ICP payroll: definition, benefits, challenges, and factors to consider

Robbin Schuchmann

Co-founder, Employ Borderless

An in-country partner (ICP) in payroll is a local payroll provider that processes employee salaries, withholds taxes, remits statutory contributions, and supports compliance with payroll-related tax and social contribution requirements on behalf of a foreign employer. ICP is one of three core approaches to paying employees internationally. For straightforward jurisdictions, ICP fees range from $20 to $100 per employee per month - far below EOR fees of $199 to $1,000+ per month. Most companies shift from EOR to ICP payroll once they have their own entity and a team of roughly 15 to 20 people in a country.

- ICP processing fee range: $20 to $100 per employee per month for straightforward jurisdictions; up to $200+ for complex ones like France, Brazil, or China.

- EOR fee range: $199 to $1,000+ per employee per month - higher because the EOR assumes legal employment responsibility.

- Minimum monthly country fees: Many ICPs charge $500 to $1,500 per country regardless of headcount.

- Headcount threshold: A team of 15 to 20 people in a country typically justifies switching from EOR to entity plus ICP payroll.

- WPS coverage: In the UAE, the Wage Protection System covers more than 99% of private-sector workers.

ICP sits alongside employer of record (EOR) and in-house payroll through a wholly-owned local entity as the three main options. A fourth option, managed global payroll (sometimes called the aggregator model), is a coordination layer that uses ICPs behind the scenes to deliver multi-country payroll through a single provider. The right choice depends on whether you have your own legal entity in the country, how many employees you're hiring, and how much of the payroll process you want to handle internally.

How does ICP payroll work?

ICP payroll works by outsourcing the payroll process for a specific country to a local provider who has the expertise, systems, and legal standing to calculate wages, withhold taxes, remit statutory contributions, and generate compliant payslips on your behalf. You keep your own legal entity in the country and maintain the employer-employee relationship directly. The ICP handles the mechanics of payroll, not the employment itself.

Each pay cycle, your company sends payroll instructions to the ICP - hours worked, salary changes, bonuses, and any adjustments. The ICP calculates gross-to-net pay using the country's current tax tables, social contribution rates, and statutory deduction rules, then withholds the correct taxes and social contributions, generates payslips, and handles tax filings with the relevant authorities.

How funds reach employees depends on the arrangement. In a pay-through model, the company transfers a lump sum to the ICP covering employee gross salaries, mandatory employer contributions (social security, healthcare, pension), statutory benefits, and the ICP's service fee. The ICP then disburses net pay to employees and remits taxes to authorities. In a direct disbursement model, the ICP calculates payroll and files taxes, but the company's local entity pays employees and remits taxes directly from its own bank account. Many multinationals prefer the direct model for cash-control and audit reasons. Either way, the ICP handles year-end tax reporting, statutory filings, and any government audits related to payroll in that country.

Payment follows the standard payroll cycle of the employee's country - monthly in most of Europe, biweekly or semi-monthly in the US and Canada, semi-monthly in parts of Asia. ICPs use local bank transfers in the country's currency. Beyond base salary, ICPs also manage bonuses, commissions, expense reimbursements, and statutory benefits like 13th-month pay.

If you're funding the ICP in one currency while employees are paid in another, currency conversion adds both cost and risk. Clarify upfront who bears the FX markup and whether the ICP locks exchange rates at a specific point in the pay cycle or uses spot rates at disbursement.

How does ICP payroll differ from an EOR?

The fundamental difference between ICP payroll and an employer of record (EOR) is who holds the legal employment relationship with the employee. With ICP payroll, your company is the legal employer, and the ICP simply processes payroll on your behalf. With an EOR, the EOR provider becomes the legal employer and assumes employment liability, while you retain day-to-day management of the employee's work. Companies choosing between an EOR or PEO for their workforce model should understand that both differ from ICP in this fundamental way.

Dimension | ICP Payroll | Employer of Record (EOR) | Wholly-Owned Entity + In-House Payroll |

Legal employer | Your company | The EOR provider | Your company |

Requires your own entity? | Yes | No | Yes |

Who processes payroll? | The ICP (outsourced) | The EOR provider | Your internal team |

Employment liability | Your company | The EOR provider | Your company |

Compliance responsibility | Your company (ICP supports and advises) | The EOR provider | Your company entirely |

Best for | Companies with existing entities wanting local payroll expertise | Companies hiring in countries without entities | Large operations with dedicated HR/payroll staff |

Typical cost | $20-$200+/employee/month (processing fee only) | $199-$1,000+/employee/month (service fee) | Internal staff + systems + entity maintenance |

If you already have a legal entity in a country and just need someone to run payroll accurately, ICP is the right model. No entity? An EOR employs workers through its own existing entity on your behalf. Large enough team to justify in-house staff? Handle it internally.

What are the three ways to run global payroll?

Companies running payroll across multiple countries choose from three operational models, each with different trade-offs in control, complexity, and growth.

In-house: The company opens payroll offices in each country and builds internal teams with local expertise. This provides maximum control but requires significant investment in local know-how, systems, and headcount. As the number of countries grows, the complexity becomes overwhelming for most organizations.

Distributed (direct ICP relationships): The company outsources payroll to separate local ICPs in each country. Each ICP uses its own formats, reporting methods, languages, and currencies. Payroll data is siloed by location, making it difficult to track global workforce costs or even the total number of employees across all locations. This model works but creates a coordination burden.

Consolidated (managed global payroll): A single provider coordinates payroll across all countries through a network of ICPs, delivering one interface, one data format, and consolidated reporting. The provider handles ICP selection, communication, quality management, and compliance monitoring. This is the model most companies operating in five or more countries eventually adopt.

What is the aggregator model in global payroll?

The aggregator model (also called managed global payroll) is a delivery layer on top of individual ICPs, where a single provider coordinates payroll across multiple countries by managing a network of local ICPs and giving you one point of contact, one data format, and consolidated reporting. It's not a separate employment model from ICP. It's an ICP with coordination and technology on top.

Most companies operating in five or more countries find it impractical to manage individual ICP relationships in each market. Different ICPs use different formats, reporting structures, and payroll calendars. An aggregator normalizes all of that into a single dashboard.

The terms "aggregator" and "managed global payroll" are used largely interchangeably across the industry. The meaningful distinction isn't in the label but in the service level. Some providers offer self-service aggregator platforms where you interact with the technology and the ICPs handle processing. Others offer fully-managed services with dedicated account teams who handle ICP coordination, exception management, and compliance monitoring on your behalf. When evaluating providers, ask which model they operate and what level of hands-on support you'll receive.

The alternative is the wholly-owned model, where a single global payroll provider owns its own payroll operations in every country it covers. The wholly-owned model offers a single platform, consistent data architecture, and single-point accountability. The aggregator model offers more flexibility: ICPs compete for the business of the global payroll provider, which keeps them accountable. If an ICP in a specific country isn't performing, the aggregator can replace them without disrupting your entire payroll operation. Each model trades different risks. Neither is universally better.

When should you use ICP payroll?

ICP payroll is the right model when your company already has a legal entity in the target country but doesn't have the internal resources or local expertise to run payroll in-house. It's the most common model for mid-sized and large companies that have established subsidiaries in multiple countries and need accurate, compliant payroll processing without building a local HR team in every location.

ICP payroll makes the most sense in three situations.

First, when you have an entity but no local payroll staff.

Setting up payroll in a new country requires understanding local tax codes, social contribution rates, mandatory benefits, and filing deadlines. An ICP already has this expertise.

Second, when you're operating in countries with complex or frequently changing payroll regulations.

India is operationalizing its four consolidated Labour Codes (effective November 2025), with final central rules being phased in through 2026 and state-level rules still varying widely. The codes restructure wage definitions, social security, and compliance requirements, and the new 50% wages rule alone changes how PF, gratuity, and bonus are calculated. Brazil's eSocial system, combined with FGTS Digital, continues to expand. Labor authorities now have near-real-time access to employment data, increasing transparency and enabling cross-checks across regulatory databases. France's 2026 Social Security Financing Act (LFSS 2026) introduced new employer contribution structures and parental leave provisions. An ICP in each of these countries tracks these changes as part of their daily operations.

Third, when your headcount in a country is too small to justify a full-time payroll person but too large to ignore.

Typically, a workforce of 15 to 20 people in a country is enough to warrant shifting from EOR to ICP payroll. At that level, companies are established enough to have their own entity, and the per-employee cost of ICP payroll ($20 to $200/month) is significantly lower than EOR fees ($199 to $1,000+/month).

ICP payroll doesn't make sense when you don't have an entity in the country (use an EOR instead), when you're only hiring one or two people in a market you're testing (an EOR is simpler), or when your in-house payroll team is already handling the country effectively. Many companies adopt a hybrid approach - using EOR for initial market entry or in countries with small teams, then transitioning to ICP payroll once they establish their own entity and reach sufficient headcount. This balances speed and flexibility with long-term cost efficiency.

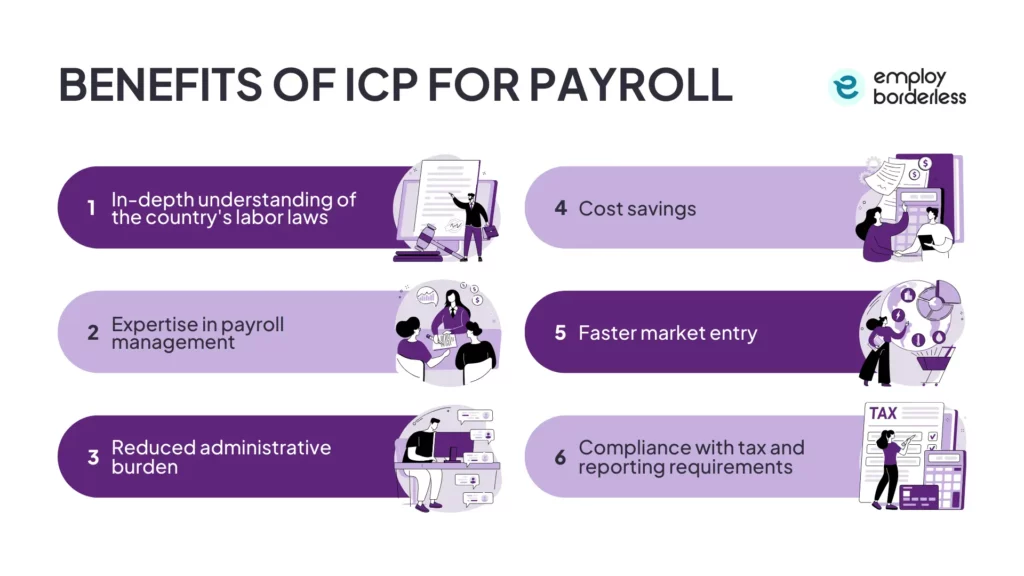

What are the benefits of ICP payroll?

ICP payroll delivers six core advantages over running payroll in-house in each country.

Compliance assurance: ICPs maintain up-to-date knowledge of local employment laws, tax regulations, and mandatory benefits, keeping your international payroll compliant regardless of changing requirements. This matters most in countries like Brazil (eSocial real-time reporting), India (Labour Code restructuring), and France (annual LFSS changes).

Cost efficiency: ICP payroll costs are lower than EOR fees because the ICP is only processing payroll, not assuming legal employment responsibility. For straightforward jurisdictions, ICP fees generally range from $20 to $100 per employee per month versus $199 to $1,000+ for EOR.

Reduced administrative burden: ICPs handle gross-to-net calculations, tax filings, statutory benefit administration, payslip generation, and year-end reporting, freeing your HR and finance teams for other work.

Local expertise: ICPs know local market practices, competitive compensation structures, and cultural expectations around pay - such as 13th-month salary norms, mandatory profit-sharing in some Latin American countries, or country-specific payslip requirements.

Scalability: You can expand or contract your international payroll operations based on business needs without building permanent payroll infrastructure in each location.

Flexibility to replace underperformers: Unlike a wholly-owned global payroll setup, the ICP/aggregator model lets you swap out an underperforming ICP in a specific country without disrupting payroll elsewhere.

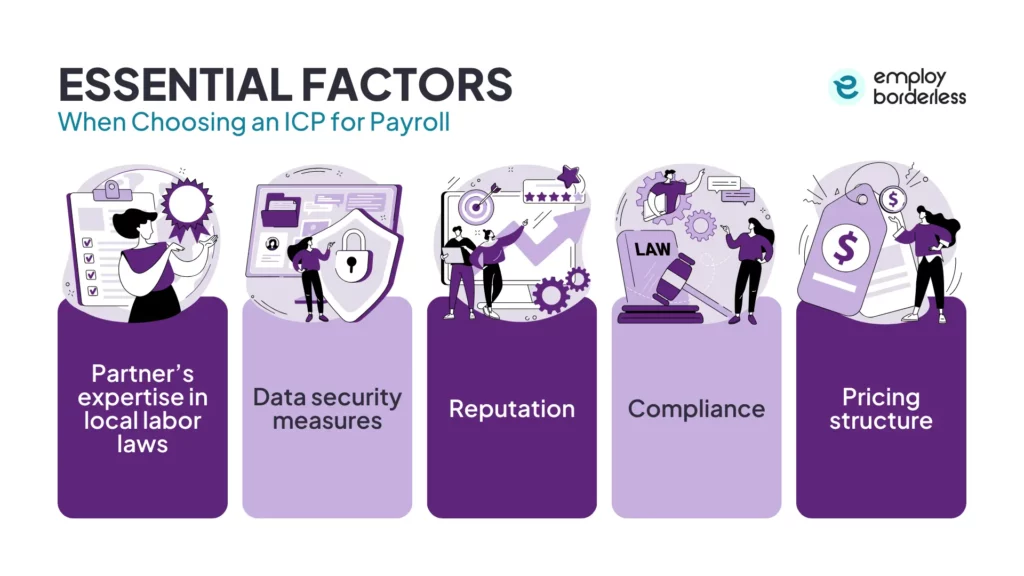

What are the essential factors when choosing an ICP for payroll?

The essential factors when choosing an ICP for payroll are local compliance depth, data security, technology integration, service-level agreements, transparent pricing, and regional expertise.

Local compliance expertise

The ICP's core value is keeping your company compliant with local payroll tax, social contribution, and statutory filing requirements. Ask specifically how the ICP monitors and implements regulatory changes. Every country's payroll involves tax tables, contribution rates, and filing deadlines that change regularly. Look for providers with a documented process for tracking legislative updates and applying them before the effective date. If the ICP can't explain their compliance monitoring process, that's a red flag. In the UAE, for example, the Ministry of Human Resources and Emiratisation (MOHRE) requires private-sector establishments registered with it to pay wages through the Wage Protection System (WPS), under Ministerial Resolution No. 598 of 2022. The WPS covers more than 99% of private-sector workers, though some free-zone authorities apply different rules and certain employee categories are excluded. An ICP operating in the UAE must be thoroughly familiar with WPS regulations and penalties for non-compliance.

Data security and privacy

Payroll data includes some of the most sensitive employee information - salaries, bank details, tax identification numbers, and home addresses. The ICP should meet the data protection standards applicable in the employee's country. For EU-based employees, that means GDPR compliance. For US-headquartered clients, ask about SOC 2 Type II certification, which is typically the first security credential procurement teams evaluate. ISO 27001 certification is a strong additional indicator of security maturity. Ask about encryption standards, access controls, data retention policies, and breach notification procedures.

Technology and integration

The ICP's payroll platform should integrate with your existing HR and finance systems to avoid manual data re-entry and reconciliation. Ask whether the ICP offers API connectivity to your HRIS (Workday, SAP SuccessFactors, BambooHR, HiBob, Rippling, or similar) and whether payroll data can be exported in formats compatible with your general ledger and ERP system. ICPs that still rely on email-based spreadsheet exchanges create unnecessary reconciliation work and increase error risk. Employee self-service capabilities - viewing payslips, updating bank details, accessing tax documents - are increasingly a baseline expectation.

Service-level agreements

SLAs should specify payroll processing timelines, accuracy guarantees, query response times, and remediation procedures for errors. A payroll error in one country can cascade into tax filing problems, employee trust issues, and regulatory penalties. The SLA should define what happens when the ICP makes a mistake, who bears the financial cost of penalties resulting from ICP errors, and how quickly corrections are processed. Include indemnification clauses that protect your company from financial exposure caused by ICP processing failures.

Pricing transparency

ICP pricing is typically structured as a per-employee-per-month fee, but total payroll costs can include setup fees, year-end reporting charges, amendment fees for off-cycle changes, and minimum monthly country fees. Request a complete fee schedule before signing. Watch for hidden charges including VAT on service fees, foreign transaction markups on cross-border payments, and rigid minimum contract terms. For complex jurisdictions like France, Brazil, Italy, or China with small headcount, per-employee fees can exceed $200/month, and many ICPs impose minimum monthly country fees of $500 to $1,500 regardless of headcount. These minimums can distort the per-employee economics for small teams.

Regional expertise and relationships

ICPs rely on local service providers - law firms, tax advisors, and banking institutions. If your situation requires niche expertise (equity management, visa complications, complex tax structures, or country-specific benefits like mandatory profit-sharing in Mexico or 13th-month pay under PD 851 in the Philippines), you need access to the right specialists. Evaluate the ICP's depth of local relationships, not just their payroll processing capability. Ask for references from clients with similar needs in the same country.

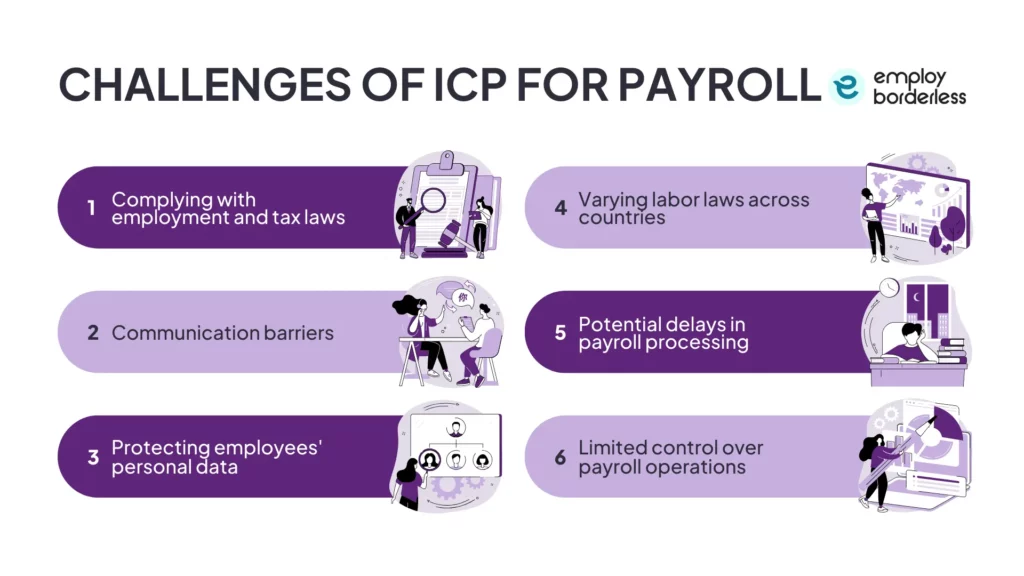

What are the challenges of using ICP payroll?

The main challenges of ICP payroll are retaining ultimate compliance liability, managing payroll calendar coordination across countries, handling data consistency, dealing with currency risk, managing multiple vendor relationships, and maintaining consistent service quality.

Compliance liability: Compliance liability stays with you. Unlike an EOR arrangement where the EOR assumes legal employment responsibility, in an ICP arrangement your company remains the legal employer. If the ICP makes a tax filing error or miscalculates a social contribution, the resulting penalty falls on your company, not the ICP. In nearly every jurisdiction, regulators direct penalties and back-payment orders to the legal employer of record. With an ICP arrangement, that's your company. With an EOR arrangement, that's the EOR. Your recourse is to pursue the ICP for damages under your service agreement, but regulatory liability sits with you. This is why SLAs and indemnification clauses in ICP contracts matter.

Payroll calendar coordination: Payroll calendar coordination is the most common daily pain point. Different countries run different pay cycles (monthly in most of Europe, biweekly or semi-monthly common in the US and Canada), different cut-off dates, and different payment timing norms. Some European countries require salary payment by a specific date each month. Many countries with 13th-month salary requirements (Latin America, the Philippines, Indonesia, Italy, Greece, and others) add extra payment cycles. If you're running ICP payroll in eight countries, you're managing eight different calendars, eight different cut-off deadlines, and eight different disbursement schedules. Understanding the history of payroll regulation in each country helps explain why these differences exist, but the practical challenge is calendar management.

Data consistency: Data consistency requires deliberate effort. When you work with different ICPs in different countries, each one may use a different data format, reporting structure, and payroll calendar. If a finance manager wants to see total global workforce spending or compare costs across locations, they have to retrieve data from individual sources, standardize the format, and convert the currency. Without aggregator technology, this process can take weeks.

Currency risk: When you fund ICPs in one currency while employees are paid in another, FX fluctuations affect your actual payroll costs each cycle. Clarify whether the ICP locks exchange rates at a specific point in the pay cycle or uses spot rates at disbursement. Negotiate transparent FX markup terms and consider whether hedging is worthwhile for large payrolls in volatile currencies.

Managing multiple vendors: Working with separate ICPs in each country means managing multiple contracts, communication channels, invoicing processes, and reporting formats. Companies can reduce this burden by using a managed global payroll provider (aggregator) that presents a unified service experience, or by implementing a payroll aggregation platform that centralizes data from multiple providers into a single dashboard. A clear governance framework with standardized processes for data collection, approval workflows, compliance verification, and performance monitoring also helps.

Shadow payroll: Shadow payroll for cross-border assignees adds complexity. If you have employees on international assignments - working in a country different from their home country - you may need shadow payroll. This means running a parallel payroll calculation in the host country to determine tax obligations there, even though the employee's primary payroll runs in their home country. Not all ICPs handle shadow payroll, so confirm this capability if you have internationally mobile employees.

How do you choose a global payroll provider?

Selecting the right global payroll provider involves five steps, whether you're choosing individual ICPs or a managed aggregator.

Determine your employment model: Decide which employment model is right for each country. EOR for countries without entities where you need to hire quickly. ICP payroll for countries where you have entities. Direct in-house payroll for countries where you have large, established teams. Many companies use all three models simultaneously across different markets.

Decide whether to open an entity: Once you plan a long-term presence in a country, it becomes cost-effective to open a legal entity. Typically, a workforce of 15 to 20 people is enough to warrant the shift from EOR to entity plus ICP payroll. Opening an entity signals to local partners and authorities that the company is committed to the market.

Choose between aggregator and direct ICP relationships: For five or more countries, a managed aggregator is usually more practical than managing individual ICPs. For one or two countries, direct ICP relationships may be simpler and cheaper. Evaluate whether you need one contract and one interface (aggregator) or are comfortable managing separate vendor relationships.

Run a pilot before full deployment: Running a pilot with a new ICP in one or two countries before full deployment helps identify potential issues and confirms service quality. This approach reduces risk while building confidence in the partnership before wider implementation.

Automate the process: An automated platform takes reports from different departments in different countries, standardizes them into a single format, consolidates siloed data streams, and processes payroll accurately. The platform should be tailored for each country's requirements, guiding the payroll team through all necessary steps and confirming the correct taxes are paid.

What does ICP stand for in payroll?

ICP stands for in-country partner (sometimes called in-country provider), referring to a local payroll company that processes payroll on behalf of a foreign employer in a specific country. The term is used primarily in the global payroll industry to describe local firms that handle payroll processing, tax compliance, and statutory filings for multinational companies that have their own legal entities in that country.

In Hindi, ICP ka arth hai "in-country partner" - ek sthaniya payroll provider jo videshi niyokta ki taraf se vetan prakriya, kar withholding, aur statutory filings sambhalta hai. The term is the same across languages; only the pronunciation differs.

Is ICP payroll the same as an EOR?

No, ICP payroll and EOR are different models. With ICP payroll, your company is the legal employer and the ICP only processes payroll. With an EOR, the EOR provider becomes the legal employer. ICP requires you to have your own entity in the country. EOR doesn't. ICP is a payroll outsourcing arrangement. EOR is an employment outsourcing arrangement.

How much does ICP payroll cost?

ICP payroll typically costs less than EOR because the ICP is only processing payroll, not assuming legal employment responsibility. Pricing varies by country and provider. For straightforward jurisdictions, ICP fees generally range from $20 to $100 per employee per month. For complex jurisdictions like France, Brazil, or China, fees can reach $200 or more per employee per month. Many ICPs also impose minimum monthly country fees of $500 to $1,500, which means per-employee economics look different for a team of 3 versus a team of 30. Watch for hidden fees, including setup charges, year-end reporting surcharges, amendment fees for off-cycle changes, VAT on service fees, and FX markups.

What is the ICP Standard Report in global payroll?

The ICP Standard Report is a payroll output document that an in-country partner (ICP) or in-country provider produces to summarize payroll calculations, statutory deductions, and net pay for a given pay period. It gives the client company a structured record of what the ICP processed - gross pay, tax withholdings, social contributions, and net disbursements - in a format that supports reconciliation and compliance review. When evaluating an ICP or reviewing ICP payroll providers, the standard report format is one indicator of the provider's data quality and transparency.

Can you use ICP payroll without a local entity?

No, ICP payroll requires your company to have a legal entity in the country where employees are being paid. The ICP processes payroll on behalf of your entity. If you don't have an entity, you need an EOR. The EOR employs workers through its own existing entity on your behalf, removing the need for you to establish a subsidiary.

What is the difference between ICP and managed global payroll?

Managed global payroll uses ICPs behind the scenes but adds a coordination and technology layer on top, giving you one contract, one interface, and one point of contact across all countries. When you work with ICPs directly, you manage those relationships yourself. Managed global payroll providers (sometimes called aggregators) handle ICP selection, onboarding, communication, and quality management. The terms "aggregator" and "managed global payroll" are used largely interchangeably in the industry.

Do ICPs handle employee benefits?

Some ICPs handle statutory benefits administration (mandatory pension contributions, social insurance, and statutory leave tracking) as part of their payroll processing, but most don't manage voluntary benefits, equity compensation, or expense management. If you need benefits administration beyond what's legally required in a country, or if you need stock option vesting and tax reporting across jurisdictions, you'll typically need a separate benefits broker or equity administration platform. Some countries have specific mandatory benefits that ICPs must manage, such as mandatory profit-sharing in Mexico or provident fund (PF) and Employee State Insurance (ESI) in India.

How do ICPs coordinate with local banks?

ICPs use each country's local banking infrastructure to disburse salaries. In the UAE, payments route through the Wage Protection System (WPS). In India, ICPs use NEFT or RTGS bank transfer systems. In the EU, payments typically flow through SEPA (Single Euro Payments Area). The ICP's integration with local banking systems keeps salary disbursements compliant with country-specific regulations, reaches employee accounts on time, and generates the documentation required by local financial authorities.

What is global payroll reconciliation?

Global payroll reconciliation is the process of examining and aligning global payroll data across all countries to confirm accuracy and compliance. It includes auditing payroll records for discrepancies between what was calculated, what was paid, and what was reported to tax authorities. Reconciliation also involves verifying that currency conversions were applied correctly, that employer contributions match statutory requirements, and that all filings were submitted on time. When payroll data is consolidated through an aggregator, reconciliation is significantly easier than when data is siloed across individual ICPs.

How does ICP payroll relate to EOR or PEO services?

ICP, EOR, and PEO are three distinct workforce models that serve different situations. ICP is payroll outsourcing for companies that already have a local entity. An EOR is employment outsourcing for companies without a local entity. A PEO (professional employer organization) is a co-employment arrangement primarily used within the US, where the PEO shares employer responsibilities with the client company. All three handle payroll processing, but they differ in who holds the legal employment relationship and what level of liability each party assumes.

For a deeper comparison of the two employment models, see our guide on EOR or PEO services.

Co-founder, Employ Borderless

Robbin Schuchmann is the co-founder of Employ Borderless, an independent advisory platform for global employment. With years of experience analyzing EOR, PEO, and global payroll providers, he helps companies make informed decisions about international hiring.

Learning path · 10 articles

Payroll fundamentals

Master the fundamentals with our step-by-step guide.

Start the pathReady to hire globally?

Get a free, personalized recommendation for the best EOR provider based on your needs.

Get free recommendations