit, establishing a time-tracking system, calculating gross payment, approving and submitting payroll, calculating payroll taxes, calculating deductions, and collecting employee timesheets. Payroll processing steps guarantee accurate payment, compliance with the law, and appropriate documentation for financial planning and audits.

What are the most common payroll challenges?

The most common payroll challenges are data accuracy, compliance issues, employee classification, manual processes, overtime calculations, tax miscalculations, overtime calculations, and data security. There are many ways to solve these payroll challenges, such as automation, regular audits, safe systems, and following payroll laws and compliance standards.

What are the different types of payroll systems?

The different types of payroll systems are payroll software systems, payroll card systems, online payroll services, manual payroll systems, outsourced payroll systems, cloud-based payroll systems, and in-house payroll systems. Payroll systems manage employee data, calculate wages and deductions, ensure tax compliance, process payments, produce reports, and keep records to provide accurate and efficient payroll administration.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations